ISS-Corporate Leads Reviews as EU GBS Gains Traction

The EU Green Bond Standard is gaining momentum—oversubscriptions, greeniums, and growing issuer confidence signal a strong future for sustainable finance.

The European Green Bond Standard (EU GBS) came into force on December 21, 2024, marking a significant milestone for EU’s commitment to sustainable finance. Aiming to enhance transparency, credibility, and comparability in green bond markets, the EU GBS sets rigorous requirements for issuers, including alignment of use of proceeds with the EU taxonomy and mandatory pre- and post-issuance disclosures verified by external reviewers.

A Strong Start for EU GBS in 2025

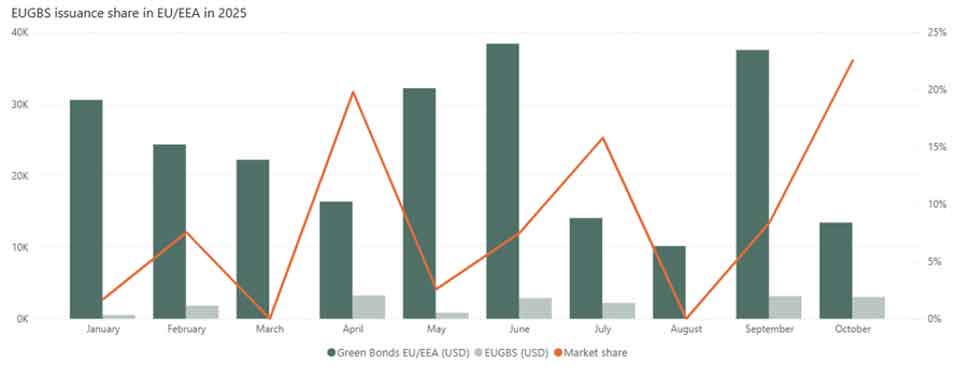

The year started with three issuances from A2A, Île-de-France Mobilités and ABN AMRO, totalling 2.25bn Euros, met with high investor enthusiasm demonstrated by the high levels of oversubscription. April marked the first issuance of EIB of 3bn Euros, which was 13.4 times oversubscribed. 10 further corporate issuers joined starting May[1] , two municipal issuers[2] , one more financial institution[3] and the first sovereign issuer (the Kingdom of Denmark[4] ). All offerings seen to date were significantly oversubscribed and several issuances saw the presence of greeniums, emphasizing the high demand for the “gold standard” bonds. According to ISS-Corporate calculations, 7% of all green bonds issued in the EU/EEA area this year had the European Green Bond (EuGB) label.[5]

Source: Environmental Finance data (efdata.org) downloaded on 18.10, complemented by ISS-Corporate database, own calculations

According to internal research, 25 factsheets were published up to October 18, 2025, 9 of which received a pre-issuance review by ISS-Corporate, making ISS-Corporate the lead External Reviewer in this space.

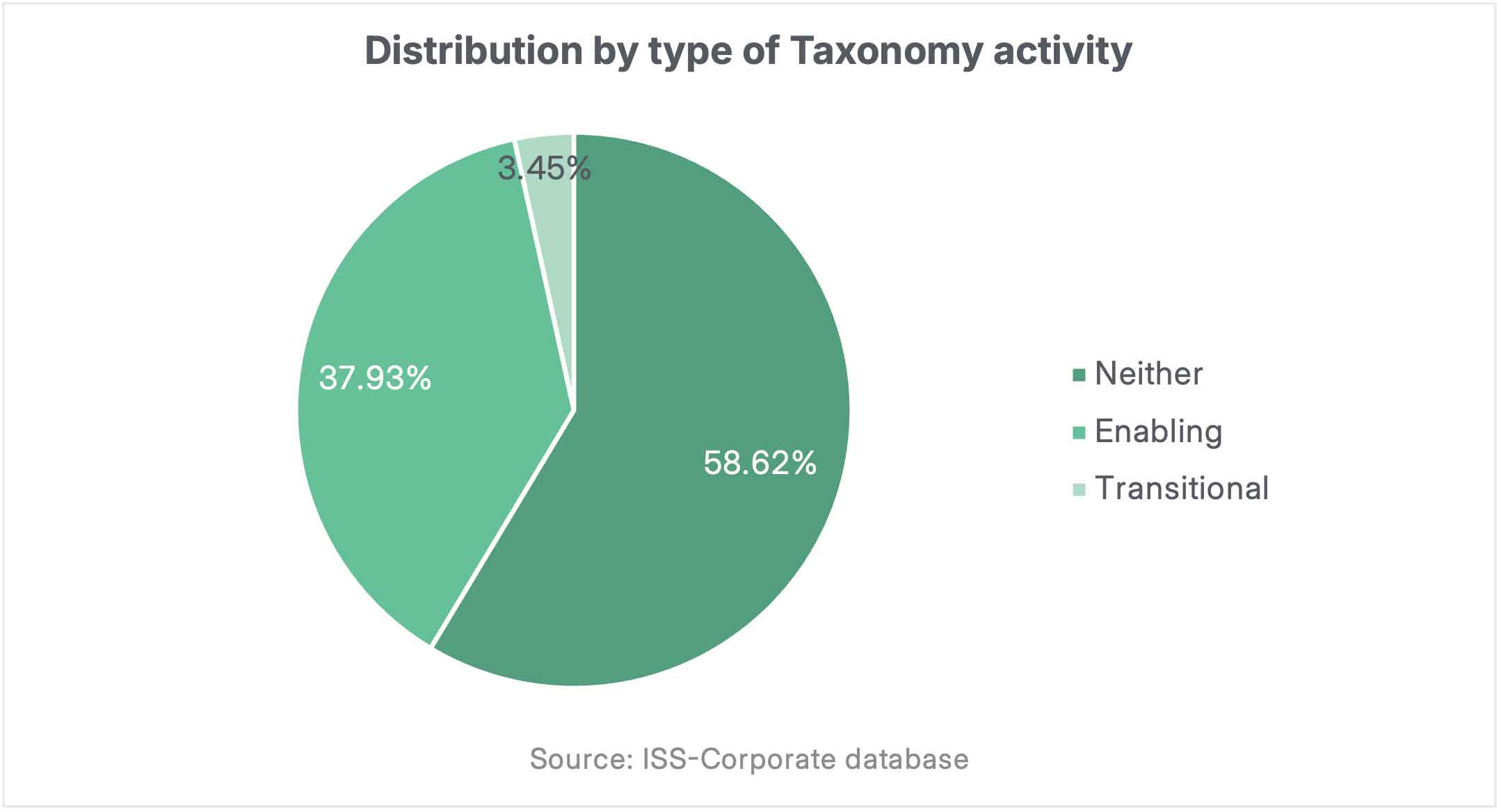

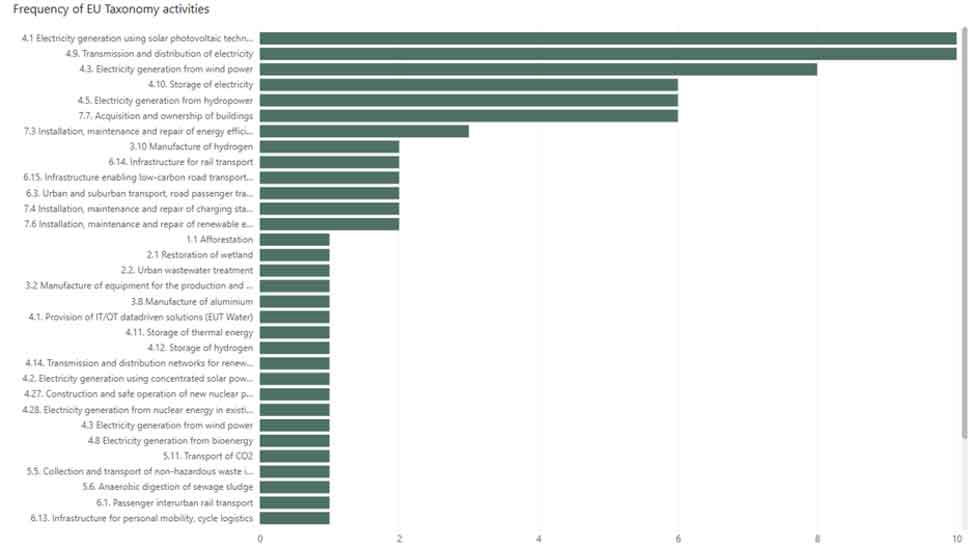

All except two of the entities that have published factsheets are experienced, frequent issuers of green bonds, following ICMA’s Green Bond Principles. Several of these documents also affirm that the European Green Bonds will align with the Green Bond Principles. Most of these entities are corporates active in the energy sector, real estate, transportation. As well, five commercial banks published factsheets. A large majority of EU Taxonomy activities to be financed are enabling activities, with activities 4.9 Transmission and distribution of electricity and 4.10. Storage of electricity being the most frequently mentioned. Among the activities that are neither transitional nor enabling, the most frequent are 4.1 Electricity generation using solar photovoltaic technology, 4.3. Electricity generation from wind power, 4.5. Electricity generation from hydropower and 7.7. Acquisition and ownership of buildings. Proceeds will mostly be used to refinance these activities.

The illustrations below refer to all European Green Bond factsheets published up to October 18.

Source: ISS-Corporate database

Looking Ahead: Confidence Grows Among Issuers

During 2025, several European Green Bond Factsheets reviewed by ISS-Corporate remained confidential for several months, while the respective clients waited as they became convinced of the benefits of the EuGB label. This approach appears to have faded, suggesting that the advantages for issuers are now more evident. Furthermore, a notable number of factsheets have been published in the recent weeks (from institutions such as Argenta, ASN Bank, Deutsche KreditBank, Latvenergo and REN – Redes Energéticas Nacionais), pointing at more issuers and greater volumes at the horizon.

Footnotes

[1] Covivio, EDP, Elenia, Elia Transmission Belgium, Eurogrid, Iberdrola, Norsk Hydro, Snam, TVO, Terna

[2] Community of Madrid and Rīgas ūdens

[3] BancoBPM

[4] A notable particularity in relation to this European Green Bond is the parallel issuance of a “twin” conventional bond having the same financial characteristics. Investors gave at any time the option to change the green bond to the conventional bond. This approach was taken to address any concerns regarding the liquidity of the green bond market. Additionally, this concept it helpful to demonstrate the presence of greenium.

[5] Sustainability bonds which may also have a green component were not considered in this calculation.