Renewable Energy Disclosure and Underlying Energy Use

Corporate energy disclosures increasingly distinguish renewable sources, reflecting evolving global standards, regulatory requirements, and growing stakeholder expectations around energy management.

Corporate disclosure of energy consumption from renewable sources is becoming more prevalent and more granular. An increasing number of companies now distinguish between renewable and non‑renewable energy in their reported consumption, and many go further by specifying the underlying renewable sources – such as wind, solar, hydropower, or biomass – either for on‑site generation or purchased energy. This evolution reflects both growing stakeholder interest in how organizations manage energy use and the gradual convergence of reporting expectations across standards and jurisdictions.

Global sustainability reporting frameworks set differentiated but complementary expectations. Under GRI 302 (Energy), organizations are required to disclose fuel consumption separately for renewable and non‑renewable sources. For other forms of energy, including purchased electricity, total consumption must be reported, while additional breakdowns by energy source are encouraged where they enhance transparency or comparability. Where energy management is deemed material, SASB standards require companies to disclose the percentage of total energy consumption derived from renewable sources, applying narrowly defined and verifiable criteria for what qualifies as renewable energy.

Regulatory requirements are also shaping disclosure practices. The European Sustainability Reporting Standards introduce more prescriptive requirements under ESRS E1, including disclosure of total final energy consumption disaggregated by fossil, nuclear, and renewable sources, along with more detailed breakdowns for high‑impact sectors and conservative, contract‑based attribution of renewable energy. In parallel, several jurisdictions that have adopted mandatory sustainability reporting regimes have introduced standardized approaches to reporting renewable energy consumption, further reinforcing consistency and comparability across markets.

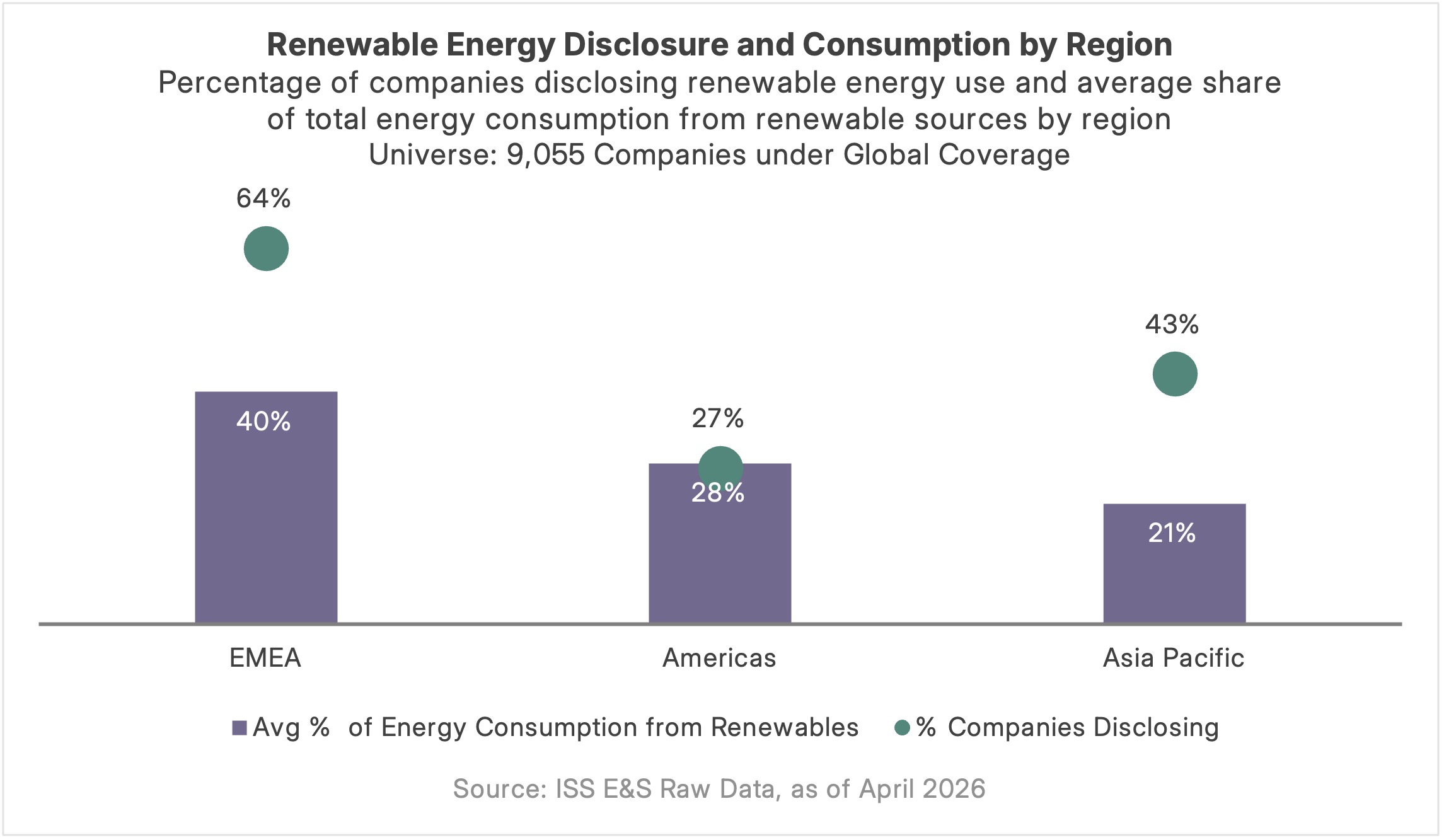

Renewable Energy Disclosure by Region

ISS‑Corporate reviewed corporate disclosure data on renewable energy consumption covering 9,055 companies in the ISS E&S Raw Data database to identify regional patterns in both disclosure practices and reported energy use. The analysis reveals significant variation by region, reflecting differences in regulatory reporting standards, renewable energy capacity, energy policies, and sectoral composition. Companies in EMEA lead on transparency, with 64% disclosing a breakdown of energy consumption by renewable source and an average of 40% of total energy consumption coming from renewables. Disclosure rates are notably lower in Asia Pacific, where 43% of companies report a renewable energy breakdown and average renewable energy use stands at 21%. Companies in the Americas lag behind EMEA on disclosure, with just 27% providing a breakdown, but report a higher average share of renewable energy consumption (28%) than Asia Pacific. Overall, these regional differences point to distinct patterns in renewable energy disclosure and reported consumption that warrant closer examination at the jurisdictional level.

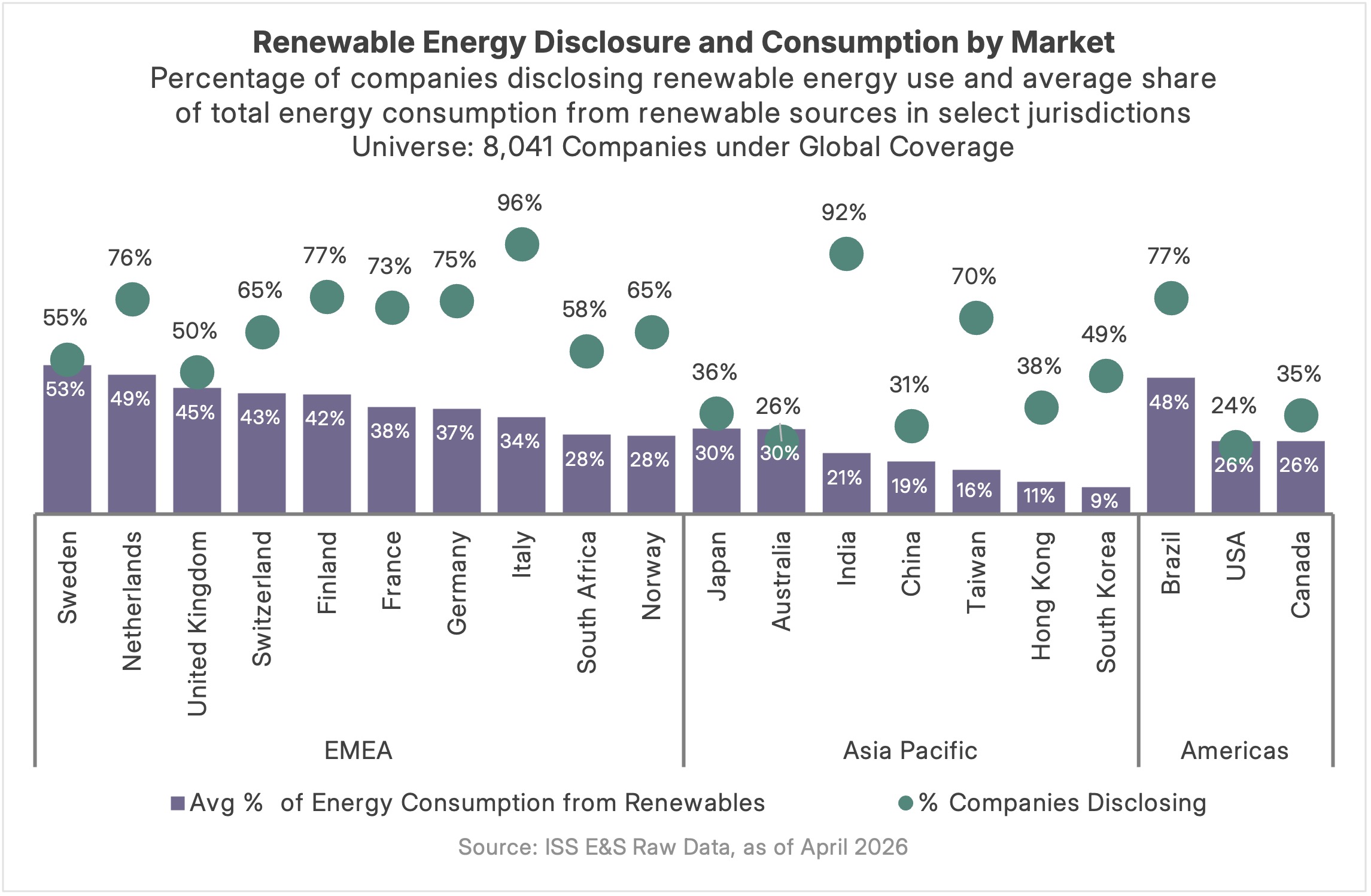

Jurisdictional Differences in Disclosure and Energy Mix

Jurisdiction‑level data highlight that disclosure practices and renewable energy consumption are influenced by different structural factors and do not always move in tandem. Across Europe, disclosure rates are generally higher and average renewable energy use tends to exceed other regions, reflecting more mature reporting requirements and, in several markets, greater renewable capacity. However, variation remains pronounced even within Europe. Italy, for example, reports near‑universal disclosure but a more moderate average share of renewable energy consumption, while Norway – despite a renewable‑rich national energy system – shows lower average consumption at the company level, likely reflecting sector composition skewed toward energy‑intensive industries such as oil and gas, materials, and industrials.

Outside Europe, Brazil and India stand out for relatively high disclosure rates, suggesting the influence of regulatory initiatives and reporting expectations, even as average renewable energy consumption differs materially between the two. In parts of Asia, advanced economies such as Japan, South Korea, and Taiwan display comparatively lower shares of renewable energy use, reflecting energy system constraints, reliance on nuclear or fossil sources, and limited domestic renewable capacity – despite steadily improving transparency. Taken together, the data underscore that disclosure levels are shaped primarily by reporting frameworks and policy expectations, while reported renewable energy consumption reflects a combination of sector mix, national energy systems, and access to renewable infrastructure.

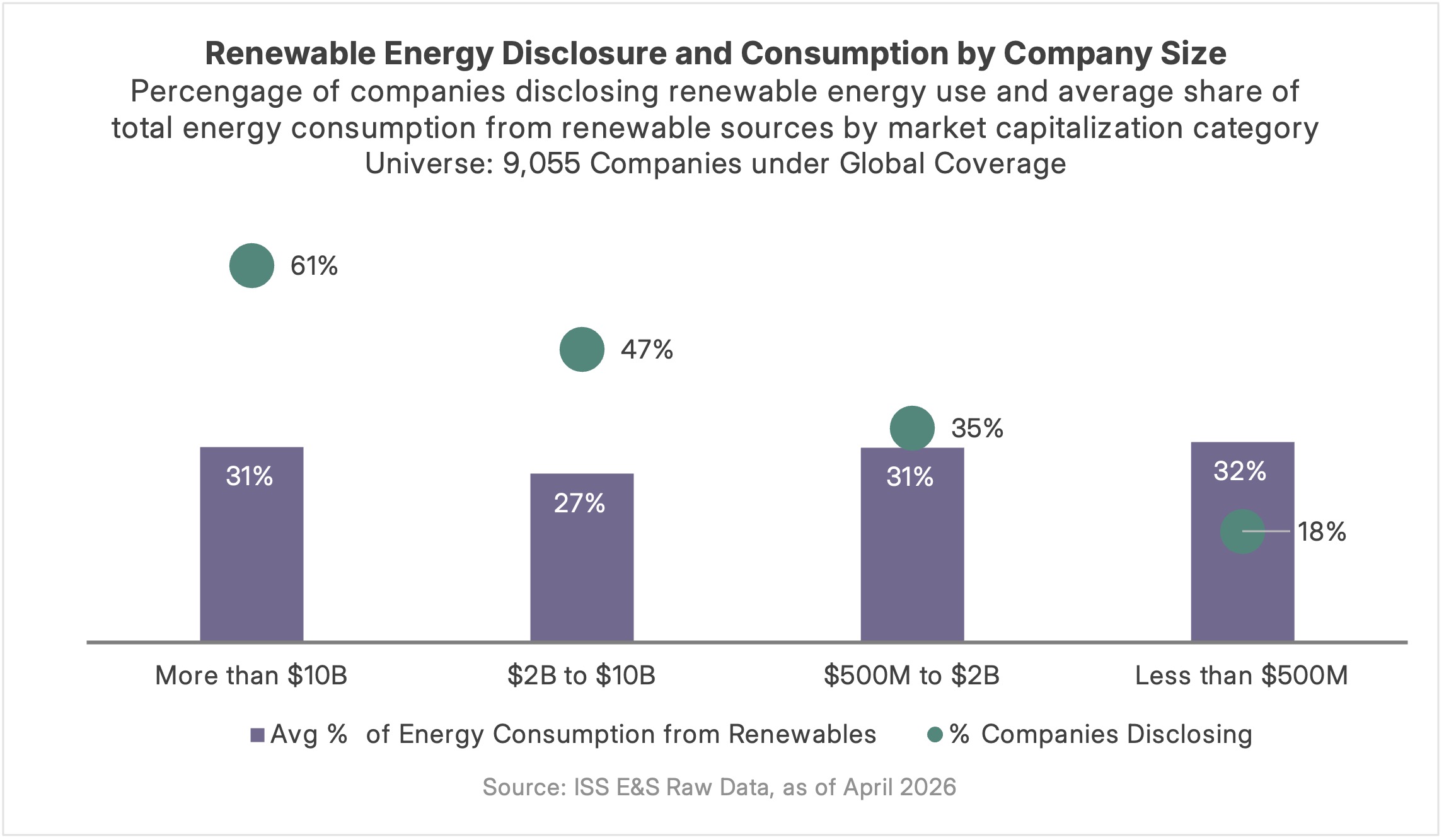

Company Size Drives Disclosure, Not Energy Mix

When viewed by company size, disclosure rates increase consistently with market capitalization. Among companies with market capitalization above $10 billion, 61% disclose a breakdown of energy consumption from renewable sources, compared with just 18% among companies with market capitalization below $500 million. In contrast, average renewable energy consumption shows relatively limited variation across size categories, ranging from 27% to 32%. The data suggests that disclosure is closely linked to company scale, resources, and reporting capacity, while the underlying energy mix appears less sensitive to size and more reflective of factors such as sector exposure, business model, and access to renewable energy resources.

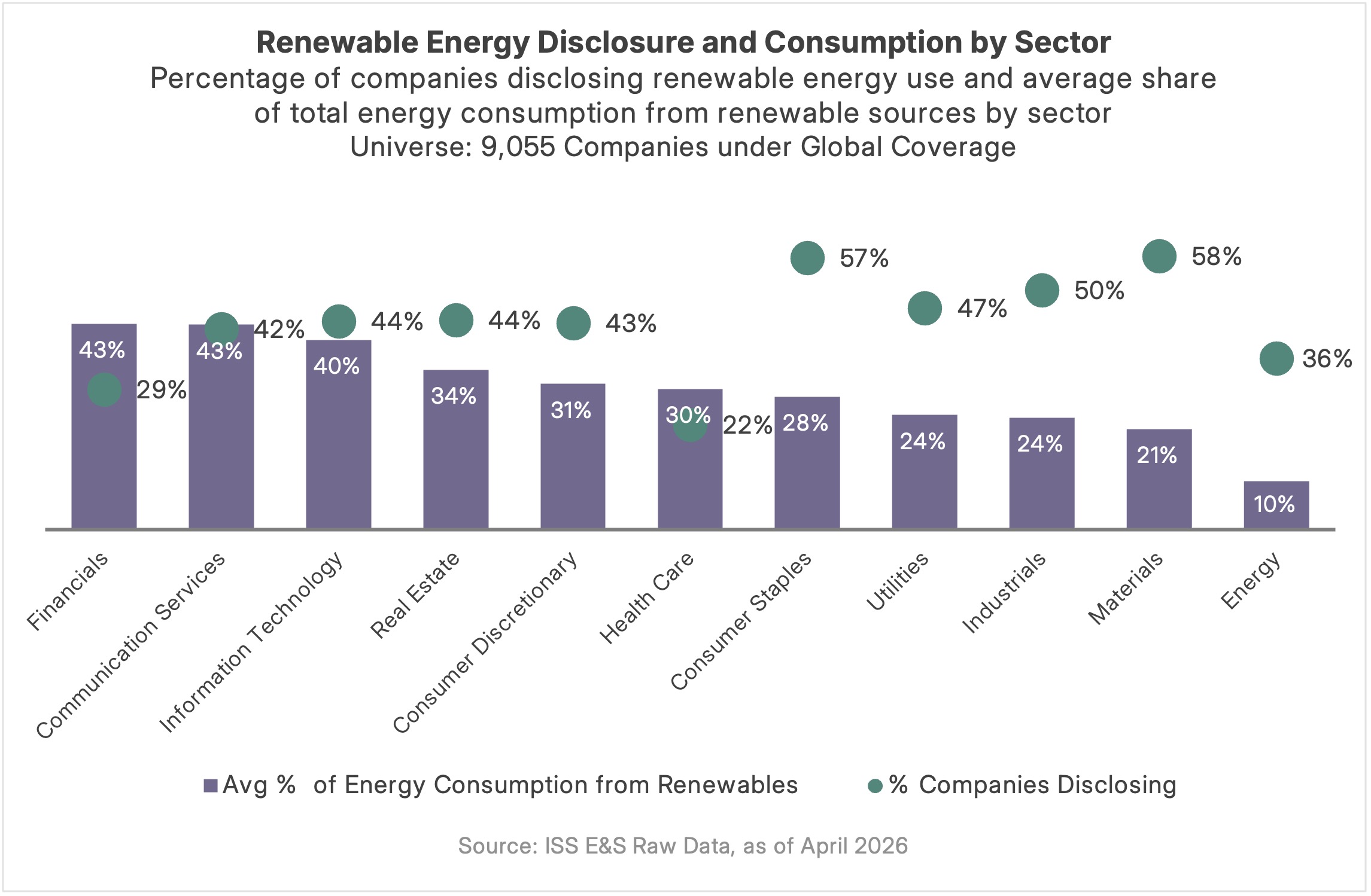

Disclosure and Renewable Use Vary by Sector

When reviewed at the sector level, disclosure rates tend to be higher in more energy‑intensive industries, reflecting greater reporting expectations and the materiality of energy management to core business operations. Sectors such as Materials, Industrials, and Utilities show relatively high proportions of companies disclosing renewable energy consumption, even as their underlying energy needs remain substantial. At the same time, average renewable energy use generally declines as total energy consumption increases. Less energy‑intensive sectors – including Financials and Information Technology – report the highest average shares of renewable energy, reflecting greater reliance on purchased electricity and a higher degree of flexibility in procuring renewable power. By contrast, sectors with large absolute energy requirements, such as Energy, Materials, and Utilities, report more limited renewable penetration, reflecting constraints related to energy‑intensive processes, limited electrification options, and the need for reliable, continuous energy supply. These sectoral patterns reinforce that disclosure behavior and renewable energy consumption are governed by different constraints, with the latter shaped less by reporting practices and more by the physical and operational realities of energy intensive business models.

Turning Renewable Disclosure into Performance

Greater transparency on renewable energy consumption is only one part of effective energy management. While disclosure frameworks help standardize reporting, sustained progress in renewable energy use is more closely tied to how companies manage, monitor, and optimize energy across their operations. Practices such as formal energy management systems, data driven monitoring, and integration of energy considerations into operational decision making can play a critical role – particularly for energy intensive sectors facing structural constraints. As renewable energy disclosures continue to mature, the ability to translate transparency into measurable performance improvements will increasingly depend on the rigor of underlying energy management practices.