Financing Climate Change Adaptation: Turning Risk into Resilience

Adaptation finance is accelerating, with corporate issuers and new taxonomies reshaping how climate resilience is funded amid global volatility.

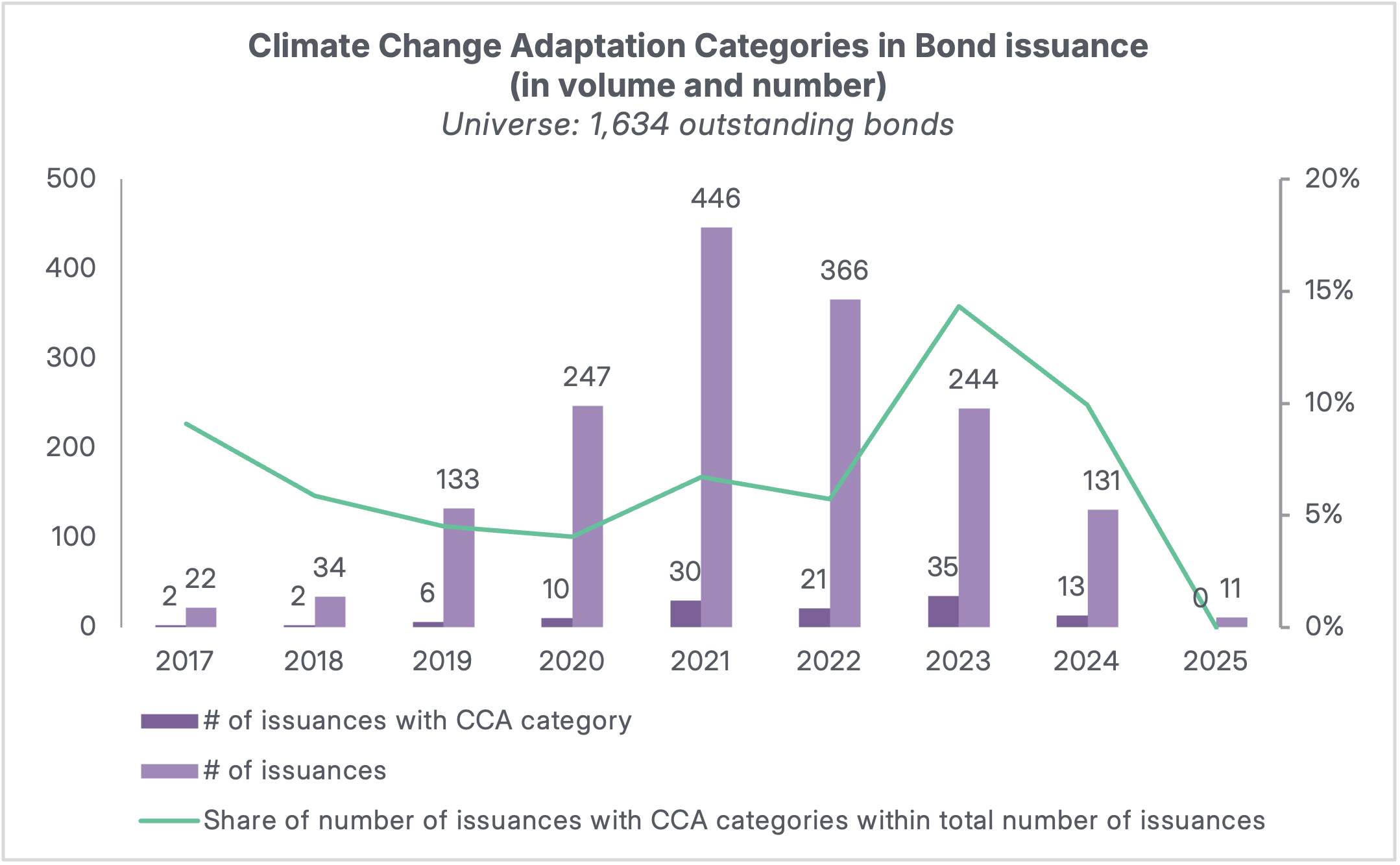

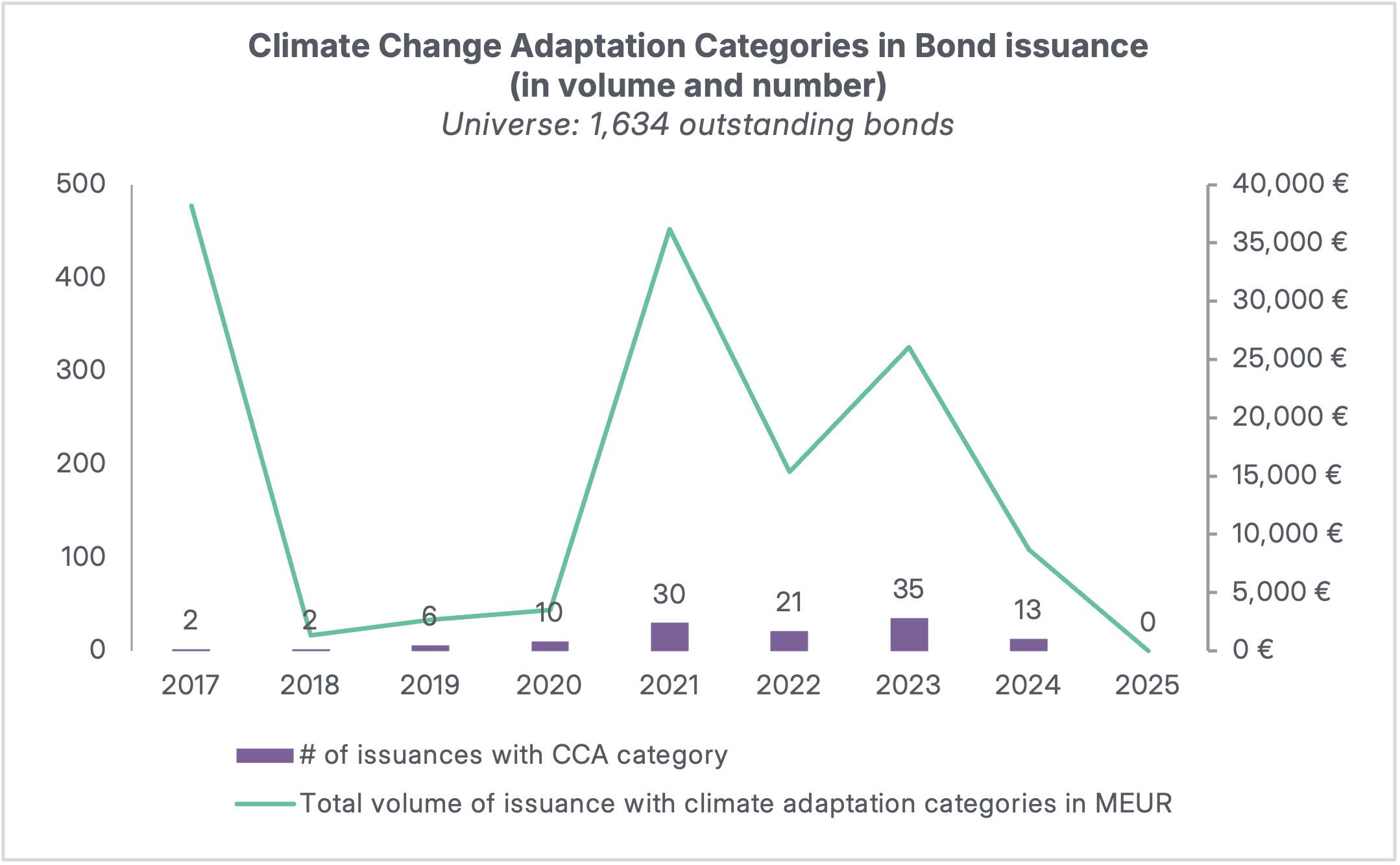

The emergence of adaptation bonds, along with a growing emphasis on adaptation within sustainable finance taxonomies, reflects increasing market recognition of the importance of business resilience to climate change. This shift is backed by compelling data: according to the Environmental Finance database, the number of bonds with a climate change adaptation (CCA) category rose from just 39 in 2017 to 601 in 2024, more than a fourteen-fold increase. Issuance volumes surged from €23 billion to nearly €268 billion, underscoring the growing financial commitment to climate resilience.

Anchored in Articles 2 and 7 of the Paris Agreement, adaptation finance [1] is positioned not only as a tool for climate resilience but also as a lever for sustainable development and poverty eradication. Supporting this view, recent research from the World Resources Institute shows that every dollar invested in adaptation and resilience yields over ten dollars in long-term benefits, ranging from avoided losses and economic gains to broader social and environmental impacts. [2] This underscores the strategic and economic imperative of scaling adaptation finance.

ISS-Corporate analyzed the evolution of climate change adaptation financing through its Sustainable Bond Rating database, which comprises 1,634 outstanding green, social, and sustainability bonds (i.e. bonds that have been issued and remain active in the market until maturity or repayment) between 2017 and April 2025. The database is built on post-issuance data. This insight piece examines how adaptation finance is gaining momentum, including the sectors and instruments driving this growth shift, and the challenges that remain. It also highlights emerging trends and expectations for the future of adaptation finance.

Adaptation Finance Gains Momentum, but Market Volatility Remains

Recent developments in the sustainable finance market, such as Japan’s €300M flood protection bond, Australia’s two-tier adaptation taxonomy released in June 2025, and the Asian Infrastructure Investment Bank’s (AIIB) AUD 500M climate-resilient infrastructure bond, signal growing institutional interest in mainstreaming adaptation finance.

ISS-Corporate’s data shows a rising trend in the inclusion of climate change adaptation categories in bond issuances, with notable inflection points in 2021 and 2023. These categories encompass a diverse range of activities aimed at improving climate resilience, including warning systems and emergency preparedness activities, preventive climate change adaptation solutions such as asset relocation or protection against natural disasters (i.e., climate-proofing water supply infrastructure and increasing embankment heights), as well as innovative adaptation technologies and solutions (like climate-resilient crop varieties). In those years, issuances related to climate change adaptation have tripled, increasing by 67% and outpacing the growth of the broader bond market. Issuance volume reached nearly €35 billion in 2021, with 30 transactions, and remained strong in 2023 with 35 issuances, despite a smaller total volume. This momentum is supported by emerging instruments such as catastrophe bonds and debt-for-nature swaps, alongside newly developed frameworks like the Climate Bonds Initiative’s Resilience Taxonomy.

However, the trend is not linear. Following early activity dominated by large sovereign or supra-national issuances in 2017, notable France’s 36 billion EUR Green Obligation Assimilable du Trésor (OAT), the market experienced volatility, with sharp declines in 2018 and again in 2024–2025, where issuance activity nearly collapsed, primarily due to a significant drop in global green, social, sustainable and sustainability-linked (GSS+) issuance volumes.

Corporate Participation Expands, but Sectoral Engagement Is Uneven

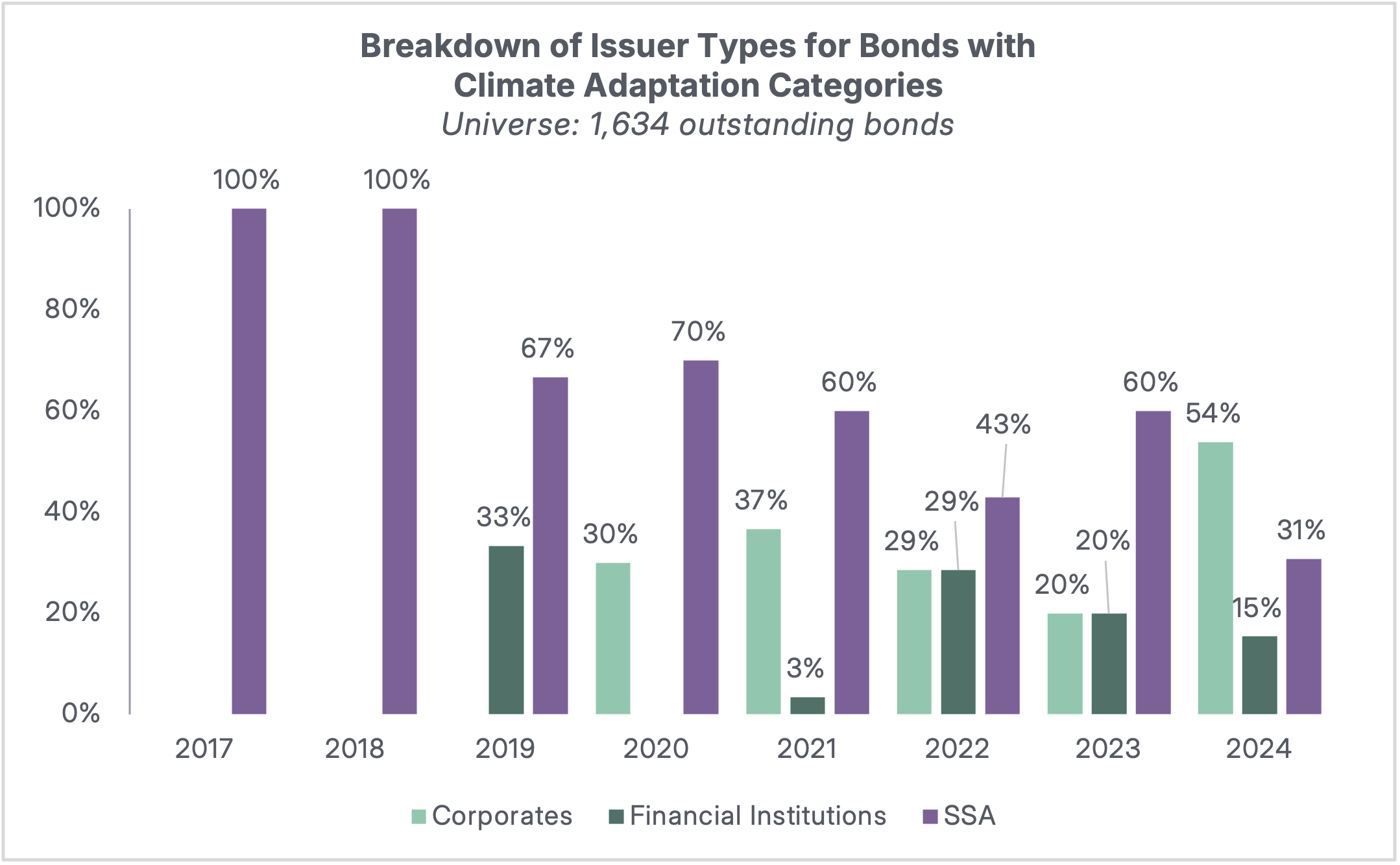

From 2020 to 2024, corporate issuers began playing a more prominent role in adaptation finance. In 2024, corporates represented 54% of adaptation-related bonds, surpassing Supra Sovereign Agencies (SSAs) for the first time. SSAs comprise supranational organizations mandated to advance public policy goals, sub-sovereign entities such as regional or municipal authorities, and agencies which are specialized public institutions (i.e., export credit agencies). This shift in corporate activities may be linked to different overlapping factors. Natural disasters triggered global insured losses of over $100 billion in the first half of 2025 alone, the second-highest figure since 2011. These mounting costs have made climate risk a material financial concern for corporates, prompting investment in resilience. Additionally, regulatory frameworks such as the IFRS sustainability standards are increasingly requiring companies to disclose climate risks and adaptation strategies, further incentivizing the use of adaptation-themed financial instruments.

However, sectoral participation remains concentrated. Only a handful of sectors, such as Utilities, Real Estate, and Transportation, have actively integrated adaptation themes into their bond frameworks. This may be partly due to the fact that regulated sectors like utilities tend to be more advanced in developing adaptation plans. Insurance companies, which fall under financial services, also play a natural role in adaptation finance, given their mandate to protect against climate-related financial risks. Yet, even within these sectors, corporate readiness remains modest.

Barriers to broader private sector engagement include: [3]

Lack of a shared market language: Unlike mitigation, which benefits from clear and widely adopted metrics such as CO₂ reductions, adaptation lacks a standardized taxonomy and success indicators. This absence of common definitions makes it challenging to determine what counts as a credible adaptation investment or to benchmark outcomes across projects and geographies.

Difficulty in pricing adaptation investments arises from two key factors: first, these projects often deliver benefits mainly through avoided losses rather than predictable revenue streams; second, the absence of detailed, reliable data on physical climate risks makes accurate valuation and risk-adjusted pricing challenging.

Misalignment between long-term adaptation timelines and short-term return expectations. Adaptation measures, such as climate-proofing infrastructure or deploying resilient agricultural systems, typically involve long investment horizons, often spanning decades. These timelines conflict with the short-term performance cycles of many corporate and institutional investors, which focus on quarterly or annual returns. Regulatory frameworks such as Basel III and Solvency II further exacerbate this issue by imposing capital charges on illiquid, long-duration assets, making adaptation projects less appealing for banks and insurers.

Geographic Disparities Highlight Institutional Gaps

Adaptation finance remains concentrated in high-income countries, excluding multilateral development banks. This geographic skew contrasts with the urgent needs of low-income and developing economies, where adaptation requirements exceed 1% of GDP annually—four times the global average, according to the IMF.[4]

This pattern reflects disparities in institutional capacity, regulatory frameworks, and investor demand for climate-aligned instruments.

Source: ISS-ESG Sustainable Bond Rating database

The Future of Adaptation Finance: Innovation, Alignment, and Strategic Relevance

Despite persistent challenges, market signals suggest that adaptation finance is entering a new stage of innovation and strategic importance. Standardized frameworks, dedicated instruments, and improved disclosures are helping to build a common understanding of adaptation finance.

ISS-Corporate’s Role in Supporting Adaptation Finance

ISS-Corporate is well-positioned to support clients in navigating this evolving landscape through:

- Use of Proceeds Second Party Opinions (SPOs)

- Alignment assessments with emerging taxonomies (e.g., Australia’s adaptation classification system)

Footnotes

[1] Adaptation finance involves supporting individuals, companies, and sovereign states in preparing for the physical impacts of climate change, such as floods, heatwaves, and rising sea levels.

[2] World Resources Institute, Strengthening the investment case for climate adaptation: A triple divide approach, June 2025, Strengthening the Investment Case for Climate Adaptation: A Triple Dividend Approach | World Resources Institute

[3] International Chamber of Commerce, The role of the private sector in climate adaptation, https://iccwbo.org/news-publications/policies-reports/how-to-scale-private-finance-for-adaptation-and-unlock-new-business-opportunities/

[4] International Monetary Fund, Poor and Vulnerable Countries need support to adapt to climate change, Poor and Vulnerable Countries Need Support to Adapt to Climate Change