Greening Data Centres Through Sustainable Finance

Data centres are becoming essential infrastructure, but the implications of their environmental impact is complex and increasingly scrutinized. As data centre projects scale, the real question shifts from capacity to standards: what truly qualifies as a “green” data centre and who sets the bar?

Sustainable Finance for Data Centres: Aligning Capital Growth with Credible Standards

Sustainable finance for data centres is moving from niche towards greater market relevance, attracting increasing attention across the broader sustainable finance landscape. As digital infrastructure becomes more central to economic growth, cloud services, connectivity, and the rapid expansion of AI are driving rising demand for data centre capacity. But this is not just a story of digital growth. Data centres also carry a broader sustainability footprint, spanning energy demand, water use, upstream resource pressures, and local social impacts.

This creates a clear role for labelled sustainable finance. Green bonds, green loans, and related instruments can help channel capital towards measures that improve the sustainability performance of data centres, including energy efficiency, lower-carbon electricity sourcing, and stronger water management. The opportunity is not simply to finance more digital infrastructure, but to link capital allocation to measurable improvements in environmental performance.

The central challenge, however, is that market growth has outpaced convergence on what should qualify as a “green” data centre. While sustainable finance activity in the sector is increasing, current frameworks still vary materially across issuers and often capture only part of the sector’s sustainability profile. In practice, energy performance remains the dominant lens, while other material considerations, especially water and local context, are incorporated less consistently. That creates risks for comparability, credibility, and market integrity.

Against this background, this article examines the sustainability footprint of data centres, the role of sustainable finance in supporting better practices, the current shape of the market, and the limits of existing definitions and frameworks. It argues that the next phase of market development will depend less on growth alone than on stronger criteria, better reporting, and more robust external assessment. As sustainable finance for data centres expands, the key test will be whether the market can move from growth to integrity.

Key takeaways:

- As data centres are becoming essential infrastructure, their sustainability footprint extends beyond energy use to include water consumption, wider system pressures and local social impacts.

- Labelled sustainable finance can help support more sustainable data centre development, but the credibility of this market depends on whether financing frameworks are tied to meaningful and measurable improvements.

- Current market practice is growing, but it remains uneven and still lacks a sufficiently consistent and comprehensive definition of what should count as a “green” data centre.

- Stronger criteria, better reporting and robust external assessment will be increasingly important if the market is to improve transparency, comparability and integrity.

The Environmental Footprint of Data Centre Growth

Data centres sit at the heart of the digital economy, underpinning cloud services, connectivity, and the rapid expansion of AI. But as deployment accelerates, so does their sustainability footprint. For sustainable finance, the key point is not simply that data centres consume copious amounts of energy and water, but that their impacts span multiple environmental and social dimensions and are often highly location-specific.

Energy is the most immediate challenge. The International Energy Agency (IEA) projects that global electricity generation to supply data centres will rise from around 460 TWh in 2024 to more than 1,000 TWh by 2030. In advanced economies, data centres are expected to account for more than 20% of growth in electricity demand over that period, reversing years of flat or falling power consumption in many markets. While renewables are expected to meet nearly half of demand growth, the IEA also finds that natural gas and coal together are still likely to supply more than 40% of additional demand through 2030. For sustainable finance, that makes it essential to look beyond efficiency alone and assess whether growth is being supported by credible low-carbon power sourcing as well.

Water is a second material issue, both directly through cooling and indirectly through electricity generation. Research published in Nature estimated that a small 1 MW data centre can consume up to 25.5 million litres of water a year for cooling alone. The risk is particularly acute where facilities cluster in already stressed basins. Analysis by Ceres finds that data centre growth could increase water stress in already strained areas by up to 17% annually, with higher seasonal spikes; its related release notes that in some locations the increase could reach 32% if all currently planned facilities come online. These dynamics make water risk highly material for sustainable finance, particularly where location, cooling design and local resource constraints are not adequately reflected in financing criteria.

The footprint also extends beyond the facility itself. Data centre expansion increases demand for resources, creating wider pressures across the value chain. For example, the National Engineering Policy Centre notes that semiconductor manufacturing, which is central to data centre hardware, relies on critical minerals. This may create additional challenges for other industries in achieving both decarbonisation and growth objectives. Upstream water use is also substantial: Ceres notes that a single semiconductor fabrication facility can consume up to 10 million gallons of ultrapure water per day. For sustainable finance, this means the case for data centre financing cannot be assessed at asset level alone; it also depends on how growth interacts with wider system constraints and the transition needs of other sectors.

There are social considerations as well. Local opposition often reflects concerns about pressure on shared infrastructure, especially electricity and water, alongside questions about how costs and benefits are distributed. Brookings notes that critics see data centres as among the least labour-intensive structures in the economy, even where they generate construction activity and tax revenues. That does not diminish their economic importance, but it does reinforce the need for a broader assessment of sustainability performance and community impact. Taken together, these issues point to a clear conclusion for sustainable finance: data centres require a more comprehensive framework than energy performance alone.

How Sustainable Finance Supports Greener Data Centres

Labelled sustainable finance instruments, such as green bonds and green loans, can help channel capital towards measures that improve the sustainability performance of data centres. Under ICMA’s Green Bond Principles, that means financing eligible projects with clear environmental benefits, supported by transparent processes for project selection, allocation, and reporting. In this context, the key question is not whether the sector is inherently green, but whether financing frameworks are tied to credible improvements in areas such as energy efficiency, low-carbon electricity sourcing, and water management.

Energy efficiency remains one of the clearest areas where sustainable finance can support better outcomes. The World Bank and International Telecommunication Union practitioner guide on green data centres highlights measures such as more efficient hardware, improved airflow and cooling design, waste heat recovery, and operational optimisation as central levers for reducing environmental impact. In a sector facing rapid demand growth and mounting pressure on electricity systems, financing frameworks that reward meaningful efficiency gains are likely to remain a core part of the sustainable finance case for data centres.

A second important area is electricity sourcing. The same World Bank and International Telecommunication Union guidance identifies renewable energy integration, energy storage, and other measures to reduce reliance on emissions-intensive power as essential elements of greener data centre design and operation. This matters because efficiency improvements alone do not resolve the sector’s sustainability challenge if the underlying power mix remains carbon intensive. The system implications of rising energy demand are already visible in some markets. In Ireland, data centres accounted for 22% of metered electricity consumption in 2024, according to the Central Statistics Office. In practice, the credibility of this category depends on the robustness of the underlying criteria, including how financing frameworks treat procurement structures, the quality of renewable energy claims and the extent to which lower-carbon electricity is matched to actual consumption.

Water management should also be treated as a core consideration rather than a peripheral one. The World Bank and International Telecommunication Union guide points to lower-water cooling systems, water reuse, and more resource-efficient operational design as important features of greener data centre infrastructure. This is particularly relevant in a sector where water risks are highly location-specific and where weak management can create operational, environmental, and reputational vulnerabilities. As a result, financing frameworks that focus narrowly on energy performance alone risk overlooking a material part of the sustainability profile.

Market signals point in the same direction. An investor survey published by Natixis CIB indicates that investors are paying increasing attention to criteria such as power usage effectiveness, renewable energy use and water-related considerations when assessing the sustainability profile of data centres, and that the sector is not viewed as green by default. While this type of survey evidence is only indicative, it is directionally consistent with a market that is placing greater weight on stronger criteria, better reporting, and a more comprehensive view of material impacts.

Taken together, these considerations show how sustainable finance can help steer the market towards more sustainable data centre development. The opportunity lies not simply in financing more digital infrastructure, but in linking capital allocation to measurable improvements in environmental performance, supported by clear criteria and transparent reporting. The case is reinforced by growing local scrutiny: in the United States, Data Center Watch reports that around USD 18 billion of projects were cancelled and a further USD 46 billion delayed over two years amid local opposition. The remaining question is how far current market practice reflects this broader sustainability logic in reality.

A Growing but Uneven Market

Recent issuance suggests that sustainable finance for data centres is beginning to scale, but the market remains concentrated, uneven, and still at an early stage of maturity. Because data centre-related transactions are rarely labelled as a distinct category, the observations in this section are based on ISS-Corporate’s analysis of sustainable bond and loan issuance by data centre operators, using Environmental Finance data as a proxy for sector activity. On that basis, the market appears to be moving from niche to material while still accounting for only a small share of the broader sustainable debt universe. The question is therefore not only whether the market is growing, but what its current shape reveals about maturity, concentration, and future direction.

Issuance Growth and Scale

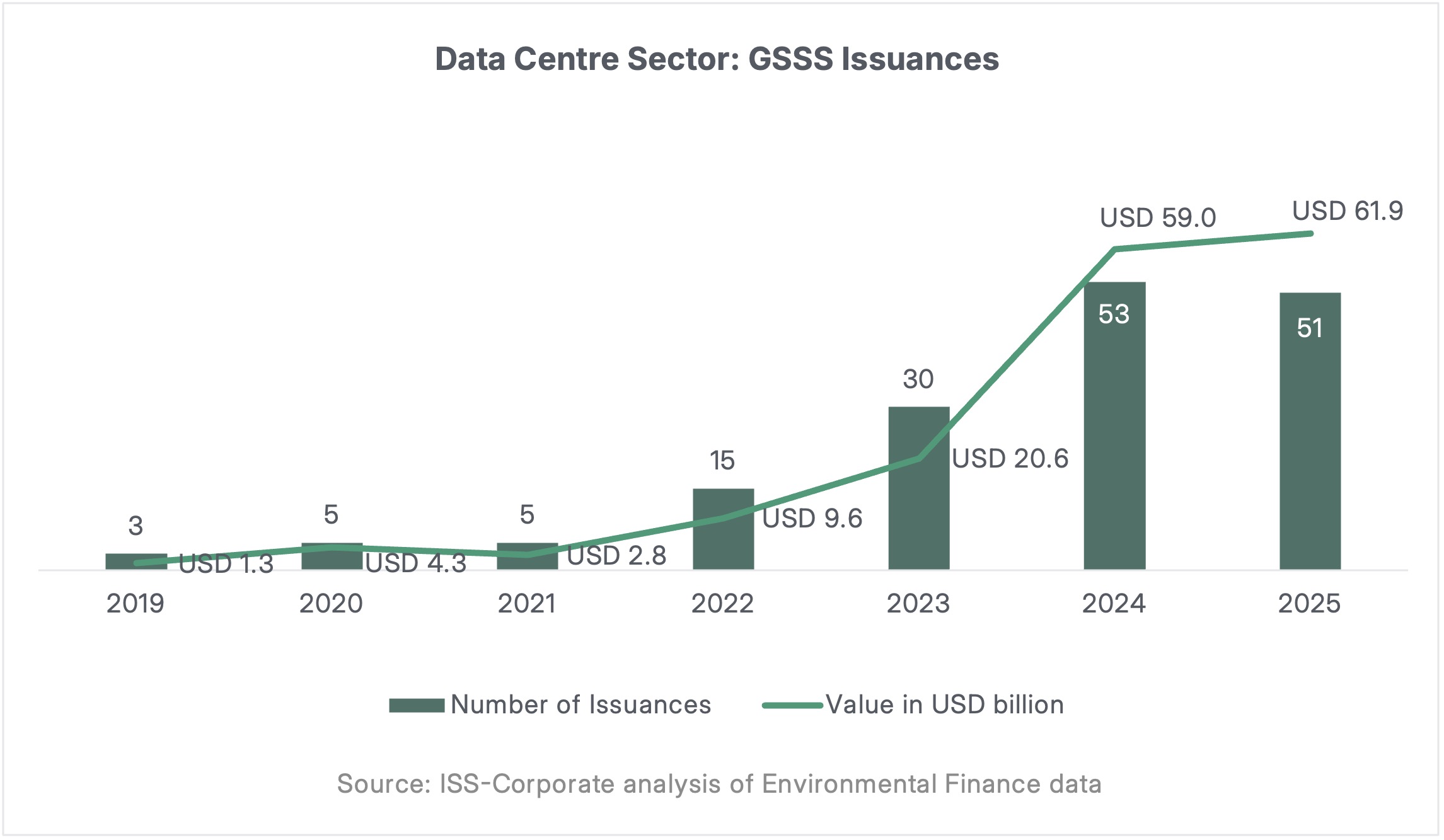

The sustainable debt market for data centres is still relatively young, which is reflected both in the evolving nature of financing frameworks and the lack of convergence on what should qualify as a “green” data centre. Even so, market activity has accelerated sharply. Issuance remained subdued between 2019 and 2021, then rose materially from 2022 onwards, peaking in 2024 and 2025. Measured by transaction count, the sector still accounted for less than 1% of the broader sustainable finance market over the period reviewed. By value, however, its significance increased more visibly, rising from well below 0.25% of the overall market to almost 3.5% in 2025. The segment therefore remains small in breadth, but increasingly meaningful in capital terms.

The chart below illustrates this acceleration in GSSS issuance in the data centre sector, both in transaction count and overall value.

The pattern of issuance is also volatile. Growth in the data centre segment substantially outpaced the wider sustainable debt market in 2023–2024, and the sector continued to expand in 2025 even as the broader market contracted. At the same time, year-on-year swings remain pronounced, reflecting a market concentrated in a limited number of large transactions by a relatively small group of issuers. That concentration is consistent with the structure of the sector itself: data centres are highly capital-intensive, barriers to entry are high, and a relatively small number of global operators dominate investment activity.

What Is Driving Market Expansion?

The observed growth in issuance appears to reflect several reinforcing dynamics. The most immediate is rapid growth in demand for digital infrastructure, particularly in connection with AI-related computing needs. At the same time, policy and taxonomy developments are helping to shape the market by clarifying how greener data centre investments can support wider objectives in areas such as climate action and digital transformation. This is increasingly visible in sustainable finance taxonomies and related frameworks. The EU Taxonomy already includes data processing, hosting, and related activities under specific technical screening criteria, while data centres and related digital infrastructure are also being addressed through regional taxonomy development in Asia and Australia. Even so, the relevant criteria and their application still vary.

A broader shift within sustainable finance may also be contributing. As more conventional green asset classes mature, investors and issuers appear increasingly willing to consider sectors that are economically essential but environmentally complex, provided a credible transition case can be made. That said, this remains an inference rather than a directly observable factor. What is clearer is that the market remains a small subset of the wider capital market for data centre financing, with most sector funding still likely to come through conventional debt, loans, equity, and private financing channels. For some issuers, the additional requirements associated with labelled instruments may still not offer a sufficiently compelling cost–benefit case, particularly in markets

Geographic Concentration and Expansion Prospects

The market is also highly concentrated geographically. The United States accounts for the vast majority of sustainable finance issuance in the data centre sector by value, at around 85%, with Europe and Asia representing much smaller shares and other regions remaining marginal. This broadly reflects where capital-intensive data centre development has so far been most concentrated, supported by deep capital markets, large technology-sector demand, and the presence of major global operators. At the same time, the pattern is not fully aligned with the global distribution of data centre markets: some sizeable locations, including Germany and China, appear less represented in labelled issuance than their infrastructure footprint might suggest.

Looking ahead, further geographic expansion appears likely, but its pace and character remain uncertain. Markets such as Brazil are emerging more clearly within Latin America, where the regional data centre market is expected to double to around USD 10 billion by 2029 from roughly USD 5–6 billion in 2023, according to UNDP. Demand projections for Southeast Asia also point to rapid growth in physical data centre capacity. But growth in infrastructure should not be assumed to translate automatically into growth in labelled sustainable finance. Whether new markets develop meaningful issuance will depend on capital-market depth, policy frameworks, investor appetite, and the credibility of sustainability criteria applied to the sector. In that sense, the geography of issuance reflects not only where data centres are being built, but also where financing conditions and market standards are sufficiently developed to support labelled transactions.

Defining a “Green” Data Centre: Where Market Practice Still Falls Short

If the previous section shows that sustainable finance for data centres is starting to scale, the next question is whether current market practice is converging on a sufficiently robust definition of what should qualify as “green.” Here, the answer remains mixed. Based on ISS-Corporate’s review of 67 data centre-related sustainable issuances, drawing on Environmental Finance data and publicly available issuer documentation, issuance is increasing, but frameworks still vary materially across issuers, instruments and time, and current practice often captures only part of the sector’s sustainability profile. In other words, market growth has so far outpaced convergence on market quality.

Growth Has Outpaced Convergence

There is still no settled market definition of a “green” data centre. Rather than following a single, well-defined standard, sustainable finance frameworks in this segment rely on differing combinations of use-of-proceeds categories, certification schemes, and performance thresholds. That variation is not surprising in a rapidly evolving market, but it does make comparability more difficult and creates room for inconsistent ambition. In practice, the market appears to be maturing gradually, but growth in issuance has so far moved faster than convergence on a comprehensive set of sustainability criteria.

What Use-of-Proceeds Categories Reveal

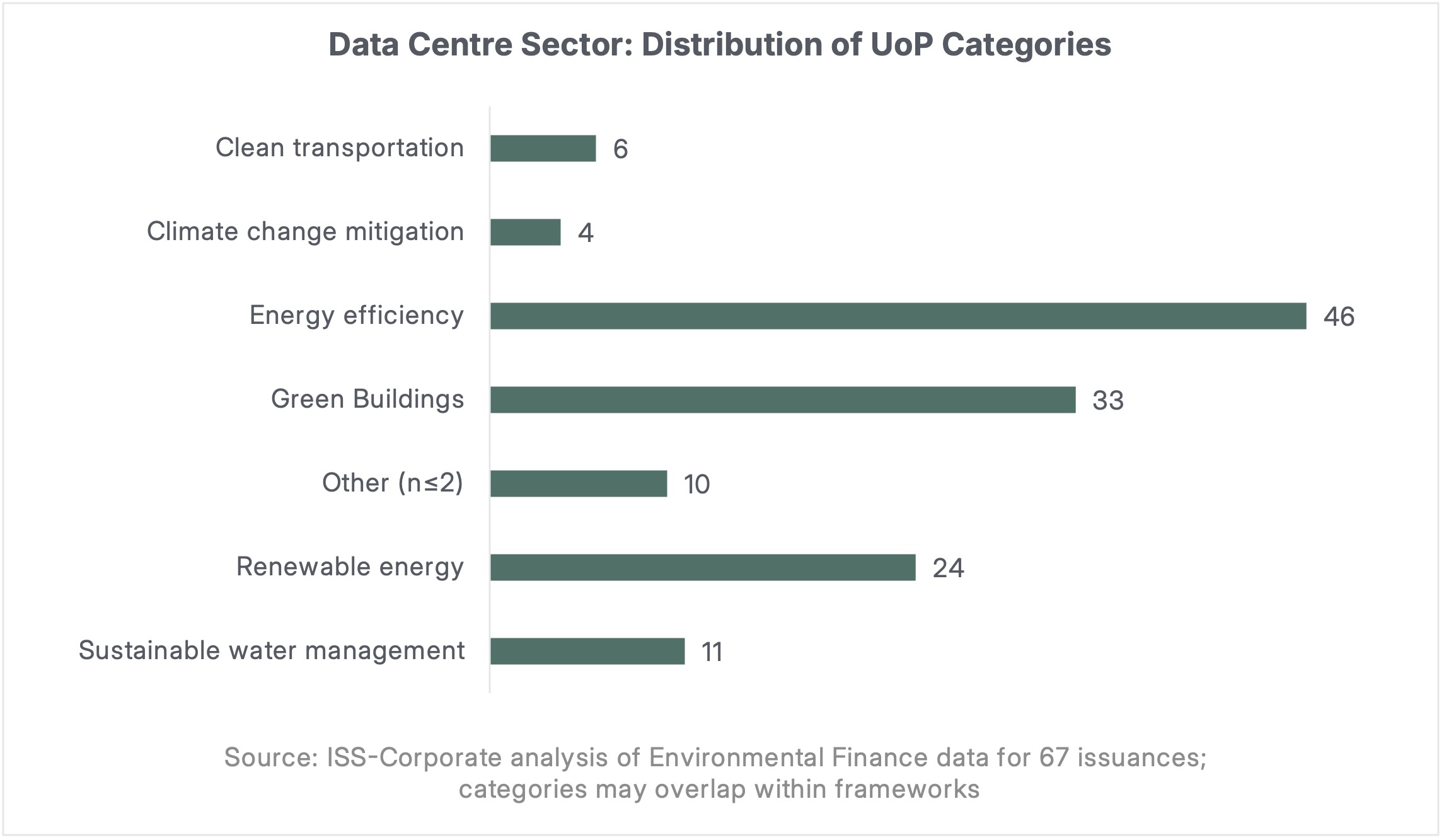

The distribution of use-of-proceeds categories helps show what sustainability objectives current market practice prioritises. The chart below indicates that issuance remains concentrated in a relatively narrow set of categories, with energy efficiency, green buildings, and renewable energy dominating the current landscape.

This concentration matters because it shows that current market practice still defines greener data centre financing primarily through operational energy performance. Other sustainability objectives remain less visible. Sustainable water management appears in only a minority of issuances, despite the sector’s well-documented exposure to location-specific water risks, while social considerations, such as access to essential services and employment generation, are rarer still.

Eligibility Criteria: Evolving, but Still Uneven

A similar pattern appears when looking at how eligibility is defined. Analysis of twelve green finance frameworks linked to data centre-related bond issuance shows that most anchor eligibility in energy efficiency, typically through Power Usage Effectiveness (PUE). This metric remains influential because it provides a simple and widely recognised indicator of how efficiently a data centre uses electricity. However, its dominance also illustrates the narrowness of many current frameworks: a strong PUE alone does not address the carbon intensity of electricity supply, local water stress, or other material sustainability impacts.

There are signs of progress. Early frameworks often used PUE thresholds around 1.5, a level that has since become much less demanding as market practice and technology have advanced. More recent frameworks show some evidence of tightening, including lower thresholds, more detailed operational assumptions, and a broader mix of criteria. In line with the use-of-proceeds patterns above, renewable energy and water-related considerations are appearing more frequently, and some frameworks also rely on improvement-based thresholds or certification schemes. Even so, comparability remains constrained. Different issuers still use different combinations of metrics, assumptions, and boundary conditions, which makes it difficult to assess whether two supposedly “green” data centre projects are genuinely comparable in ambition or impact.

Why Reporting Matters

Where definitions remain uneven, reporting becomes even more important. Labelled instruments can enhance transparency compared with conventional financing by requiring clearer disclosure on allocation and impact but reporting practices across the data centre sector remain inconsistent. This is particularly evident for water, where visibility is still limited despite growing materiality: Environmental Finance reports that only around 40% of data centre operators track water-usage metrics. Stronger reporting on energy use, renewable energy sourcing, and water management would improve investors’ ability to assess risks, compare frameworks, and identify more credible approaches.

This matters not only for transparency, but also for market discipline. Where eligibility criteria differ, disclosure can help reveal how ambitious a framework really is, whether key trade-offs are being addressed and how performance is evolving over time. Better reporting is therefore not a substitute for stronger criteria, but it is an essential complement to them in a market where definitions are still taking shape.

What Stronger Practice Looks Like

A more credible approach to data centre financing would go beyond narrow energy-efficiency metrics alone. It would assess energy performance alongside the quality of electricity sourcing, water management, local resource constraints, and the transparency of impact reporting. It would also recognise that context matters: what counts as a credible improvement may differ depending on whether a facility is new or existing, where it is located, and which environmental constraints are most material in that setting.

This is reflected in ISS-Corporate’s approach, which does not treat data centres as inherently green but instead assesses whether a financing framework supports meaningful improvements in environmental performance. In practice, that means looking at energy efficiency, renewable or lower-carbon electricity use, attention to water stress and other minimum safeguards, together with stronger expectations on transparency. Framed this way, external assessment does not confer an automatic label but helps issuers and investors judge whether a framework is sufficiently robust for a sector whose sustainability profile is still evolving.

What Comes Next: Strengthening Integrity, Comparability and Transparency

Sustainable finance for data centres is likely to remain a growing and strategically important segment of the market. But if that growth is to support credible environmental outcomes, the next phase of market development will need to focus less on expansion alone and more on quality. The central challenge is no longer simply whether data centres can enter sustainable finance, but whether the criteria used to assess them are sufficiently robust, comprehensive, and transparent to distinguish meaningful improvement from weak labelling.

That requires a broader and more consistent approach to what counts as a credible sustainable financing framework in this sector. Energy efficiency will remain central, but it should not be treated as sufficient on its own. Electricity sourcing, water management, local resource constraints, and stronger impact reporting all need to become more systematic parts of market practice. Greater alignment with taxonomies and other recognised frameworks may help improve comparability, but market integrity will still depend on how rigorously these criteria are applied in practice.

This is where external assessment can make a meaningful contribution. In an evolving market, Second Party Opinions and Report Reviews can help issuers and investors navigate complexity by clarifying assumptions, strengthening disclosure, and improving confidence that labelled instruments are linked to material environmental improvements rather than narrow or outdated proxies. Their value lies not in conferring a label automatically, but in supporting greater discipline, consistency and credibility as market practice matures.

As digital infrastructure becomes more central to economic development, the financing of data centres will increasingly sit at the intersection of sustainability, competitiveness, and industrial strategy. That makes the question of what qualifies as “green” in this sector more than a technical one: it is central to whether sustainable finance can allocate capital in ways that are environmentally credible, operationally relevant, and useful for investment decision-useful. The opportunity is real, but so is the need for stronger standards. The credibility of this market will depend on whether it can move from growth to integrity.