Mapping Corporate Climate Commitments: Aligning Business Action with Global Climate Goals

Corporate climate ambition is rising—but how aligned are targets with global goals? Discover regional and sector trends in GHG reduction commitments ahead of COP30.

The third round of Nationally Determined Contributions (NDCs) – the central mechanism through which countries commit to climate action under the Paris Agreement – was originally due in February 2025, covering targets for 2035. Due to low submission rates, the deadline was informally extended to September 24, 2025, giving countries additional time to develop robust, high-quality plans ahead of COP30, which will take place in Belém, Brazil in November 2025. According to Climate Action Tracker, only 40 countries had submitted their NDCs as of September 23, representing 24.5% of global emissions and 16.6% of the global population. While the overall outlook on global commitments remains cautious, efforts to establish ambitious targets continue beyond the formal deadline.

Regional Trends in Corporate Climate Commitments & GHG Reduction Targets

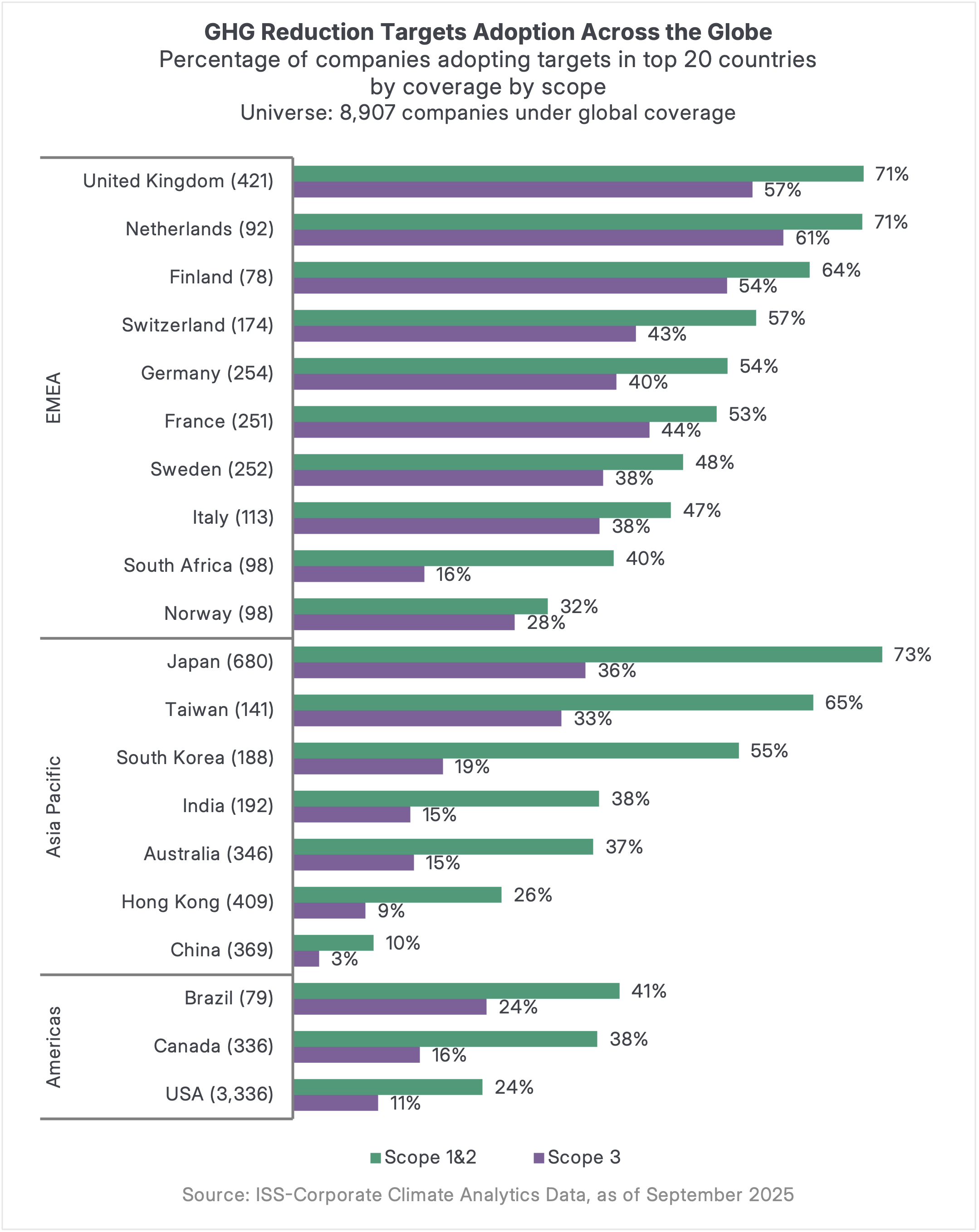

Against the backdrop of ongoing NDC negotiations and preparations for the COP30 summit, ISS-Corporate analyzed corporate disclosure data to assess the global prevalence of greenhouse gas (GHG) emissions reduction targets. The findings reveal significant variation across countries and regions, with companies in Europe and Asia Pacific showing more consistent commitments—particularly in setting Scope 1 & 2 and Scope 3 targets—compared to their counterparts in the Americas.

Within Europe, the United Kingdom, the Netherlands, and Finland stand out for their high levels of ambition, with most companies under coverage establishing targets across all scopes. In Asia, Japan, Taiwan, and South Korea lead the region in climate commitments, with the majority of firms setting Scope 1 & 2 reduction targets. However, Scope 3 targets remain less common, appearing at roughly half the rate of Scope 1 & 2 commitments in these markets.

In the United States, approximately 24% of companies under coverage have established Scope 1 & 2 emissions reduction targets, while 11% have set Scope 3 targets. Among large-cap companies – those with a market capitalization above $10 billion – these figures rise to 58% and 31%, respectively. While the higher rates among large caps are notable, it’s important to consider the broader context: the U.S. market includes a substantial number of small- and micro-cap companies, resulting in wider coverage and a more diverse corporate landscape compared to other regions. That said, even when controlling for company size, the adoption of GHG reduction targets by U.S. firms remains lower than in many other major markets.

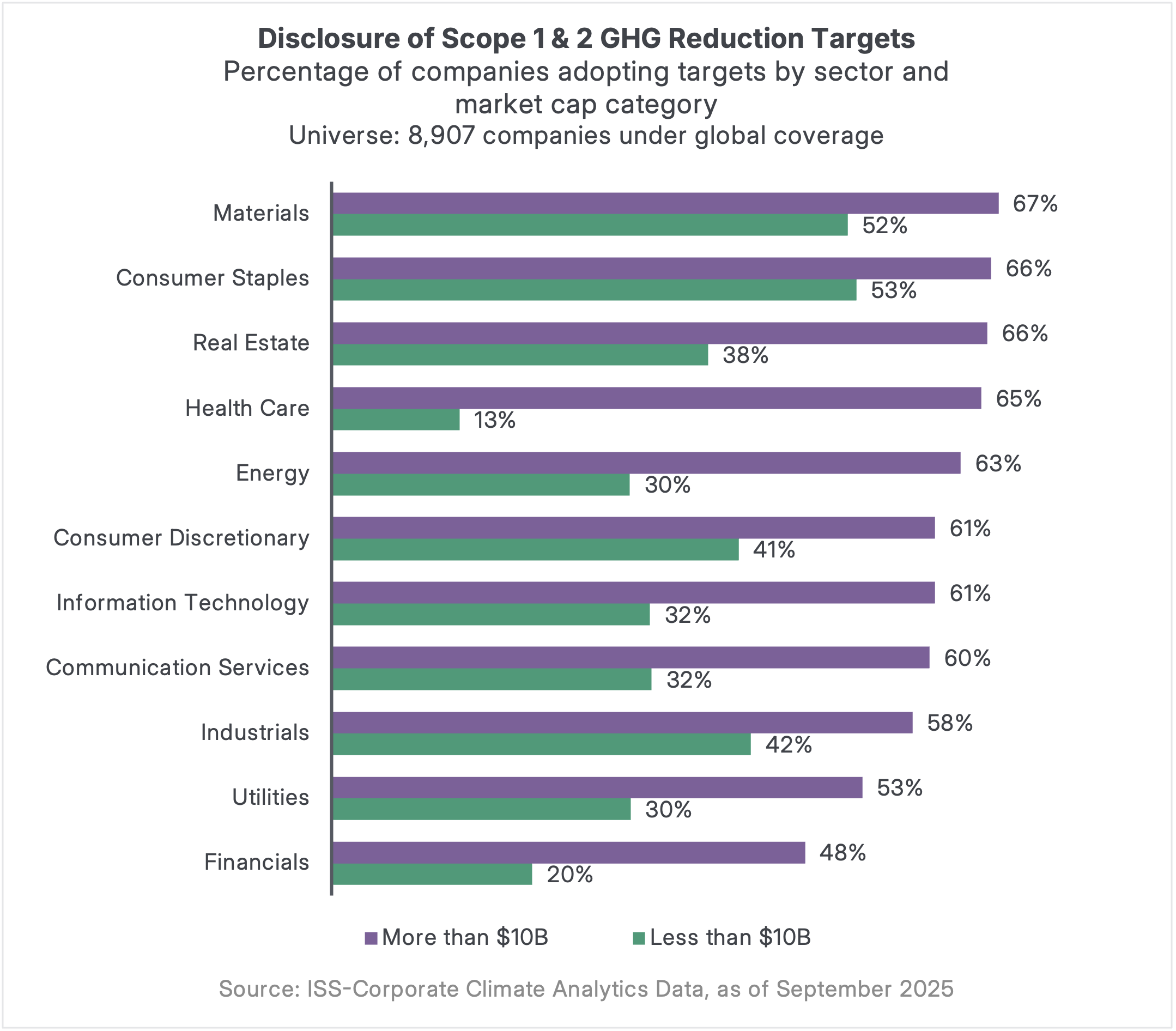

Sectoral Trends of Scope 1, 2 & 3 Emissions Reduction Targets

Building on regional differences, sector-level analysis reveals further nuances in how companies approach climate target-setting. An analysis of Scope 1 and 2 GHG reduction target adoption across sectors and market cap categories reveals notable patterns. Among large-cap companies (market capitalization above $10 billion), adoption rates are relatively consistent across sectors, with most exceeding 60%. Materials, Consumer Staples, and Real Estate lead the way, while Utilities (53%) and Financials (48%) fall just below the threshold.

In contrast, target adoption among smaller companies varies significantly by sector, reflecting differences in market cap composition. For instance, sectors like Health Care and Financials include a high proportion of small and micro-cap firms, which correlates with lower adoption rates—13% and 20%, respectively—compared to 65% and 48% among their large-cap counterparts. These disparities underscore the influence of company size and sector structure on climate target-setting behavior.

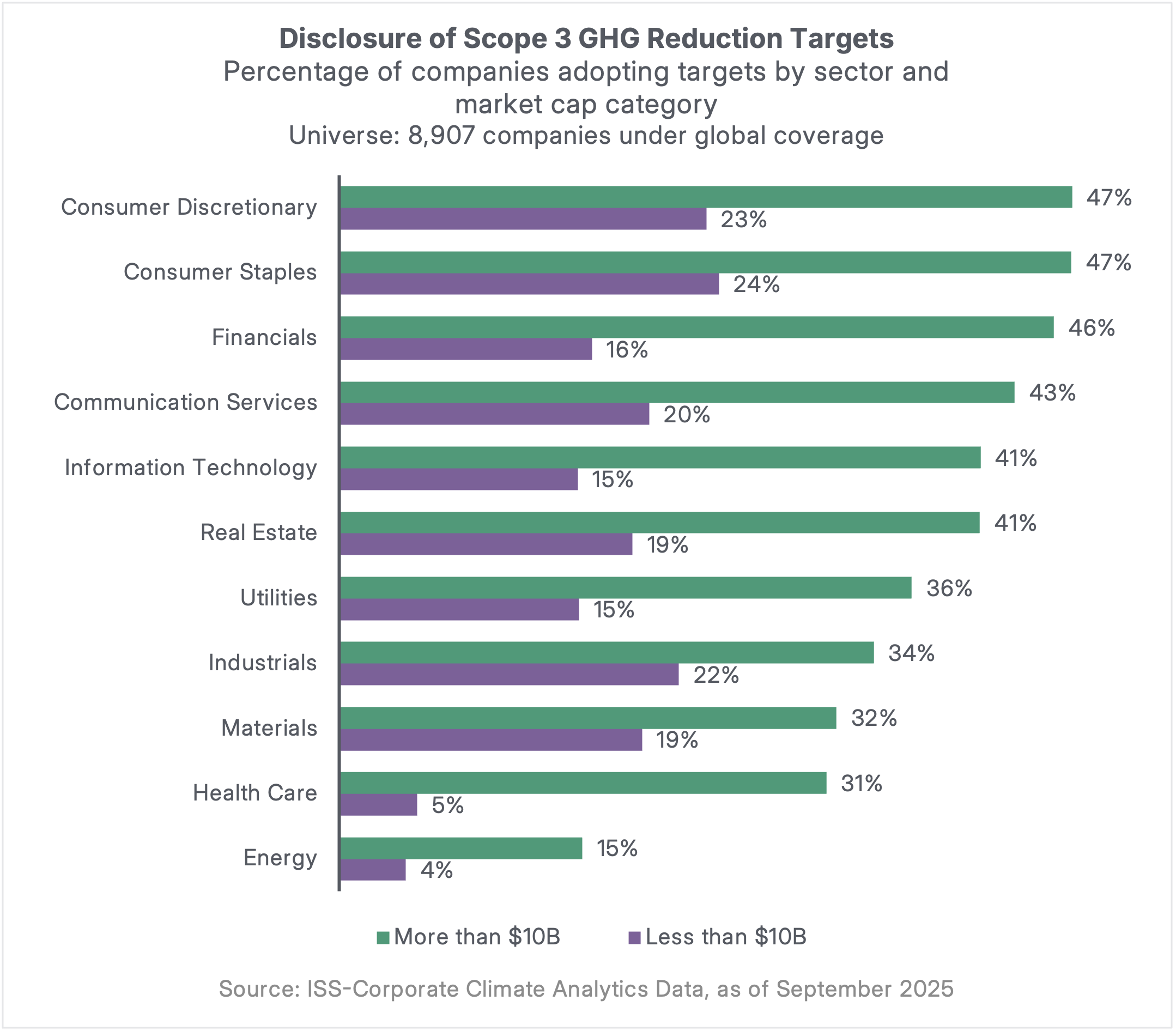

When examining Scope 3 GHG reduction targets, a more fragmented picture emerges, even among large-cap companies. Adoption rates vary significantly across sectors, with Consumer Discretionary (47%), Consumer Staples (47%), and Financials (46%) leading the way. Notably, Financials – previously among the low-performing sectors for Scope 1 and 2 targets – rank high for Scope 3, reflecting the materiality of financed emissions, which dominate the sector’s climate footprint. In contrast, sectors that showed strong adoption of Scope 1 and 2 targets – such as Materials, Health Care, and Energy – fall behind on Scope 3, with fewer than one-third of large-cap companies setting reduction goals. This disparity highlights the challenges of managing value chain emissions, particularly downstream impacts among Energy and Materials firms.

Strengthening Corporate Climate Action & Emissions Goals

As policymakers continue to negotiate climate targets in the lead-up to COP30, uncertainty persists – both in the policy space and in corporate climate practices. Despite potential setbacks, momentum remains strong. Companies across sectors and regions are actively setting new GHG reduction targets and refining existing commitments. In this evolving landscape, it is essential for firms not only to strengthen their climate programs but also to ensure that their goals are both realistic and achievable. Given the wide variation in target-setting practices across industries and geographies, benchmarking against peers and learning from sector leaders can provide valuable insights, helping companies align ambition with execution and contribute meaningfully to the global climate effort.