2025 Sustainability Reporting: Global Trends in Framework Adoption

Companies face shifting sustainability reporting standards in 2025, navigating global mandates, voluntary frameworks, and strategic choices in sustainability reporting.

The sustainability reporting landscape is at a pivotal moment in 2025. Companies across regions are navigating a complex mix of evolving standards, regulatory mandates, and investor expectations. Understanding framework adoption trends is critical because these choices shape how businesses communicate sustainability and climate management, while affecting comparability, credibility, and compliance.

This year marks several major developments:

- Europe’s first year of ESRS implementation: The rollout of the European Sustainability Reporting Standards introduced detailed requirements, while an omnibus proposal to simplify the standards created uncertainty for preparers.

- Jurisdictional adoption of IFRS S1 and S2: IFRS is gaining traction globally, with more than 30 jurisdictions moving toward mandatory reporting. IFRS S2 builds on Task Force on Climate-related Financial Disclosures (TCFD), effectively replacing it, while IFRS S1 incorporated SASB principles and industry-specific metrics.

- Regional regulatory shifts: In the U.S., the SEC withdrew its climate disclosure rule after prolonged litigation, leaving no federal mandate in place. Meanwhile, California moved forward despite legal challenges, with mandatory climate reporting set to begin in January 2026. In Canada, IFRS-aligned standards (CSDS 1 and CSDS 2) are available for voluntary adoption, but mandatory implementation awaits regulatory action, with no major updates since the government change.

Against this backdrop, a question that often arises among corporates is: “What should we use for reporting now?” It is a good question – and one worth considering given the pace of change in sustainability standards.

This analysis looks at trends in the adoption of key frameworks – GRI, TCFD, and SASB – across major regions and explores what these patterns may signal for the future of sustainability reporting.

Regional Trends in Framework Adoption

Americas: Voluntary Frameworks Gain Ground

In the Americas, sustainability reporting frameworks have continued to gain traction over the past four years, reflecting both investor expectations and evolving regulatory dynamics. Adoption of the TCFD framework has risen steadily, moving from 27% in 2022 to 35% in 2025, with a considerable increase expected in 2026 as California’s climate disclosure laws take effect. The SASB standards – originally a framework developed for U.S. companies – have also maintained strong momentum, increasing from 37% to 41% during the same period, driven by their industry-specific focus and widespread acceptance among investors. The GRI framework has remained relatively stable, with a modest increase from 27% to 29% of companies under coverage, suggesting continued relevance for companies seeking comprehensive coverage in sustainability disclosures. These frameworks have coexisted effectively in a voluntary reporting environment, enabling companies to layer climate-specific, industry-focused, and broad sustainability disclosures without conflicting requirements – a flexibility that has driven uptake among large and mid-cap companies in the region.

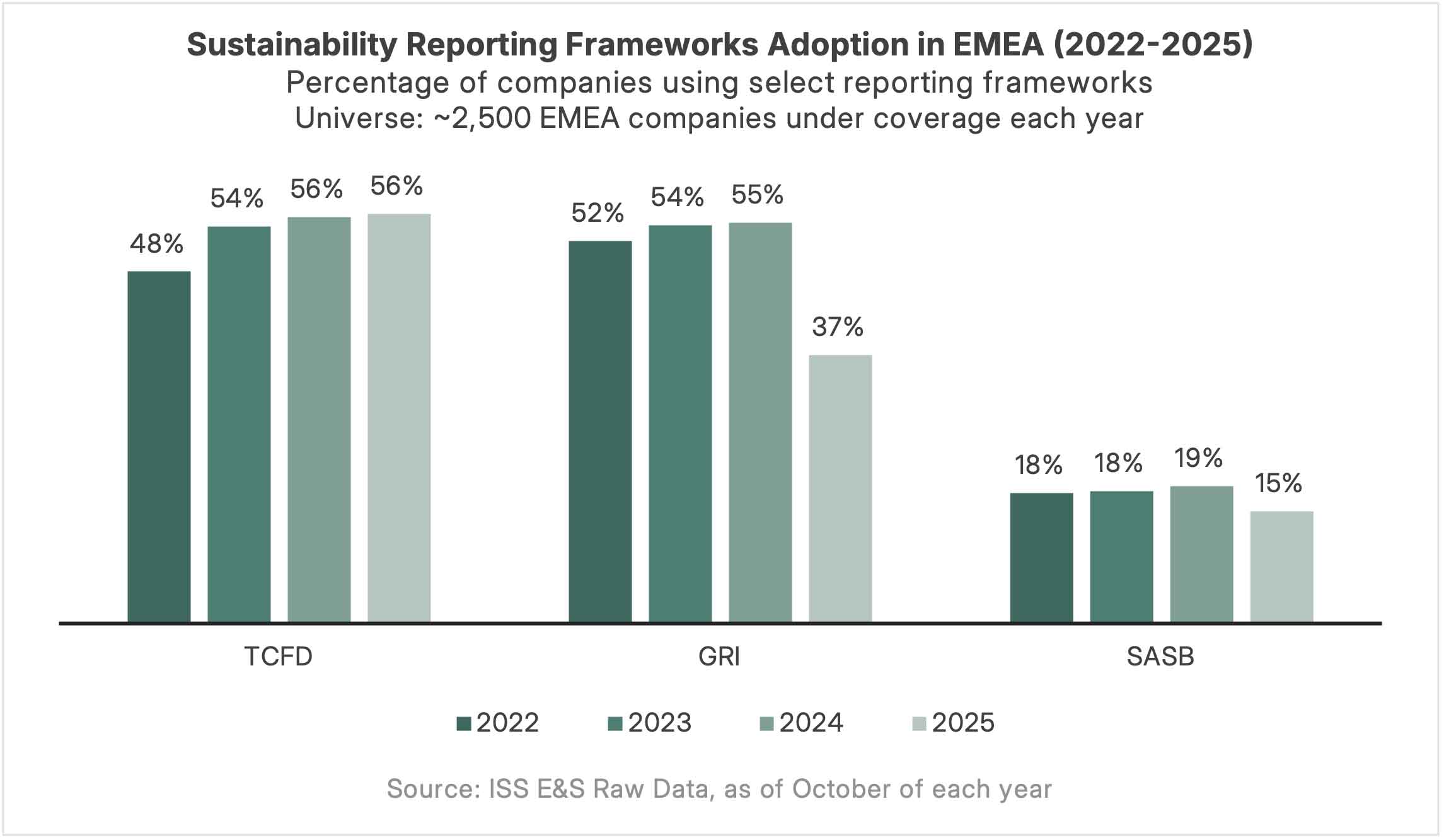

EMEA: ESRS Reshapes Disclosure Practices

The introduction of the European Sustainability Reporting Standards (ESRS) is already reshaping disclosure practices across EMEA. While formal compliance is limited to Wave 1 companies in 2025, many others have begun aligning with ESRS in preparation for future mandates – prompting a noticeable shift away from voluntary frameworks. GRI adoption dropped from 55% in 2024 to 37% in 2025, as ESRS’s comprehensive scope made GRI appear redundant for many companies. Still, some continue to reference GRI alongside ESRS to maintain stakeholder continuity or bridge transitional gaps. This dual use reflects the complexity of the current reporting environment.

SASB adoption declined from 19% to 15%, not due to regional limitations but because ESRS already addresses many of the same topics. While SASB was once viewed as U.S.-centric, its integration into the ISSB framework has elevated it to global standard status. Under ESRS, however, its incremental value is limited.

TCFD reporting remained steady at 56%, underscoring its continued relevance for climate disclosures. ESRS E1 fully incorporates TCFD’s 11 recommended disclosures, offering strong interoperability and allowing companies to build on existing practices in governance, strategy, and risk management. As companies adapt, they are reassessing the role of voluntary frameworks – balancing regulatory compliance with stakeholder expectations and leveraging interoperability where possible.

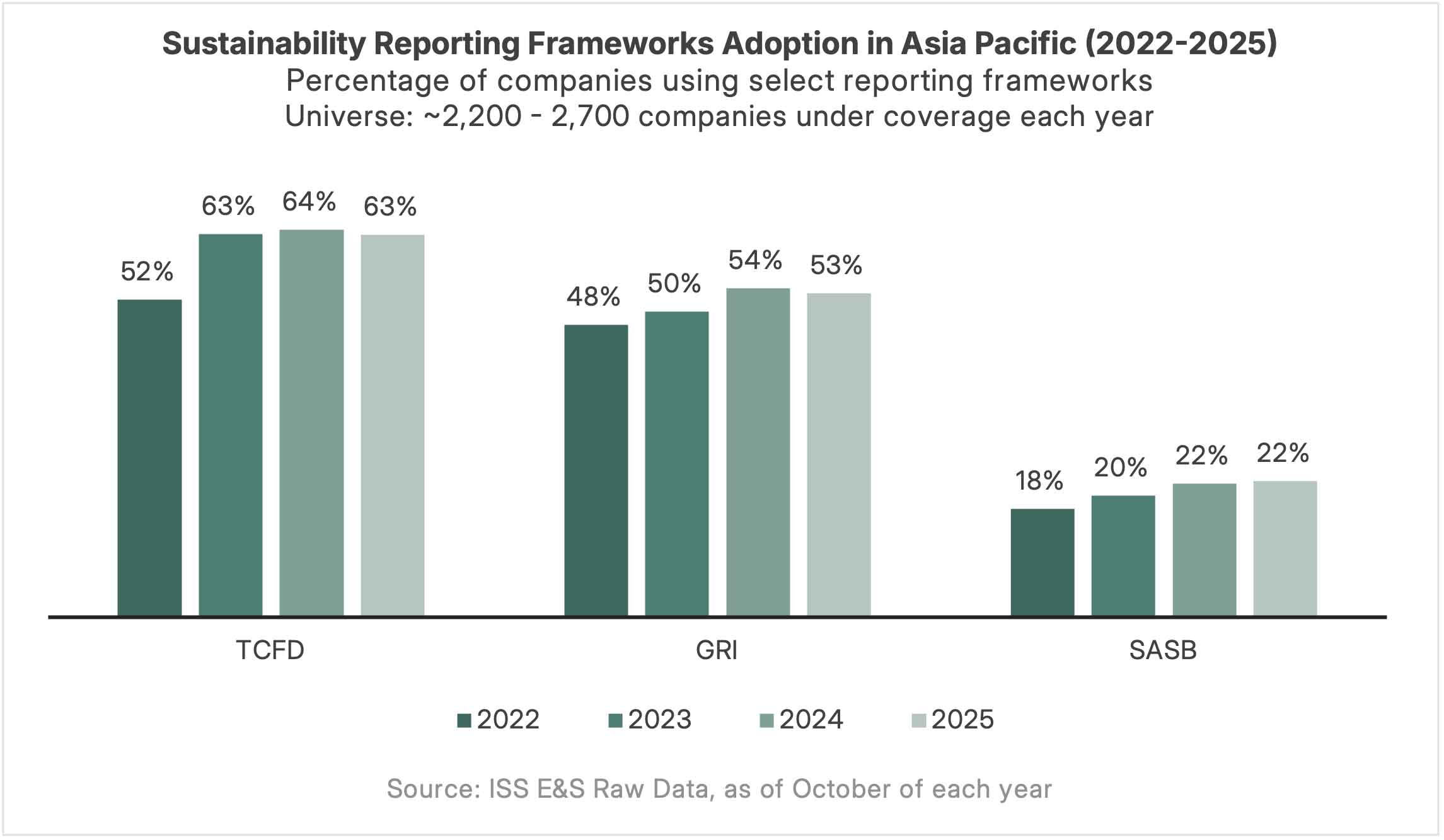

Asia Pacific: TCFD Dominance and IFRS Convergence

Regulatory reporting mandates across Asia Pacific have reinforced the dominance of TCFD and shaped the trajectory of other frameworks. TCFD adoption held at 63% in 2025, reflecting its role as the foundation for emerging regulatory requirements. Jurisdictions such as Japan, Hong Kong, and Australia have embedded TCFD principles into mandatory disclosure rules, while China, South Korea, Taiwan, and India are advancing similar initiatives. Adoption is particularly high in Taiwan (98%), Japan (91%), and South Korea (74%), where companies are increasingly aligning with global climate disclosure standards. Many of these jurisdictions are converging around IFRS S2, which is emerging as a common reference point across the region.

GRI remained steady, reaching 54% in 2024 before dipping slightly to 53% in 2025. Its persistence reflects continued demand for broad sustainability disclosures, even as climate-specific mandates take center stage. Companies in markets like Taiwan and South Korea, where GRI adoption is particularly high, often use it to complement climate-focused frameworks and meet broader stakeholder expectations.

SASB adoption increased gradually from 18% to 22%, likely supported by its integration into the ISSB framework. Jurisdictions such as Hong Kong, Japan, and Malaysia have formally aligned with ISSB rules, while Australia and Singapore focus on climate disclosures under IFRS S2. Taiwan (95%) and South Korea (76%) stand out with the highest SASB adoption rates in the region, reflecting strong uptake of industry-specific standards even as broader regulatory frameworks evolve.

What’s Next: Strategic Choices, Convergence, and Simplification

As jurisdictions finalize mandates, accelerated adoption of IFRS standards is expected in 2026–2027, reinforcing the global shift toward standardized sustainability disclosures. In the U.S., California’s climate disclosure rules are likely to drive broader uptake of TCFD and IFRS S2, especially among companies with national or global footprints.

In Europe, greater clarity is expected soon on the final version of the simplified ESRS, which is likely to support more consistent and accessible disclosures. The revised standards, following the Omnibus proposal, are expected to streamline reporting requirements while maintaining ESRS’s robustness as a comprehensive sustainability framework. For European companies outside the scope of ESRS, the VSME standard will serve as the recommended voluntary framework. However, some may still opt to report using ESRS, recognizing its broader coverage and alignment with global expectations.

Despite the rise of regulatory frameworks, multi-framework reporting remains relevant, particularly in voluntary settings. GRI continues to play a complementary role, offering broader sustainability coverage that can enhance disclosures under IFRS. While IFRS S1 and S2 emphasize financial materiality and decision-useful information for capital markets, GRI’s focus on stakeholder inclusiveness and double materiality can complement these disclosures – particularly for companies with diverse stakeholder bases or those seeking to maintain consistency with previous reporting approaches.