CARB Updates on California Climate Laws: SB 253 & SB 261 Guidance

NOTE: This blog was originally published on September 2, 2025. It has been updated on September 4, 2025 to provide additional information provided in the Climate Related Financial Risk Disclosures: Draft Checklist released by CARB on September 2, 2025.

California Climate Accountability Package: What You Need to Know

The California Air Resources Board (CARB) hosted a public workshop on August 21 to discuss the California Climate Accountability Package (CCAP). This was the second of two workshops hosted by CARB this summer. To read ISS-Corporate’s summary of the first workshop on May 29, click here.

The CCAP requires companies doing business in California to annually disclose scopes 1, 2, and 3 greenhouse gas emissions (SB 253) and to biennially report on climate-related financial risks (SB 261). The two laws are also collectively referred to as “the 200s.”

The latest workshop proposed key clarifications for the laws including updated definitions, reporting timelines, fee payments, and minimum reporting requirements. In addition, CARB released a draft checklist for SB 261 compliance on September 2, 2025. However, full regulatory guidance is still a work-in-progress and expected to be released by the end of the year, leaving little time for covered entities to incorporate relevant updates.

ISS-Corporate Key Takeaways

- Definitions and scope are still pending: Definitions for “revenue”, “doing business in California”, and parent-subsidiary considerations have yet to be finalized. CARB requested additional public feedback.

- Proposed exemptions under SB 253 and SB 261: CARB proposed certain entities to be exempt from reporting, including non-profits, government entities, and companies whose only business in California is the presence of teleworking employees.

- New implementation fee structure: CARB proposed a new flat fee structure, with the fees adjusted annually for inflation. CARB estimated the 2026 fees for SB 253 and SB 261 to be $3,106, and $1,403, respectively. Entities that are subject to both regulations must pay both fees.

- Updated reporting deadlines: For SB 261, reporting deadline of January 1, 2026, remains firm. Starting December 1, 2025, companies can submit their climate reports to a public docket. For SB 253, CARB proposed a deadline of June 30, 2026, for scopes 1 and 2 emissions.

- Regulatory guidance timeline: CARB released a draft checklist for SB 261 on September 2, 2025 (details below). CARB plans to release additional guidance, including a draft reporting template for scopes 1 and 2 emissions (SB 253) by the end of September 2025 and a notice for rulemaking by October 14, 2025.

CARB Guidance Released on September 2nd Provides Draft Checklist for Climate Related Financial Risk Disclosures

As mentioned in the workshop, CARB released a draft checklist for climate related financial risk disclosures. This includes answers to frequently asked questions and a starting point for reporting entities to use in understanding potential compliances options. CARB emphasizes that a key guiding principal for preparers should be that “disclosures should reflect a company’s effort to assess and communicate risk.” Key details from the draft checklist include:

- Scenario Analysis: CARB acknowledged feedback that conducting detailed quantitative scenario analysis may cause undue burden for some reporting entities. Therefore, where “feasible and relevant”, CARB encourages companies to conduct a qualitative-based scenario assessment for initial reports due on January 1, 2026.

- Metrics & Targets: Reporting scopes 1, 2, and 3 emissions is a core recommendation for TCFD and IFRS S2-alignment. However, CARB acknowledged that including these metrics as part of SB 261 compliance may not be feasible for some companies by the initial deadline of January 1, 2026, as well as potentially duplicative for companies in scope of SB 253. Therefore, CARB is not including greenhouse gas emissions as a minimum requirement for the initial reporting period.

- FY or CY Data: CARB noted that SB 261 does not specify whether climate related risk information should cover the previous fiscal year or calendar year. As such, companies should use the “most recent/best available data” for reports due on January 1, 2026.

CARB Workshop Regulatory Updates

The August 21 workshop introduced proposed clarifications for key aspects of the laws.

Proposed Clarifications for Covered Entities

CARB has yet to formalize definitions for “revenue,” “doing business in California,” and parent-subsidiary considerations. CARB is seeking feedback on the concepts presented in both workshops until September 11. CARB has also compiled a list of entities potentially in scope for SB 253 (~2,600 entities) and SB 261 (~4,200 entities) and stated its intent to publish these lists in the coming weeks. CARB noted the lists are not definitive, and the responsibility is on companies to determine if they are covered under the laws.

Additionally, CARB presented a proposed list of entities to be exempted from SB 253 and SB 261 reporting, including:

- Non-profits

- Companies whose only business in California is the presence of teleworking employees

- Government entities

- Business entities whose only activity in California consists of wholesale electricity transactions that occur in interstate commerce

CARB’s Implementation Fee Proposal

SB 253 and SB 261 authorize CARB to assess an annual fee to cover the costs of implementation and administration of the laws. CARB proposed a flat annual fee that would be adjusted for inflation in future years. The current estimated fees for 2026 are $3,106 (SB 253) and $1,403 (SB 261), though these numbers are not final. Entities in scope of both laws would be subject to both fees.

Climate Risk Reporting Guidance

To help companies comply with SB 261, CARB shared existing resources on climate risk reporting from the TCFD and IFRS S2. CARB also shared the following requirements for SB 261 disclosures:

- Entities may use the TCFD, IFRS, or related standards as a framework for the report

- Each submitted report must include a statement on:

- The reporting framework applied (TCFD, IFRS S2, or other related standards)

- Which recommendations and disclosures from the framework have been compiled and which have not

- For the recommendations that have not been compiled, an explanation as to why the disclosures are not included and plans for future disclosures

TCFD Pillars as Reporting Foundations

Lastly, CARB discussed the foundational pillars of the TCFD framework that form the basis of any climate-related risk disclosure:

- Governance: Disclosure of the organization’s governance around climate-related risks and opportunities, such as board oversight and management’s responsibilities.

- Strategy: Disclosure of the actual and potential impacts of climate-related risks and opportunities on the organization’s operations, strategy, and financial planning.

- Risk management: Disclosure of how the organization identifies, assesses, and manages climate-related risks.

- Metrics and targets: Disclosure of the metrics and targets used to assess and manage relevant climate-related risks and opportunities.

Assurance Requirements

SB 253 requires third-party assurance on emissions reporting. CARB proposed the below list of potential assurance standards and emphasized that this list is available for public feedback:

- ISSA 5000 (IAASB)

- AA1000

- ISO 14060 family

- AICPA

Reporting Deadlines

CARB confirmed the January 1, 2026, deadline for SB 261 or the Climate-Related Financial Risk Report will not change. There will be a public docket for entities to post the public links to their reports available on December 1, 2025.

For SB 253, CARB proposed a June 30, 2026, implementation deadline for scopes 1 and 2 reporting. CARB stated its intent to release draft reporting templates for scopes 1 and 2 reporting by the end of September 2025.

Regulatory Summary: SB 253 & SB 261

Please see a summary table of the laws below, with proposed updates from the August 21, 2025, workshop highlighted in footnotes:

| SB 253 | SB 261 | |

| Goal |

Increase transparency by requiring companies to measure and disclose their scopes 1, 2, and 3 emissions. | Increase transparency and integrate material climate-related financial risks into corporate strategies. |

| Disclosure Requirements & Deadlines | CY 2026[1]: Annual disclosure of prior fiscal year’s scope 1 and 2 emissions.

CY 2027: Annual disclosure of prior fiscal year’s scope 1, 2, and 3 emissions. |

Jan. 1, 2026: Biennial publication of a climate-related financial risk report in accordance with TCFD or an equivalent reporting framework (e.g., IFRS). |

| Companies in Scope [2] [3] [4] | Public and private U.S. companies that do business in California and have revenues >$1B. | Public and private U.S. companies that do business in California and have revenues >$500M (insurance businesses are exempt). |

| Disclosure Format | Own website: The reporting entity must make the report publicly available on its own website.

Public repository: CARB has stated its intention to work with a third party to create a publicly accessible digital platform that will receive and publish emissions data from reporting entities. |

Own website: The reporting entity must make the report publicly available on its own website.

Public repository: On December 1, 2025, CARB will post a public docket for covered entities to post a public link to their first climate risk report. This docket will help support transparency by providing one location for the public to view all reports. |

| Assurance Requirements | Scopes 1 & 2: Limited assurance beginning in 2026, and reasonable assurance beginning in 2030.

Scope 3: Limited assurance beginning in 2030. |

None. |

| Penalties | Penalties shall not exceed $500,000 in a reporting year.

|

Penalties shall not exceed $50,000 in a reporting year.

|

| 2026 First-year Reporting Leniency |

In December 2024, CARB released an Enforcement Notice stating that entities may use existing emissions data from prior fiscal years for the first year of reporting and that CARB will use discretion for the first reporting cycle as long as companies show good faith effort to comply. | In July 2025, CARB released an FAQ document stating that initial climate-related financial risk reports submitted by January 1, 2026, may cover fiscal years 2023/2024 or 2024/2025, given the burden on companies to collect this data. |

CARB’s Next Steps & How to Stay Ahead

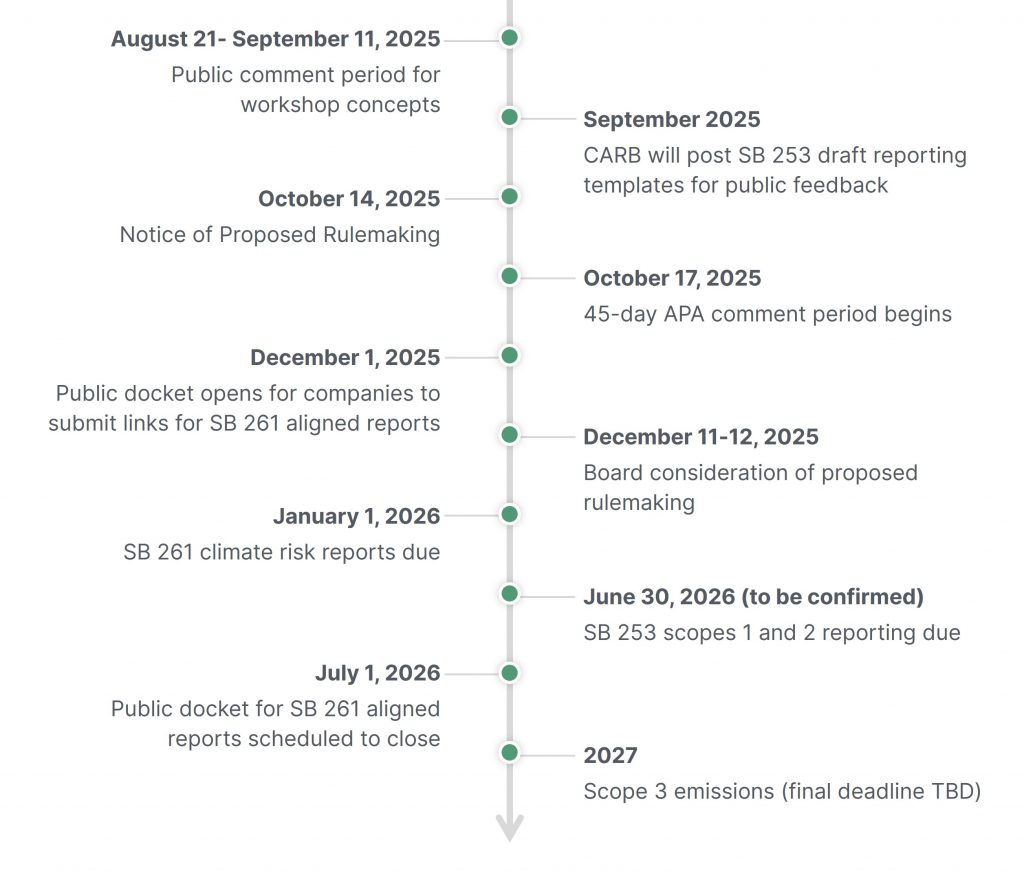

CARB’s Draft Timeline for Rulemaking

CARB is seeking stakeholder feedback on information presented during the August 21 workshop. To provide feedback, stakeholders can email CARB directly at climatedisclosure@arb.ca.gov or submit a comment here.

While full regulatory guidance is still pending, CARB reiterated the initial reporting deadline of January 1, 2026, for SB 261 has not changed. For entities that have not published greenhouse gas emissions and/or a climate-related risk report before, both disclosures are large undertakings which could require months of work. While it would be ideal to have full regulatory guidance sooner rather than later to know exactly what is required for compliance, companies are encouraged to start preparing these disclosures as soon as possible to meet the January 1, 2026, deadline.

Footnotes

[1] On August 21, 2025, CARB proposed a deadline of June 30, 2026, but this has yet to be finalized.

[2] Final definitions of “revenue” and “doing business in California” are yet to be determined by CARB.

[3] Reports may be consolidated at the parent company level. If a subsidiary of a parent company meets the outlined criteria, they are not required to prepare a separate report.

[4] On August 21, 2025, CARB proposed the following entities be exempt: (1) Non-profits; (2) A company whose only business in California is the presence of teleworking employees; (3) Government entities; and (4) A business entity whose only activity in California consists of wholesale electricity transactions that occur in interstate commerce. These exemptions have yet to be finalized.