FTSE 350: Board, Committee Chair Shareholder Support Can Signal Governance Concerns

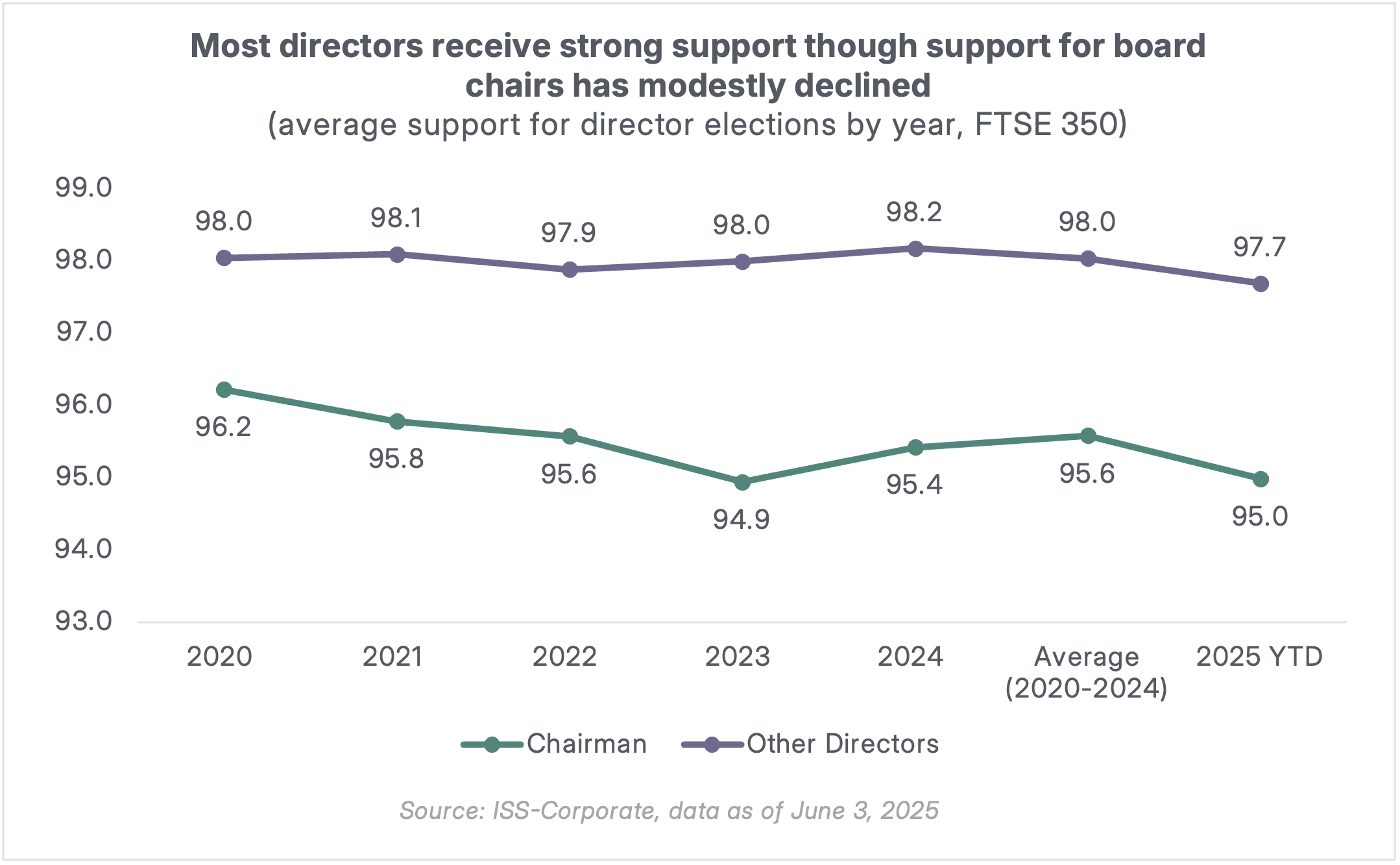

Director elections on the FTSE 350 over the past five years reveal a growing gap between support for board and committee chairs and all other board members seeking re-election. Board chairs have been receiving lower support than other directors as investors scrutinize their performance more closely and often hold them more accountable for corporate governance concerns at the company.

Institutional investors’ policies have also evolved, with more accountability expected from directors in board and committee chair positions. Despite these issues, directors of FTSE 350 companies continue to enjoy a high level of approval from shareholders, with directors (excluding board chairs) receiving average shareholder support of 98.0% over the past five years.

Based on past board chair elections, the most prominent drivers of investor dissent include:

- Accountability for the company’s corporate governance shortcomings

The board chair bears responsibility for the overall effectiveness of the board and, consequently, is held accountable when governance practices deviate from market expectations. These can include concerns over board independence, board diversity, inadequate responsiveness to significant shareholder dissent, as well as ineffective oversight of management. - Overboarding

Board chairs are expected to dedicate significant amount of time to the company and its board, and their outside commitments can prompt shareholder opposition. Many institutional investors closely scrutinize the number of other public company board seats held by a board chair. The board chair position often accounts for higher weights than the non-executive director role when calculating a director’s total board mandates. This can lead to a view that a board chair is holding excessive board seats, or “overboarding,” which in turn could cast doubt on effective board monitoring and participation. - Long tenure

Chairs who have held the role for an extended period of time are often assessed more carefully by investors. Factors including the number of years served in the role, succession planning, and concurrent tenure with the incumbent executives can impact investor votes on whether to re-elect the board chair. - Lack of independence

The UK Corporate Governance Code requires that the board chair should be independent and the roles of chair and chief executive should not be held by the same individual. The Code states that the designation of an executive chair could be interpreted negatively by investors as evidence of one individual combining leading the board with bearing some executive responsibility for the company’s operations. Proposals to elect a combined CEO and Chair usually prompt notable shareholder dissent.

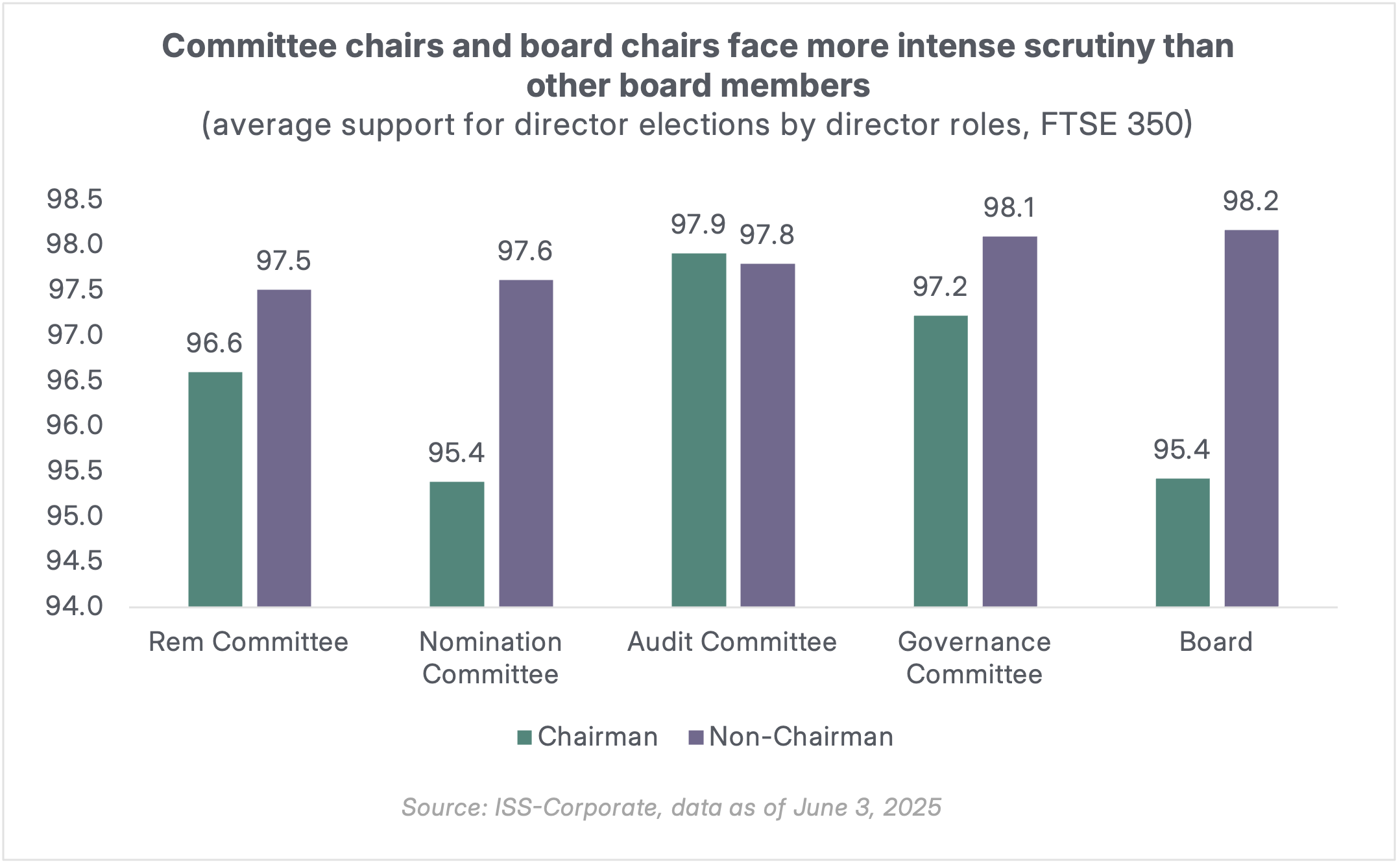

Similarly, committee chairs are also likely to be held accountable for specific corporate governance concerns. The voting data suggests that nomination and remuneration committee chairs face particularly intense scrutiny, as shown by greater investor dissent. This may be attributed to the fact that when any diversity issues are identified, investors often voice their concern by opposing the re-election of the nomination committee chair. Other concerns related to the board composition, such as independence, refreshment and directors’ commitment and accountability can also lead to lower support on nomination committee chairs. For the remuneration committee chairs, consistent concerns with a company’s remuneration arrangements can lead to shareholder opposition on re-election of remuneration committee chairs.

Conclusion

While failed elections of directors are extremely rare among FTSE 350 companies, our study shows that senior board members (board chair and committee chairs) tend to attract greater shareholder dissent, which may signal potential shareholder discontent for certain corporate governance practices. Among the director election proposals which received more than 10% shareholder dissent over the last five years, 29.6% of them are for Board Chairs, 29.8% are for Nomination Committee Chairs, and 15.7% are for Remuneration Committee Chairs. Given the crucial role the senior directors play in a company’s overall governance, it is essential for companies to proactively address shareholder concerns through active engagement and enhanced transparency.