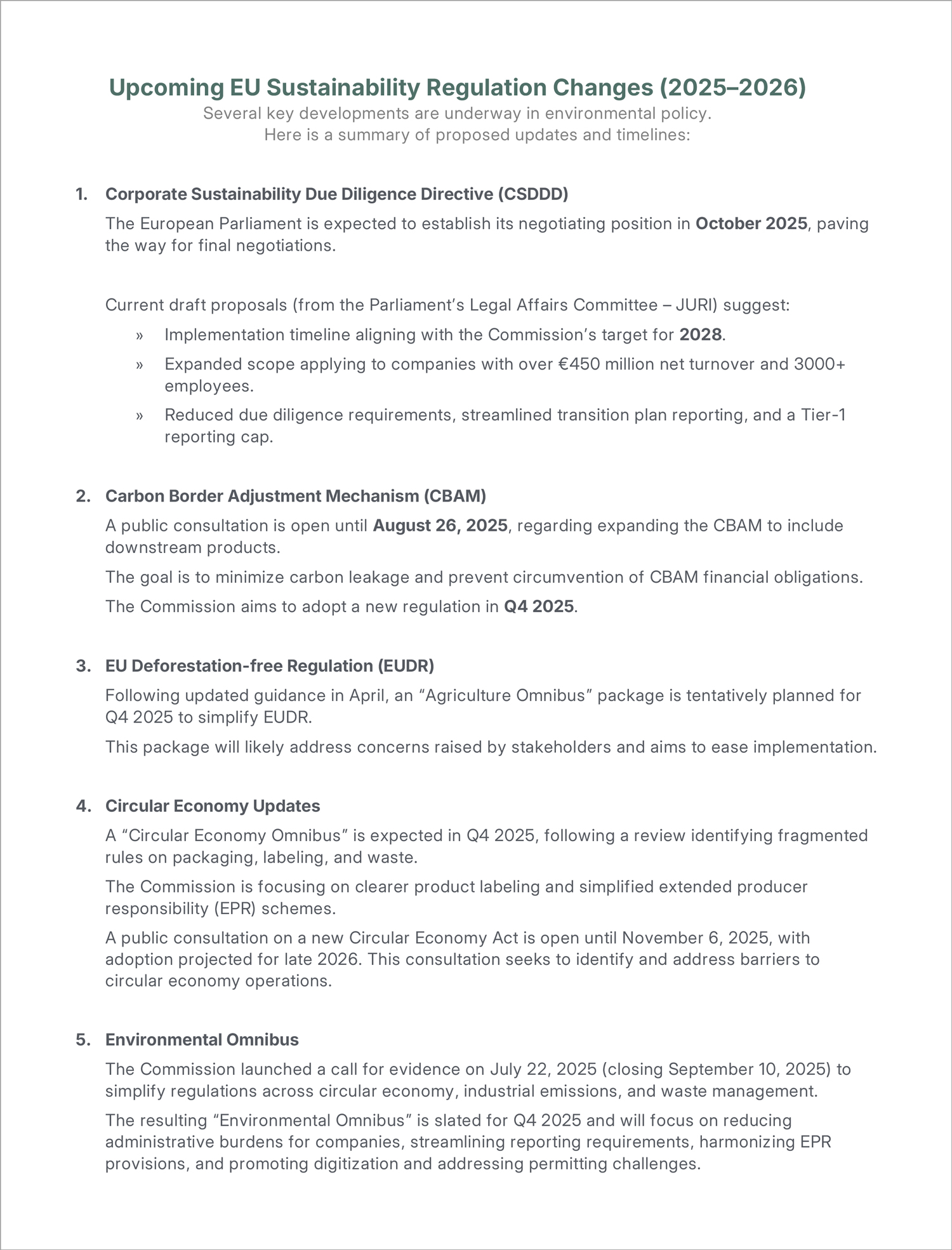

EU Sustainability Reporting Updates – July 2025

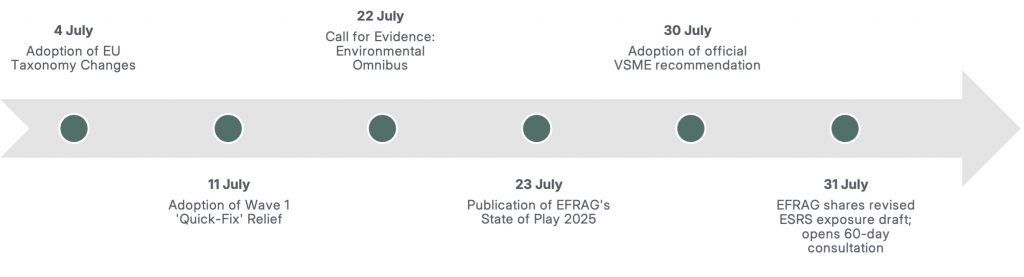

July was a significant month for European sustainability reporting, highlighted by the European Financial Reporting Advisory Group (EFRAG) releasing the long-awaited simplified European Sustainability Reporting Standards (ESRS) Exposure Draft on July 31. The EU Commission also adopted changes to the EU Taxonomy earlier in the month, alongside ‘quick-fix’ relief measures for the first wave of companies subject to the Corporate Sustainability Reporting Directive (CSRD). Beyond these, a “Call for Evidence” launched on July 22 sought input on potential simplifications of EU environmental regulations (the Environmental Omnibus), and EFRAG published its 2025 State of Play report and dashboard for Wave 1 ESRS reporting. The EU Commission officially adopted recommendations regarding the Voluntary Reporting Standards for SMEs (VSME) on July 30. Despite this progress, the final scope of the CSRD remains under negotiation and is expected to be clarified in the coming months.

CSRD Reporting Scope Updates and Ongoing Negotiations

Updated: July 2025

Uncertainty remains concerning the scope of the Corporate Sustainability Reporting Directive (CSRD) and the number of companies it will affect. The initial Omnibus proposal in February 2025 introduced a significant reduction in scope, applying the requirements to companies with over 1000 employees, over €50 million in net turnover, or over €25 million on the balance sheet. The proposed amendment would reduce the number of companies required to report by approximately 80%, from over 45,000 to around 9,000.

Since then, further thresholds have been proposed. In mid-June, the European Parliament´s Omnibus negotiator proposed a significant increase in the employee and turnover thresholds, and a week later, the Council of the EU announced its position. The proposals can be compared in the table below.

| Proposing Entity | Applicability Threshold |

| Original CSRD Scope | Wave 1: Large EU Public Interest Entities (PIEs) Large PIEs > 500 Employees Wave 2: Large EU Company Large companies with (2 out of 3) > 250 employees > EUR 50M net turnover > EUR 25M balance sheet Wave 3: Listed EU SMEs with (2 out of 3) Between 10 and 250 employees > EUR 700k net turnover > EUR 350k total assets |

| EU Commission Proposal (Omnibus) | > 1000 employees AND > EUR 50M net turnover OR > EUR 25M balance sheet |

| EU Council Proposal | > 1000 employees AND > EUR 450M net turnover |

| EU Parliament Draft (European People’s Party) |

> 3000 employees AND > EUR 450M net turnover |

Significant debate has focused on the varying proposed scopes for CSRD reporting and their potential impact on the number of companies required to report. A recent study by Rasche et al. demonstrated that the European People’s Party’s threshold of 3,000 employees and EUR 450 million in net turnover would reduce the number of companies in scope by 94% compared to the original CSRD provisions. Notably, all three proposals would represent a regression in scope from the previous mandatory EU reporting standard, the Non-financial Reporting Directive (NFRD), which is estimated to have captured approximately 11,000 companies.

Next, the Parliament needs to finalize its position before trilogue negotiations begin (between the Commission, Council, and Parliament) in October/November. The Content Directive, which officially amends the CSRD, is still expected to be adopted in December 2025 and take effect after transposition by Member States, anticipated to be completed by January 2027.

CSRD Wave 1 Reporting Relief Measures for 2025–2026

The Commission adopted a Delegated Act in mid-July to address challenges faced by Wave 1 companies – those beginning mandatory sustainability reporting this year for financial year 2024 results.

This measure provides relief because Wave 1 companies were not covered by the “Stop-the-Clock” Directive, adopted in April, which delayed reporting requirements for Waves 2 and 3 for two years.

Under this Delegated Act, Wave 1 reporters can omit certain phased-in provisions in their 2025 and 2026 financial year reporting, including anticipated financial effects of sustainability-related risks, Scope 3 greenhouse gas emissions, and standards like Biodiversity and Ecosystems (E4), as well as much of the social standards.

The amendments are subject to a two-month scrutiny period by the European Parliament and Council of the EU, beginning in mid-July. If no objections are raised, the amendments will take effect without the need for transposition into national laws.

ESRS Simplification: Reduced Disclosure and Materiality Requirements

On 31 July, EFRAG released the revised Drafts of the European Sustainability Reporting Standards (ESRS), resulting in significant simplification of reporting requirements. The total number of disclosures – both mandatory and voluntary has been reduced by 68%.

The revisions focus on providing companies with greater flexibility and reducing the complexity of reporting. Revisions include streamlining the double materiality assessment requirements and disclosures, reducing overlaps across the standards, clarifying the language and structure, and removing all voluntary disclosures. More specifically, these changes include:

- Reduced disclosure requirements: The revised standards move away from detailed narratives and prescriptive guidance, offering a more flexible approach to reporting on strategy, business models, value chain, governance, policies, actions and targets.

- Streamlined materiality assessments: The process for determining material sustainability topics has been simplified, emphasizing “fair representation” and user-focused information. The requirements promote more focus and proportionate reporting. Minimum Disclosure Requirements have been replaced by simpler General Disclosure Requirements.

- Alignment with international standards and increased clarity: All the voluntary disclosures have been deleted, language streamlined, and redundancies removed. The standards are more closely aligned with international frameworks like GRI, ISSB, and SASB. While EFRAG made significant efforts towards interoperability, the amended guidance indicates that there may be differences compared to other standards in some instances.

- Greater flexibility: Companies have more leeway in how they present information, including the option to include an executive summary, and new reliefs have been introduced regarding data quality and financial effects.

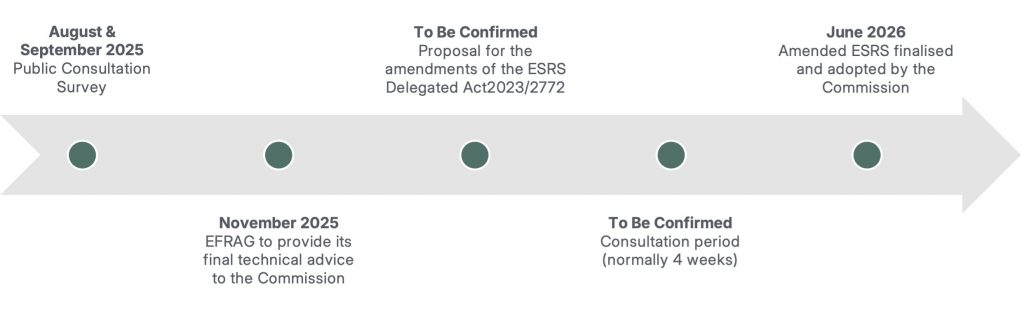

EFRAG has now launched a 60-day public consultation survey to gather feedback from stakeholders between July 31 and September 29, 2025. The feedback received will be incorporated into EFRAG´s final technical advice to be presented to the European Commission.

The implementation date of the proposed amendments is not yet confirmed, however Commissioner Albuquerque recently indicated that they hope to finalize the amendments to the ESRS Delegated Act before the end of the first semester 2026, depending on the omnibus legislative developments.

Until the revised ESRS Delegated Act takes effect, companies currently reporting under ESRS adopted in 2023 within the scope of the CSRD should continue to do so, taking into account the additional flexibility provided by the “stop-the-clock” and “quick fix” legislative acts.

Voluntary Sustainability Reporting Standard (VSME) for SMEs

On July 30, the European Commission adopted a Recommendation on voluntary sustainability reporting for small and medium-sized companies (SMEs). The Recommendation introduces the Voluntary Sustainability Reporting Standard for non-listed Micro-, Small-, and Medium-sized Enterprises (VSME), which is designed for entities with less than 250 employees and was released by EFRAG back in December 2024.

The VSME standard is structured into Basic and Comprehensive modules and is designed to help SMEs – those not currently required to report under the CSRD – respond to growing requests for sustainability information from larger businesses and financial institutions.

The Commission recommended the adoption of a voluntary standard for companies that will no longer be in scope for CSRD reporting (specifically, those with up to 1000 employees). The standard would be adopted via a delegated act and would align with the proposed value chain cap on information outlined in the omnibus proposal. The Commission intends to base this new standard on the VSME but states:

The content of the future voluntary reporting standard might differ from the current VSME Recommendation. The empowerment of the Commission to adopt a voluntary standard by means of a delegated act, and the timing of any such adoption, depends on the conclusion of negotiations between co-‑legislators on the omnibus simplification proposal. Today’s recommendation on a voluntary standard will be used as the basis for the future voluntary standard.

Comprehensive guidance accompanies the VSME standards, along with a range of resources to support SMEs in implementation.