Global Sustainability Pulse: Key Trends in Corporate Strategy and Disclosure

Global sustainability efforts remain steady or growing, though regional dynamics introduce varying levels of momentum and uncertainty in disclosures.

Between August 25 and September 19, ISS-Corporate conducted a global survey of corporate issuers to assess evolving priorities in corporate sustainability. The survey sought to capture corporate perspectives on the development of sustainability strategies, reporting practices, and key focus areas in response to market and regulatory shifts over the past year. It also explored expectations for how these priorities may continue to evolve in the years ahead.

A total of 220 respondents participated, representing companies of various sizes across all major regions and sectors. Of these, 93 were based in the Americas, 65 in Asia Pacific, and 62 in EMEA.

The findings reveal dynamic shifts in the sustainability landscape, shaped by regulatory developments and broader market trends. They also highlight notable regional differences in how companies are approaching sustainability today – and how they anticipate doing so in the future.

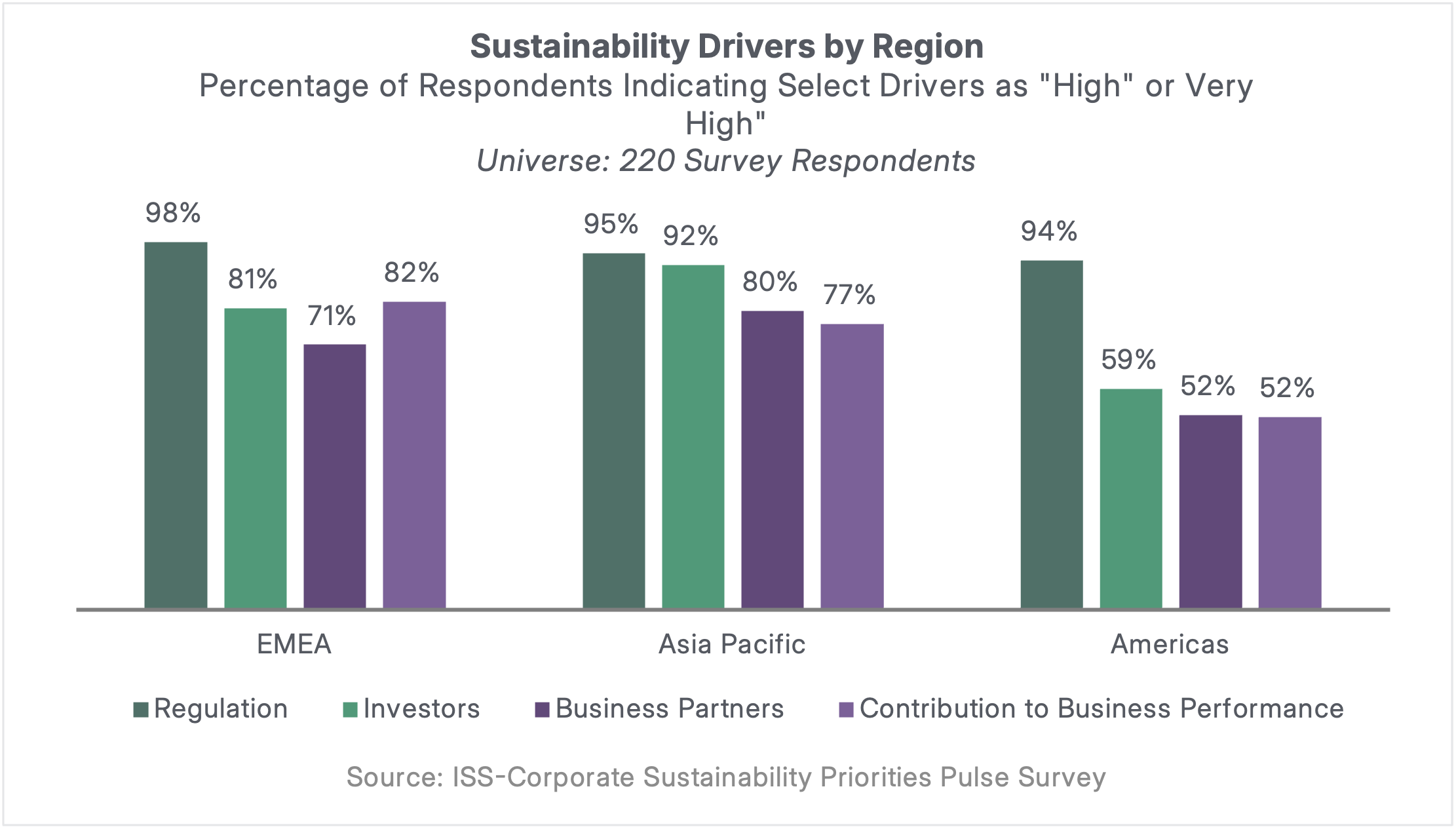

Regulation Leads as Key Driver of Corporate Sustainability in 2025

Regulation emerged as the most prominent driver of corporate sustainability, with 95% of respondents rating it as having “high” or “very high” importance for their organization (other response options included “moderate,” “low,” and “very low”). This strong emphasis on regulation was consistent across all regions.

However, regional differences became apparent when evaluating other potential drivers – such as investor expectations, business partner requirements, and the contribution of sustainability to overall company performance. These factors were rated as “high” or “very high” in importance by more than 70% of respondents in EMEA and Asia Pacific, indicating a broader set of motivations driving sustainability efforts in these regions.

Notably, 82% of European respondents identified sustainability’s contribution to company performance as a major driver, reflecting alignment with the Corporate Sustainability Reporting Directive (CSRD). While the CSRD is undergoing simplification through the EU Omnibus initiative, its core principles remain intact for in-scope companies and are expected to continue shaping the European reporting landscape.

In contrast, fewer than 60% of respondents in the Americas rated investor expectations, business partner requirements, or sustainability’s contribution to company performance as highly important drivers. The data suggests a more regulation-driven approach to sustainability in the region.

The emphasis on regulation may be influenced by shifting political dynamics in the United States, where 81 of the 93 Americas-based respondents represented U.S. companies. Increasing scrutiny and skepticism from both federal and state-level actors toward sustainability-related corporate practices may be shaping how companies prioritize and communicate their sustainability strategies.

Sustainability Strategies Hold Steady, with Diverging Regional Trends

The survey explored how companies are responding to shifts in the political and regulatory landscape by asking: “How have external developments over the past 12 months (e.g., political, market, regulatory) influenced your organization’s sustainability strategy?” Across all regions, the majority of respondents indicated that their organizations are either maintaining or expanding their sustainability efforts. However, regional differences were evident.

In Asia Pacific, 49% of respondents reported a moderate or significant expansion in their sustainability programs, followed closely by 39% in EMEA. In contrast, only 31% of respondents in the Americas reported similar levels of expansion. A substantial portion of companies in EMEA and Asia Pacific – 50% and 49% respectively – indicated they are maintaining their current commitments with minor adjustments, a response categorized as “Continued Focus.” In the Americas, 43% of respondents selected this option.

When it comes to scaling back sustainability efforts, the trend was minimal in EMEA and Asia Pacific, with only 11% and 2% of respondents respectively reporting moderate or significant reductions. However, in the Americas, approximately 26% of respondents indicated a pullback in their sustainability programs, suggesting a more cautious or reactive approach in that region.

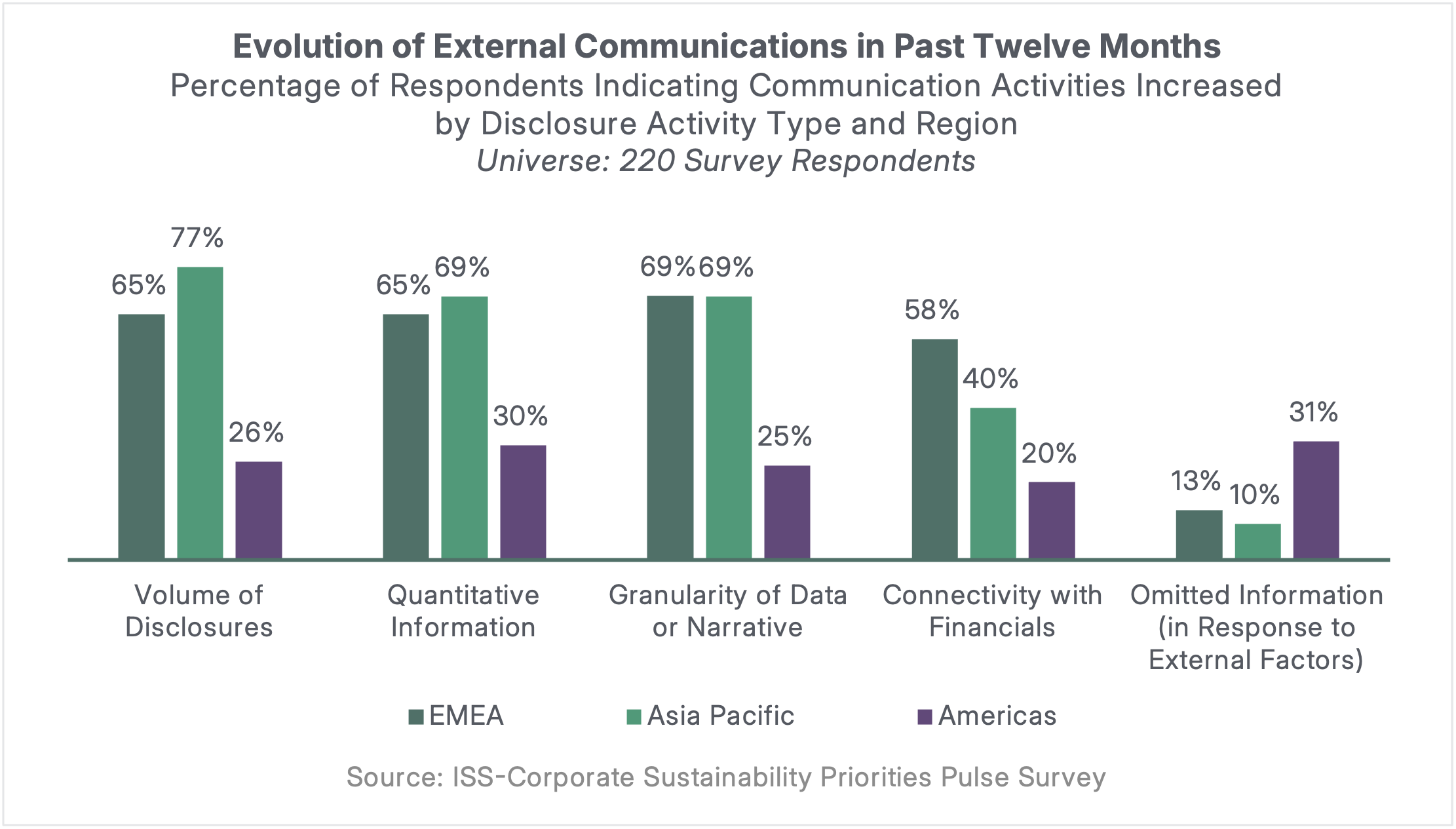

Disclosures Expanding Significantly in EMEA and Asia Pacific

When asked about potential impacts on sustainability communications, respondents pointed to a continued expansion in disclosures – both in volume and in the granularity of information. This includes a rise in quantitative data and stronger integration with financial reporting. The trend is especially pronounced in EMEA and Asia Pacific, where nearly 70% of companies anticipate increases in disclosure volume, detail, and use of quantitative metrics. In these regions, evolving regulations are driving momentum toward standardized disclosures that reflect both financial and impact materiality. In EMEA and Asia Pacific, the share of companies expecting to reduce disclosures remains in single digits across various categories

Despite the EU’s recent scaling back of ESRS requirements under the Omnibus plan, European companies remain committed to integrated reporting, embedding sustainability within their financial disclosures. Key jurisdictions in Asia Pacific – such as Japan, South Korea, Taiwan, and Australia – are also advancing in this direction.

In contrast, the U.S. regulatory landscape is more contentious, with actions that challenge rather than simply reassess sustainability practices. As a result, disclosure growth in the Americas is more tempered. Most companies (53% to 59%, depending on disclosure dimension) report no change in their disclosure levels, while 25% to 30% expect increases in disclosure volume, quantitative information, and granularity. However, a notable minority (14% to 22%) anticipate a decrease in disclosure activity.

When asked specifically whether companies are omitting disclosures due to litigation risks tied to shifting political dynamics, 31% of respondents in the Americas said yes – compared to just 13% in EMEA and 10% in Asia Pacific.

While disclosure growth in the Americas is less pronounced, it’s important to note that approximately 80% of companies in the region still report either maintaining or increasing the volume and granularity of their sustainability disclosures.

Looking Ahead: Global Convergence or Regional Divergence?

Survey responses point to a sustained global focus on sustainability, though with a more cautious tone in the Americas – largely influenced by political dynamics in the United States. While no significant pullback is evident at this time, shifts in sentiment raise important questions about the future landscape: Will sustainability disclosures continue to converge globally, or are we entering a phase of regional divergence? And what might this mean for business standards and the integration of practices across multinational firms?

These are critical trends we will continue to monitor closely.

Stay tuned for future publications, where we’ll delve deeper into these survey findings – including respondents’ outlook for the next two years. We’ll explore anticipated expansion across key topical areas (e.g., climate, nature, human rights) and examine planned investments in internal sustainability capabilities such as data collection, supply chain due diligence, and materiality assessments.