California Climate Accountability: Getting Started on SB 253 and SB 261 Reporting

Key Takeaways:

- Emissions Disclosure: SB 253 requires companies in scope to annually disclose scope 1 and 2 GHG Emissions (Scope 3 starting 2027)

- Financial Risks: SB 261 requires companies to report biannually on climate-related financial risks

- Future Guidance: CARB will develop guidance around the climate acts, but these will likely not be finalized until late 2025.

- Getting Ready for Emissions Reporting: Companies can begin developing disclosures aligned with SB 253 requirements using available guidance and standards.

- Framework Clarity: SB 261 is informed by the TCFD and IFRS S2 frameworks. Companies can proactively address the regulation by aligning their reporting with these standards, as CARB continues to finalize specific requirements.

The January 2026 reporting deadline for The California Climate Accountability Package (CCAP), which requires companies to report their greenhouse gas emissions and climate risk exposure, is closing in. Yet, there are still uncertainties about exactly what companies are expected to report on. Despite lacking guidance from the California Air Resource Board (CARB), there is sufficient information for companies in scope of the regulations to start preparing disclosures.

Early preparation will make the process more comfortable for first time reporters and leave room to anchor strategic decisions within the organization.

For more background, you can download our comprehensive report on the CCAP.

Background: What Is CCAP Trying to Achieve?

The state of California has identified climate change as posing a global threat, and a threat to the state of California, its citizens, and its businesses. The senate bills underpinning the CCAP argue that “the long-term strength of global and local economies” depends on their ability to withstand climate-related risks1.

The purpose of the CCAP is to assess and reduce climate risk exposure, and to identify the measures that can be taken to increase the resilience of the state and the businesses operating within it.

The California legislature considers the current state of voluntary reporting inadequate and has therefore chosen to implement mandatory disclosure to “begin to address the climate crisis.”2

How to Comply with SB 253 (GHG Emissions Reporting Requirements)

Many companies were hoping for clearer disclosure requirements before the SB 253 regulation takes effect. CARB now indicates that official guidance, originally expected by July 1, will likely not be available until later in 2025.

Despite the lack of guidance, the requirements for complying with SB 253 in the first reporting year are reasonably clear. In December 2024, it was communicated that CARB will “exercise enforcement discretion”, if reporting entities show “good faith efforts”3 to disclose emissions following the guidance of the GHG Protocol.

That means that companies that are either already applying the GHG Protocol Corporate Standard, or start doing so now, will meet the disclosure requirements.

Challenges with SB 261 (Climate-Related Financial Risk Disclosures)

Compliance with SB 261 is complex, and CARB is still developing implementation details, including minimum reporting requirements. During a recent webinar, CARB sought input on whether to implement SB 261 through formal regulation or supplemental guidance, indicating that key decisions remain undecided. Despite this uncertainty, companies are still expected to publish their first SB 261 disclosures by January 2026.

Reporting Expectations: What We Know So Far

Covered entities are expected to report on climate-financial risk according to the recommendations provided by the Task Force on Climate-related Financial Disclosures (TCFD) or IFRS Sustainability Standard S2, which builds on TCFD recommendations. Reporting may also be conducted using other frameworks deemed equivalent to TCFD or IFRS S2 by CARB. Companies are expected to report “measures adopted to reduce and adapt” to climate risks defined as “material risk of harm to immediate and long-term financial outcomes due to physical and transition risk.”4 Organizations are expected to identify any gaps in their disclosures relative to the required standards and detail a plan for future improvement.

Which Reporting Framework Should I Use? TCFD vs ISSB

For companies new to climate-related financial disclosures, the TCFD recommendations offer a practical starting point. TCFD’s more focused scope allows organizations to build a foundation for future, more comprehensive reporting.

However, given the increasing sophistication of climate risk assessments and the broader alignment with IFRS S2 standard, companies anticipating reporting in multiple jurisdictions or seeking to demonstrate a deep understanding of their climate risk exposure may find the IFRS standards more suitable. As the regulatory landscape evolves, and market expectations rise, IFRS-aligned reporting will likely become the baseline expectation.

Companies subject to reporting regimes that cover equivalent requirements e.g. through laws in other jurisdiction, can use those disclosures.

How to Prepare for the January 2026 Deadline

The key question everyone is currently asking, is:

- What level of disclosure meets the minimum compliance threshold under SB 261?

As a voluntary framework, TCFD does not mandate full disclosure of all recommended disclosures, and many companies disclosing against its recommendations often chose which disclosures to report against selectively.

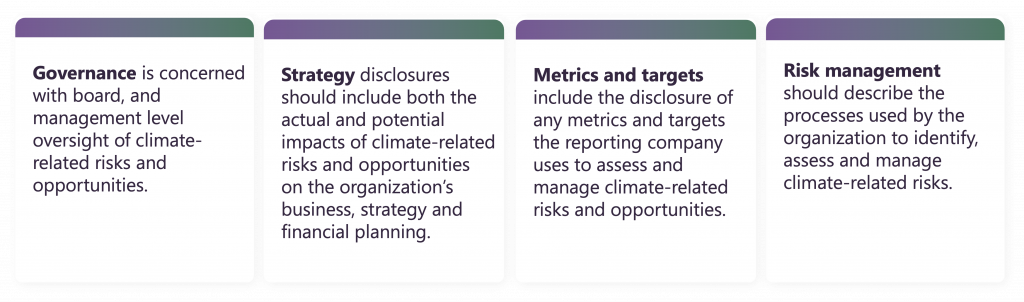

The disclosure requirements referred in SB 261 follow the foundational structure of the TCFD. Disclosures are split into four pillars: Governance, Strategy, Risk Management and Metrics and Targets.

For the first year of SB 261 compliance, reporting companies should, at minimum, disclose against all four pillars of the TCFD, with the intention of ensuring that relevant stakeholders, such as investors, have sufficient information to understand company’s risk exposure.

There is currently sufficient information to begin preparing disclosures, and companies will benefit from starting the process as soon as possible. Early preparation reduces stress and allows for consistent decision-making throughout the organization.