UK SRS Published: A New Chapter for Sustainability Reporting

UK SRS S1 and S2 are now final, with climate disclosures mandatory from 2027 and phased expansion beyond climate thereafter.

The UK Department for Business and Trade published the final UK Sustainability Reporting Standards (UK SRS) on February 25, 2026. The long-anticipated standards – UK SRS S1 and S2 – mark the formal endorsement of the international baseline developed by the ISSB, adapted for the UK market.

Overview of the Final UK SRS S1 and S2

The release follows extensive consultation throughout 2025, culminating in a framework now available for organisations to adopt voluntarily. The government has formally approved two standards that enable any UK entity to begin reporting under the framework immediately:

-

- UK SRS S1 – the general requirements for sustainability-related financial disclosures

- UK SRS S2 – the climate-related financial disclosures

The Financial Conduct Authority is consulting on mandatory adoption

Although the standards are ready for use now, the move towards mandatory adoption will unfold in phases. The Financial Conduct Authority (FCA) is consulting on changes to the UK Listing Rules (UKLR) to incorporate the new framework as the means to report on climate-related risks and opportunities, where TCFD reporting is currently required. Consultation closes on March 20, 2026.

Under current proposals, UK-incorporated listed companies would begin reporting against UK SRS S2 – and the relevant parts of S1 – for accounting periods starting on or after 1 January 2027. Initially, the reporting requirements would cover climate-only disclosures, with Scope 3 emissions and information about sustainability-related risks and opportunities beyond climate subject to a comply or explain approach from accounting periods beginning on or after 1 January 2028 and 2029, respectively.

In addition, the government plans further consultation later this year on whether to bring certain private companies into scope through the Companies Act 2006 (CA 2006). Depending on the consultation outcome, mandatory sustainability disclosures could eventually extend beyond listed entities.

In practical terms, companies captured in the FCA’s proposals would be expected to deliver their first UK‑SRS aligned reports in 2028, covering the 2027 financial year.

Key differences between the IFRS SDS and the UK SRS

The UK SRS are aligned with IFRS S1 and S2 to provide UK companies with a consistent reporting structure. However, the UK has made targeted modifications to tailor the framework to suit local needs. The main differences include:

-

- A reporting entity “may” rather than “shall” consider SASB standards when reporting.

- Timings have been removed for temporary reliefs (these may be re-introduced when the reporting schedule has been mandated).

- The option to publish sustainability disclosures after the financial statements has been removed, requiring sustainability information to be reported at the same time as the financial statements.

- Entities relying on transitional reliefs may not make an unqualified statement of compliance with the UK SRS and are required to clearly disclose and explain the reliefs applied.

- Financial institutions may report financed emissions using data from a different reporting period, provided additional disclosures are made explaining the timing difference and its implications.

The UK’s Existing Climate Disclosure Landscape

Before considering the implications of the UK SRS, it is worth noting that UK companies start from a relatively strong foundation in climate-related reporting. Following several years of TCFD-aligned requirements, disclosure levels are already high: 97% of UK companies report climate change as a business risk in their annual or financial statements, and 91% publish TCFD-aligned disclosures, either within the annual report or in a standalone TCFD report.

This strong baseline reflects well-established governance and risk assessment practices and provides important continuity as reporting expectations evolve. Because the UK SRS S2 builds directly on the architecture of TCFD, many organisations already have the core elements in place. What the UK SRS now requires is a deepening of disclosures – particularly around the quantification of transition actions, anticipated financial effects, and clearer connectivity to financial statements.

The UK’s Existing Climate Disclosure Landscape

The government has yet to publish its response to the June 2025 consultation on climate transition plans, formalising whether they will become mandatory and for which entities.

In the meantime, UK SRS S2 already requires companies to disclose any transition plans they have, including key assumptions and dependencies. In addition, entities must provide material information on climate-related risks and opportunities that could reasonably affect their prospects, including how they mitigate and adapt to transition and physical risks.

The FCA, has proposed a “disclose or explain” approach rather than mandating transition plans, meaning listed companies must state whether they have published one and, if not, explain why.

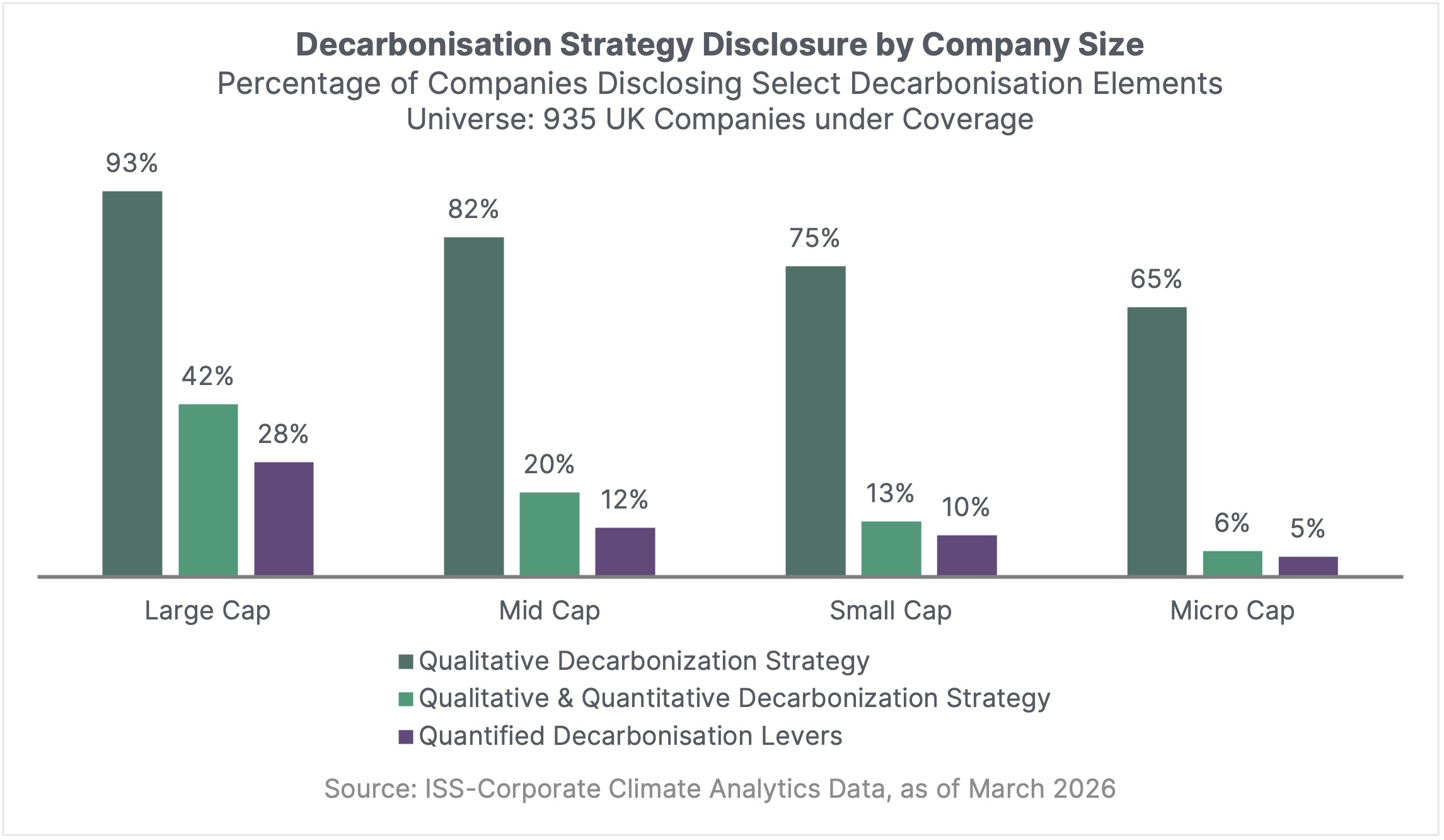

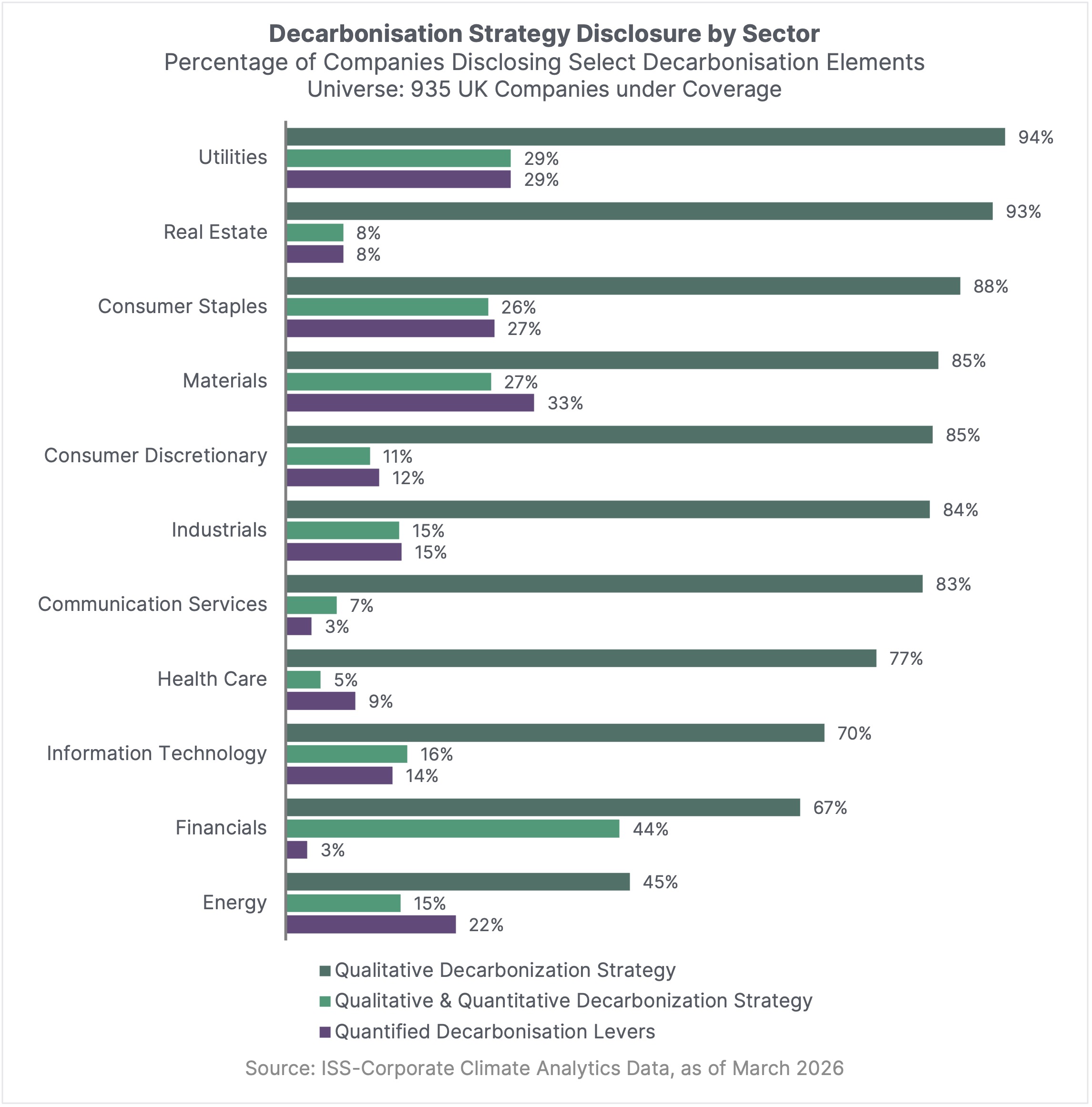

UK Issuers Current Climate-Related Reporting Alignment

To understand how prepared UK companies are for the transition to UK SRS S2, we analysed three indicators of decarbonisation‑strategy maturity:

-

- Qualitative Decarbonisation Strategy

- Quantitative Decarbonisation Strategy

- Quantified Decarbonisation Levers

These indicators illustrate how far companies have progressed from identifying actions, to quantifying them, to demonstrating how each action contributes to their climate targets.

Across both charts, a consistent pattern emerges: qualitative decarbonisation strategies are fairly widely disclosed, but far fewer companies are disclosing their quantified actions, effectively providing details such as the percentage share of renewable energy or financial spend on specific transition activities, within the plan that support the overall strategy, or quantifying the contribution of specific decarbonisation levers.

Large companies lead in disclosure maturity, with 42% providing both qualitative and quantitative strategies, while small and micro caps lag sharply. Sector results show the same dynamic: most industries articulate high‑level actions, but only a minority quantify those actions, and break down the impact of individual levers.

Why Quantifying Decarbonization Actions Remains a Challenge

Identifying decarbonisation actions that can be taken within a strategy is easier than measuring and quantifying the specific implementation required of those actions to support emissions reduction. It is even harder to then measure and quantify the contribution of any one of the implemented decarbonisation measures and to assess the level of success an individual strategic lever is having on the overall decarbonisation plan. The level of disclosure associated with these activities is therefore a reflection of the related complexity of delivering these actions for organisations.

This gap between qualitative and quantitative communication of decarbonisation strategies is significant, and trying to reduce it is important. Measurement is key to quantifying progress and to providing greater levels of certainty to stakeholders, using more widely understood metrics, such as financial spend or percentage adoption. Crucially, the ability to link this information – such as actions in a company’s decarbonisation strategy – to their associated financial costs or benefits to the company over time is a core principle of the UK SRS (and, by extension, the IFRS SDS) through the concept of connected information.

As a result, the UK SRS places greater emphasis on assessing the current and anticipated effects of decarbonisation actions, mitigation and adaptation efforts, alongside clearer connectivity to the financial statements. This emphasis is reflected in the removal of the relief allowing sustainability information to be reported after the financial statements. In this context, measuring, quantifying, and articulating the role and effectiveness of strategic decarbonisation levers is increasingly important, providing decision-useful information for both companies and investors.

As UK-listed companies prepare for mandatory UK SRS S2 reporting from 2027, they will need to consider where additional work may be required to meet the new expectations around targets, measurable transition actions, and decision-useful disclosure.

How ISS‑Corporate Supports UK SRS‑Aligned Reporting

As expectations on climate disclosures rise – both globally and domestically in the UK – many companies are now assessing what meaningful, decision-useful reporting will require.

Whether preparing for upcoming regulatory changes, strengthening the credibility of climate data or developing a transition plan aligned with investor expectations, we support companies in translating evolving standards into clear, actionable steps. Our support is designed to meet organizations where they are, from identifying gaps and assessing climate risks to setting robust targets and preparing high quality disclosures.