Latin America’s Sustainability Reporting Gains Momentum

Latin America accelerates sustainability reporting, driven by IFRS adoption, climate mandates, and supply chain due diligence – strengthening global alignment and investor confidence.

2025 was marked by headlines spotlighting sustainability reporting developments in North America and Europe – regions where regulatory mandates dominate the dialogue and legal challenges often make news. Meanwhile, Latin America has been steadily advancing its own sustainability agenda, with progress that merits closer attention. From Brazil to Mexico, Chile, and Colombia, companies and regulators are shaping disclosure practices that align with global standards and strengthen the region’s competitive position in international markets.

Key Regulatory and Market Drivers Across the Region

Alignment with global standards is a key driver, as Brazil and Mexico have signaled adoption of IFRS S1 and S2, embedding international best practices into local frameworks. In Brazil, Resolution CVM No. 193 introduced voluntary adoption since 2024, with mandatory adoption effective on January 1, 2026 for listed companies and certain regulated entities. Assurance requirements follow a phased approach: limited assurance for reports covering fiscal year 2025 and reasonable assurance for those covering fiscal year 2026. Similarly, in Mexico, January 2025 CNBV resolution published in the Diario Oficial de la Federación requires companies to prepare reports aligned with IFRS S1 and S2 for fiscal year 2025, submitted in 2026, with limited assurance starting in 2027 and reasonable assurance from 2028 onward.

Chile and Colombia are also advancing sustainability, though at different stages. Chile’s NCG 461 mandates listed companies to disclose governance, strategy, risk management, and metrics aligned with TCFD and SASB. The country has signaled plans to integrate IFRS S1 and S2 by 2026. Colombia, meanwhile, introduced Guideline No. 100-000002 in 2025, encouraging voluntary sustainability reports (Report 08) covering sustainability and governance disclosures. While IFRS adoption is not yet mandatory, Colombia participates in an IFRS Foundation–IDB partnership focused on capacity building and future alignment.

Power your reporting metrics in evolving regions with our Climate Solutions »

Trends in Sustainability Disclosures

ISS-Corporate analyzed corporate public disclosures from Latin American companies included in the ISS E&S Raw Data dataset. The analysis focuses primarily on companies based in Brazil (78 companies under coverage in 2025), Chile (29 companies), and Mexico (37 companies) – among the largest and most mature in these markets – representing a significant share of market capitalization in each. While the dataset does not capture the full breadth of these markets, it provides a strong indication of prevailing trends and the level of adoption of reporting and business practices.

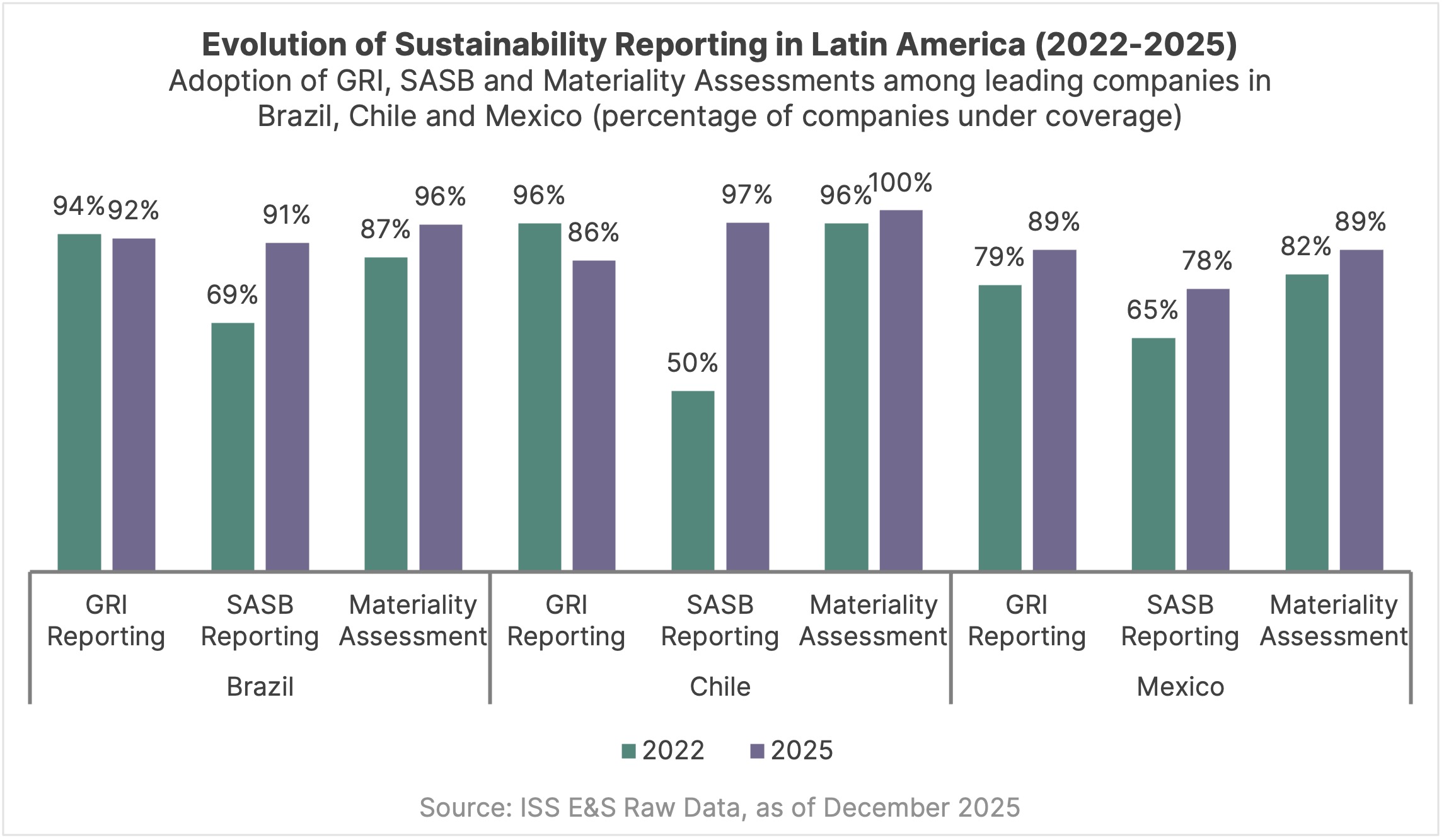

Framework Adoption and Materiality Assessments

Between 2022 and 2025, sustainability reporting in Latin America shifted markedly toward global standards, particularly SASB. Brazil and Chile saw the most significant gains in SASB adoption – jumping from 69% to 91% in Brazil and from 50% to 97% in Chile – driven largely by emerging regulatory requirements. Materiality assessments also advanced across all markets, reaching full adoption in Chile and notable increases in Brazil and Mexico. In contrast, GRI reporting declined slightly in Brazil and Chile, though it remains widely used, suggesting a pivot toward frameworks mandated by regulation and investor expectations. Mexico demonstrated steady progress across all dimensions, with meaningful improvement in SASB reporting, signaling broader convergence toward financially relevant disclosures.

Climate Reporting Gains Traction

Regulatory momentum and convergence with international standards have accelerated climate-related disclosures across the region. Chile leads with TCFD reporting rising from 54% to 76% and widespread adoption of GHG reduction targets and verification, reflecting mandates under NCG 461 and plans to integrate IFRS S1 and S2 by 2026. Brazil shows steady progress, particularly in third-party verification (65% to 81%), supported by CVM Resolution 193 and phased assurance requirements. Mexico’s gains are more modest, though improvements in TCFD reporting and targets signal early compliance with CNBV’s IFRS-aligned framework. As mandatory standards and assurance timelines take effect, these trends are expected to accelerate further, embedding climate considerations more deeply into corporate strategy across the region.

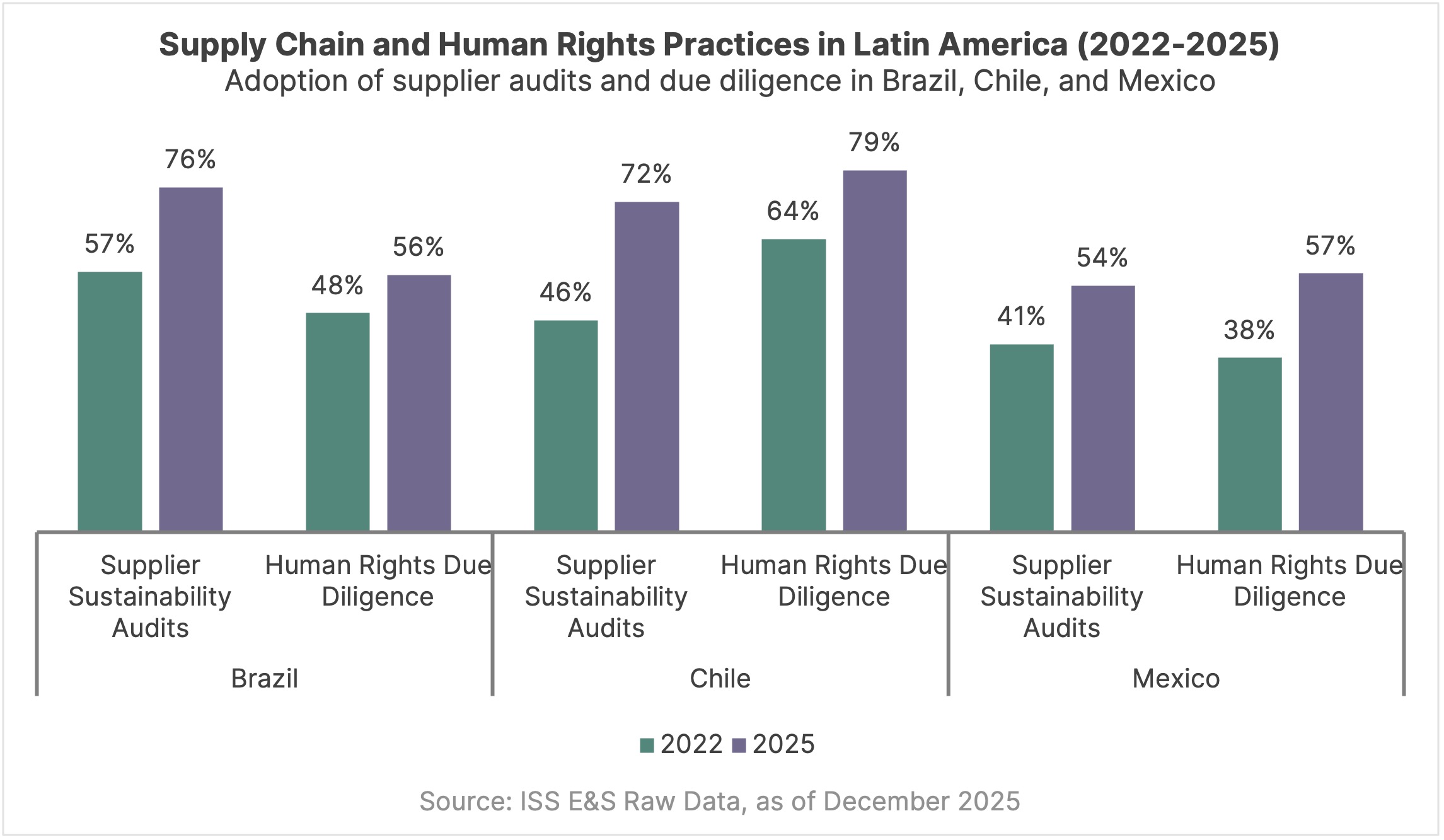

Supply Chain and Human Rights Practices Strengthen

Between 2022 and 2025, supplier sustainability audits increased notably across Latin America – rising from 57% to 76% in Brazil, 46% to 72% in Chile, and 41% to 54% in Mexico. In Brazil, this growth coincides with the introduction of Draft Bill 572/2022, which, if enacted, would require companies to implement human rights due diligence (HRDD) across their value chains. Brazil’s HRDD adoption also rose for companies under coverage (48% to 56%), reflecting movement towards alignment with anticipated obligations. In Chile, supplier audits (46% to 72%) and HRDD practices (64% to 79%) advanced alongside several bills under discussion in the Chilean National Congress (Bill Nos. 17.196-17, 17.446-17, 17.520-17) and the National Action Plan on Business and Human Rights. In Mexico, increases in both areas are primarily linked to trade-related requirements, including the USMCA’s forced labor provisions and recent enforcement measures. These trends highlight the combined influence of regulatory developments and evolving market expectations.

Sustaining Momentum

The data point to significant advancement across all major areas of sustainability practice among leading Latin American companies. These markets are adopting global best practices and positioning themselves to remain competitive and attractive to international investors and business partners. The direction of travel is clear, with emerging standards increasingly backed or shaped by regulatory action.

Brazil’s role as host of COP 30 in 2025 further underscores the region’s growing commitment to sustainable business and development. As regulatory frameworks continue to evolve and new initiatives take shape, Latin America’s progress will be important to watch – not only for local stakeholders but also for global market participants seeking resilient and responsible partners. Continued monitoring of legislative developments and market responses will be essential for understanding the trajectory and impact of sustainability in the region.