California Climate Accountability Update: Highlights from CARB Workshop on SB 253 & SB 261

The California Air Resources Board (CARB) hosted a public workshop on May 29, 2025 to discuss the development of California’s Corporate Greenhouse Gas Reporting Program established by Senate Bill (SB) 253 and the Climate-Related Financial Risk Disclosure Program authorized by SB 261, collectively called the California Climate Accountability Package (CCAP).

Despite an ambiguous timeline for the release of full regulatory guidance, the original reporting deadlines established by CCAP remain intact, with the first deadline approaching on January 1, 2026. The regulation, which requires companies doing business in California to annually disclose scopes 1, 2, and 3 GHG emissions (SB 253) and to biennially report on climate-related financial risks (SB 261), introduces unprecedented climate-related disclosure requirements for U.S. companies. While CARB noted its intent to publish full regulatory guidance by the end of 2025, companies would benefit from beginning compliance work now to prepare for the January 2026 reporting deadline.

Key Takeaways from the May 2025 CARB Workshop

- Record Turnout: This workshop was the most widely attended ever hosted by CARB, demonstrating the public’s strong interest in the CCAP and desire for more detailed guidance.

- Guidance Delay: CARB previously announced that it would share regulatory guidance for SB 253 and SB 261 by July 1, 2025. Throughout the webinar, it became clear full regulatory guidance may not be ready by July 1, 2025. Instead, CARB emphasized that it plans to release full regulatory guidance “by the end of the year.”

- Reporting Deadlines Stand: Despite the ambiguous timeline for regulatory guidance, CARB reiterated that SB 253 and SB 261 reporting deadlines remain intact for now:

- For SB 253, Scopes 1 and 2 greenhouse gas emissions are expected in 2026 on calendar year 2025 data, and Scope 3 greenhouse gas emissions are expected in 2027 on calendar year 2026 data.

- For SB 261, a climate-related risk report aligned with the Taskforce on Climate-related Financial Disclosures (TCFD) and/or the International Sustainability Standards Board (ISSB) are expected to be published on company websites on or before January 1, 2026.

- Definitions Still Evolving: CARB provided working definitions for such terms as “doing business in California” and “revenue,” but has requested multiple rounds of public feedback throughout 2025 before complete regulatory guidance is finalized.

Regulatory Review of SB 253, SB 261 & SB 219

Enacted in October 2023, SB 253 and SB 261 were created to increase transparency and comparability of California companies’ greenhouse gas emissions and climate-related risks (please see ISS-Corporate’s publication providing an overview of the legislation here).

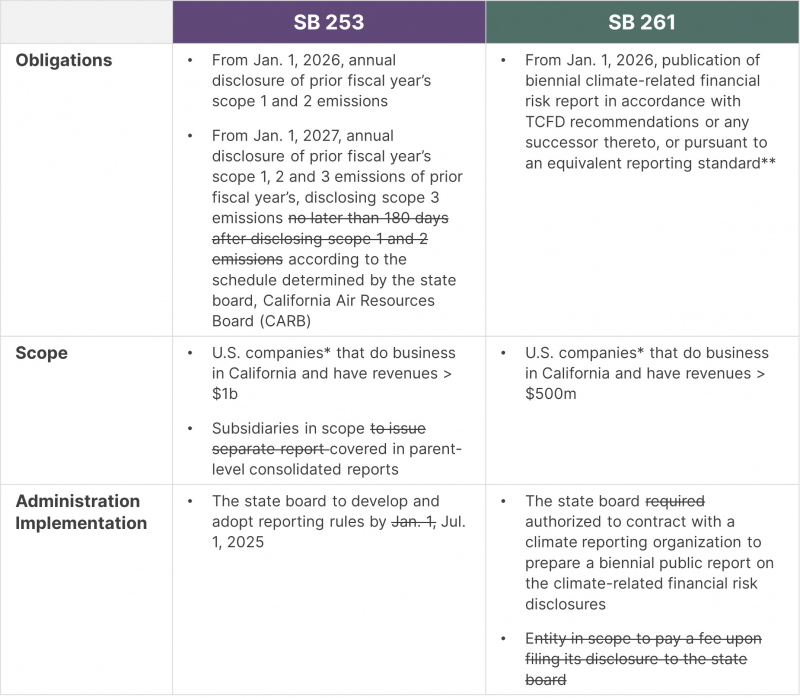

In September 2024, the state of California signed SB 219 into law, implementing the CCAP (SB 253 and SB 261). SB 219 made slight amendments to SB 253 and SB 261, highlighted in the graphic below:

KEY REQUIREMENTS

(amendments under SB 219 marked in strikethrough text)

In December 2024, CARB released an Enforcement Notice specific to SB 253 stating that entities reporting scopes 1 and 2 greenhouse gas emissions in 2026 may use existing data “at the time this Notice was issued” when completing the first year of reporting. CARB reiterated this update during the May 29 workshop, asserting that there will be “no penalties in 2026 if companies show good faith effort” in reporting scopes 1 and 2 emissions.

Recent Regulatory Updates

The May 29, 2025 workshop was hosted by CARB to discuss the entity’s ongoing development of the CCAP. The authors of SB 253 and SB 261, State Senators Scott Weiner and Henry Stern, opened the workshop affirming the importance of the legislation and that the regulatory development process will move forward despite ongoing litigation. The Senators also highlighted that they are paying close attention to developments related to the Corporate Sustainability Reporting Directive (CSRD) in Europe and ISSB adoption globally as they continue to develop California’s own climate-related reporting standards.

CARB then presented clarifications on the scope of the CCAP, specifically providing draft definitions for “doing business in California” and “revenues”. CARB noted its intent to utilize existing definitions already codified in California law. The initial CARB staff concept for “doing business in California” utilizes the definition provided in § 23101 of California’s Revenue and Tax Code (RTC) (a business operating in the state with sales of more than $500,000 or 25% of total revenue, owning property of $50,000 or more or with payroll of $50,000 or more). The initial CARB staff concept for “revenue” is “gross receipts” as set for in California Revenue and Taxation Code § 25120(f)(2). Additionally, CARB addressed parent-subsidiary considerations by stating the initial staff concept for defining corporate relationships relies on the definition established in the California Cap-and-Trade program. CARB the noted it will need public feedback on these concepts before moving forward in clarifying other aspects of the CCAP.

CARB ended the workshop with an open forum for questions and feedback. Many questions revolved around whether CARB would share further guidance by July 1, 2025, as mandated by SB 219. CARB equivocated on providing a direct answer, instead offering that it has the challenge of trying to harmonize existing voluntary standards (GHG Protocol, ISSB, and TCFD) with the specific requirements the state of California must follow to implement any regulation, and it is hoping to complete this task and release regulatory guidance “by the end of the year”.

Staying Ahead of CARB: Why Early Preparation Matters

CARB will host more workshops throughout 2025 to engage stakeholders at each stage of the rulemaking process. There are more definitions and clarifications to come. While we are still waiting for full regulatory guidance, CARB reiterated the initial reporting deadline of January 1, 2026, has not changed.

For entities that have not published greenhouse gas emissions and/or a climate-related risk report before, both disclosures are large undertakings which could require months of work. While it would be ideal to have full regulatory guidance sooner rather than later to know exactly what is required for compliance, it may make sense for companies to start preparing these disclosures as soon as possible to meet the January 1, 2026, deadline.