Getting Materiality Right: Challenges, Risks, and Best Practices

“Materiality assessments are vital, yet complex. Learn how to navigate stakeholder engagement, evolving standards, and group structures to build a resilient sustainability strategy.”

Materiality assessments are not new: for years, they have served as a fundamental tool for organizations seeking to identify and prioritize the sustainability issues most relevant to their business. Beyond informing reporting, they have played a strategic role – shaping decision-making, guiding resource allocation, and strengthening stakeholder relationships. By identifying issues that matter most, they enhance organizational resilience, stakeholder trust, and long-term value.

As sustainability becomes more central to business strategy, the importance of materiality assessments has grown. While recent developments in frameworks like the European Union’s European Sustainability Reporting Standards (ESRS) and the International Sustainability Standards Board’s Sustainability Disclosure Standards (ISSB-SDS) have formalized the practice, they have also raised the bar. They have introduced more rigorous expectations around identifying material sustainability topics, with the aim of creating a more consistent, comparable and forward-looking approach to sustainability disclosures.

While materiality assessments offer their strategic value, they are often complex and resource intensive. Practitioners frequently cite challenges such as time-consuming stakeholder engagement, methodological ambiguities, fragmented data, and difficulties with integrating results from complex group structures. Below, we explore these challenges in more detail and propose practical strategies for companies to address them.

Navigating Materiality Assessment Challenges

Solving Common Challenges in Materiality Assessments

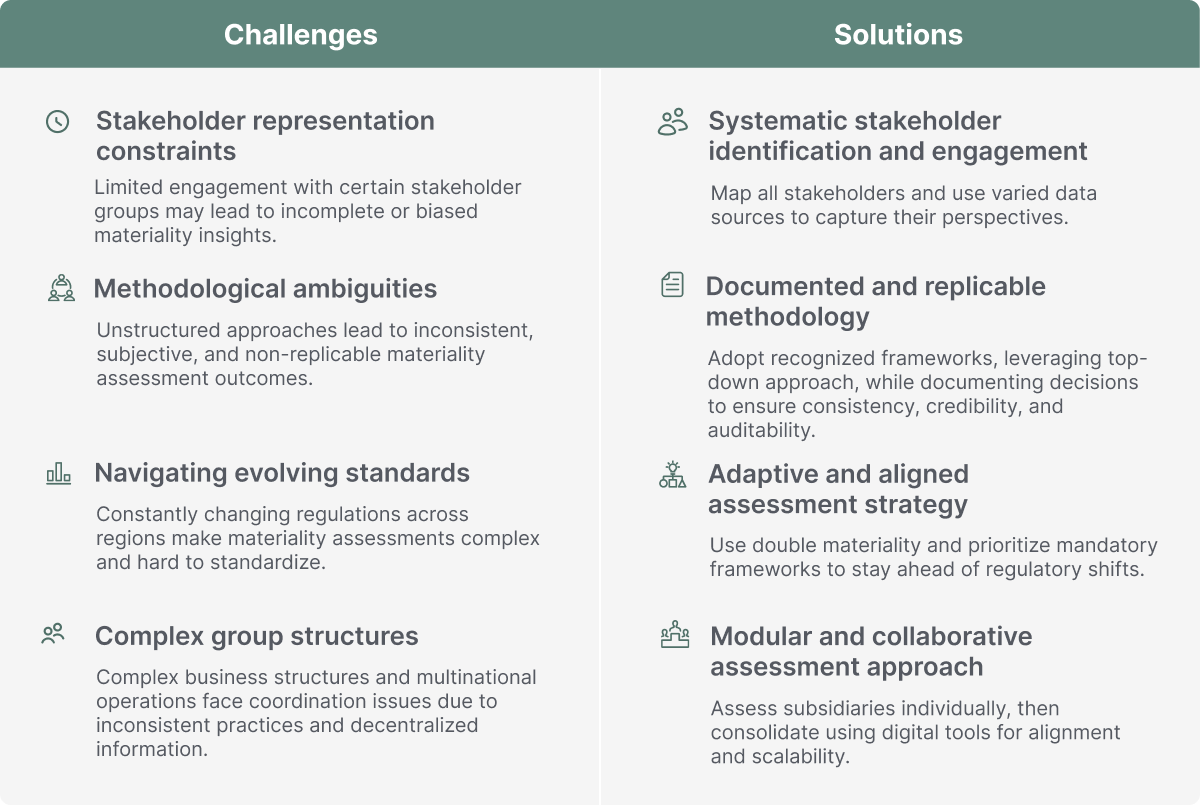

Stakeholder representation constraints

Engaging with a wide range of stakeholder groups is crucial yet often represents a significant challenge during materiality assessments. While companies commonly prioritize engagement with investors, customers, and employees, a truly comprehensive and credible assessment must also account for perspectives that are frequently overlooked – such as local communities and supply chain workers – whose experiences can reveal critical insights and risks. The omission of these groups not only stems from the difficulties associated with obtaining meaningful feedback, but also from practical barriers such as language differences and lack of established communication channels. This may result in an incomplete or potentially biased understanding of the company’s material topics and related impacts, risks and opportunities (IROs).

To address this issue, companies may benefit from a systematic stakeholder identification process, beginning with a compilation of all internal and external stakeholders. Particular attention should then be directed towards those stakeholders along the value chain (both upstream and downstream) who are or may be affected by the company’s operations, products and/or services, either positively or negatively.

Recognizing that direct engagement can be constrained, a multi-faceted approach to data collection is key. This includes employing different types of data sources, prioritizing direct consultation where feasible, and supplementing with proxy data when direct access is limited. For instance, utilizing data from a Non-Governmental Organization with established relationships with local communities may serve as a proxy for that community’s views on material topics, and speaking with a trade union representative may provide insights into the priorities of a particular industry’s workforce within the value chain.

A comprehensive stakeholder engagement program is fundamental to ensuring the accuracy and relevance of the materiality assessment by capturing insights from the stakeholders most pertinent to the organization’s sustainability context. This targeted engagement enhances the organization’s ability to make informed decisions and manage risks proactively.

Methodological ambiguities

Methodological ambiguity is another challenge practitioners face when conducting materiality assessments. Many companies lack a standardized or well-documented approach for evaluating and prioritizing sustainability topics, which often leads to inconsistent results. In the absence of a structured approach, teams tend to rely on personal judgement without clear documentation of the rationale behind decisions, resulting in subjective outputs that may vary widely across reporting cycles. This hinders the replicability of the assessment and may undermine its credibility and limit its auditability.

To address these challenges, companies may consider adopting existing approaches for assessing materiality, such as those established in reporting frameworks like the Global Reporting Initiative (GRI), IFRS and ESRS. These frameworks recommend starting with understanding the company’s business model, strategy, and value chain, and then layering in stakeholder perspectives and data as needed to assess the materiality of topics.

Explore expectations and best practices for materiality assessments in this related article

To identify material topics, the most recent version of the Exposure Draft for the Amended ESRS 1 recommends using a “top-down” approach, by which the company identifies material topics first, and then material IROs related to those topics. Following this initial step, the company may engage with stakeholders to assess the severity and likelihood of the IROs. The revised standards highlight how “[a]dopting a top-down approach may be more pragmatic and reduce the complexity of the process,”[1] ultimately leading to outcomes that are just as decision-useful as those produced by more complex and resource-intensive methods.

While frameworks and standards provide a structure for materiality assessments, it is considered best practice to document all decisions made during the process. Documenting how the material topics were determined, who approved of them, the stakeholders that were engaged, who was involved in the assessment of IROs, among others, can be helpful when trying to replicate the assessment in future reporting periods, as well as supporting any auditability efforts.

Navigating evolving standards

Multinational companies must navigate a complex patchwork of requirements across geographies, such as the ESRS in Europe, the California Climate Rules (SB-253 and SB-261) in the United States, and the implementation of the ISSB-SDS in the Americas and Asia Pacific. These regulations and reporting frameworks are constantly evolving, posing a challenge for practitioners to remain current. Consequently, acknowledging overlaps in regulatory requirements across geographies is crucial.

While materiality assessments have gained renewed attention, their foundational principles have long been established. International standards such as the United Nations Guiding Principles on Business and Human Rights (UNGPs) and the OECD Guidelines for Multinational Enterprises have consistently emphasized the importance of identifying and addressing the most significant impacts businesses have on people and the environment and provide guidance on prioritizing issues based on severity and likelihood.

Therefore, sustainability-related materiality is a well-established practice rooted in existing due diligence processes and responsible business conduct. The recent evolution lies in the growing expectation for standardized, transparent, and data-driven application of these principles, reflecting a movement toward harmonization and enhanced quality in sustainability reporting.

To proactively manage this evolving landscape, companies benefit from a flexible and forward-looking approach to materiality assessments. Utilizing a double materiality lens (considering both a company’s sustainability impacts and associated financial risks and opportunities) provides a solid foundation for disclosures aligned with multiple frameworks. Prioritizing mandatory requirements while selectively aligning with additional voluntary frameworks, where relevant, enables organizations to build a robust and adaptable reporting strategy. Over time, iterative refinement of the materiality process helps companies stay ahead of regulatory shifts.

Complex group structures

Organizations with multinational operations or complex group structures often struggle with conducting materiality assessments due to fragmented data, inconsistent application of sustainability criteria, and different reporting practices across subsidiaries. These complexities create coordination challenges and hinder the consolidation of insights into a unified report.

A modular approach can simplify this process. Conducting individual materiality assessments for each subsidiary allows the consideration of company-specific context. By treating each unit as a building block, companies are enabled to scale their assessments more effectively, and aggregate findings into a coherent, enterprise-wide materiality matrix.

Effective implementation may require leveraging digital collaboration platforms that enable asynchronous data input, real-time feedback, and centralized documentation. Doing so will further streamline coordination and improve alignment across the organization.

The importance of getting materiality right

Without a clearly defined materiality lens, decision-making across teams may lack cohesion, leading to conflicting priorities, inefficient resource allocation, and weakened stakeholder communications. If challenges like the ones discussed above are not addressed appropriately, the company may face risks, such as:

- Regulatory and legal exposure: Overlooking negative impacts exposes companies to regulatory penalties and potential legal action, which can lead to financial implications and reputational damage.

- Operational and financial vulnerability: Similarly, missing key sustainability-related risks may affect operational performance and access to credit. Without a robust materiality assessment process in place, companies may be ill-prepared for potential disruptions caused by environmental factors, social issues, and other external pressures. These disruptions can impact not only direct operations but also supply chain continuity and overall business resilience.

- Strategic and innovation setbacks: An incomplete assessment of sustainability-related opportunities may result in missed chances for growth, innovation, and competitive differentiation.

- Misallocation of resources: Without a solid understanding of materiality, companies are likely to dedicate resources (both time and money) to sustainability initiatives that are not impactful or underinvest in areas critical to business’ success.

- Inaccurate reporting and investor distrust: Investors rely on transparent and relevant disclosures to inform their decision-making. A poorly designed or insufficiently rigorous materiality assessment may lead to underreporting or overreporting of key material issues. Such misalignment can erode investor trust and hinder access to capital.

While these challenges and risks are real, they are not insurmountable. A data-enabled materiality assessment provides companies with a roadmap and compass to guide their sustainability strategy. Identifying potential sustainability risks and opportunities that may financially impact the company, as well as how the company may impact people and the environment, can inform strategy development, target-setting, and reporting. The findings of a materiality assessment can also enable companies to gain necessary internal support and resources for developing key components of their sustainability programs.