Science-Based Targets: Evolving Standards and Global Adoption

Science-based targets increasingly serve as a common reference point, with evolving standards shaping credibility, comparability, and corporate climate decision-making.

Companies increasingly use science-based targets as a common reference point for articulating and explaining their climate ambitions. At their core, science-based targets provide a consistent, science-based approach to setting and evaluating corporate climate targets, supported by independent review from the Science Based Targets initiative (SBTi). For investors and other external users, this independent validation is central: it introduces a level of credibility and comparability that allows climate targets to be assessed across companies and sectors, reducing reliance on self-defined or opaque benchmarks.

For companies, the continued uptake of science-based targets reflects a different, but related, set of considerations. Externally, validated targets support credible signaling to investors, customers, and business partners, and increasingly serve as a reference point for setting expectations within the value chain. Internally, the target-setting process helps translate long-term climate ambition into more structured planning discussions, informing decisions around operations, sourcing, and engagement with suppliers. Separately, disclosure frameworks such as IFRS S2 and the EU’s CSRD have increased scrutiny of how companies define climate targets, track progress, and explain transition plans. While these frameworks do not require science-based targets, leveraging science-based targets can serve as a structured and credible reference point for organizing climate-related disclosures and governance narratives.

Upcoming Changes to SBTi’s Net-Zero Standard

As science-based targets have moved into more mainstream use, the standards that define how those targets are set and assessed are also being revisited. SBTi periodically updates its Net-Zero Standard to reflect methodological developments, implementation experience, and feedback from companies and other stakeholders. At present, SBTi’s Net-Zero Standard Version 1.3 continues to apply to new target submissions through December 31, 2027. SBTi has indicated that an updated version of the standard is expected to be finalized in 2026, with the new requirements applying to targets submitted from January 1, 2028 onward.

Scope‑Specific Target Requirements

Based on consultation materials, the draft Net-Zero Standard Version 2 places greater emphasis on clarity, operational relevance, and accountability. A central proposed change is the separation of targets by emission scope, with distinct targets for Scope 1, Scope 2, and Scope 3. The intent is to prevent progress in one area from obscuring slower movement elsewhere, while aligning targets more directly with the operational levers companies control across operations, electricity procurement, and the value chain.

The draft also introduces expanded options for Scope 1 emissions, including alignment targets and Asset Decarbonization Plans linked to company-specific carbon budgets and asset replacement cycles. These approaches are designed to be more practical for asset-intensive sectors where decarbonization pathways are shaped by long investment horizons. For Scope 2, the framework proposes stronger integrity requirements around renewable electricity claims, including expectations related to timing and geographic relevance, particularly for large electricity consumers.

For Scope 3, the emphasis shifts toward categories with the highest emissions and greatest influence, supported by more action-based alignment options such as supplier engagement and low-carbon energy alignment. The draft also introduces Ongoing Emissions Responsibility, outlining a potential graduated approach under which larger companies in more advanced economies would assume increasing responsibility for ongoing emissions over time.

These changes suggest a more structured, scope-specific framework that reinforces governance, periodic re-validation, and clearer links to transition planning.

Advance your science‑based target implementation with our Climate Solutions »

Global Adoption Trends of Science-Based Targets

ISS-Corporate analysis reviewed science-based target adoption across a global universe of 9,063 publicly traded companies, using SBTi approval status to distinguish between validated targets (“approved”) and public commitments (“committed”). While overall adoption remains uneven, several clear patterns emerge by geography, company size, and sector.

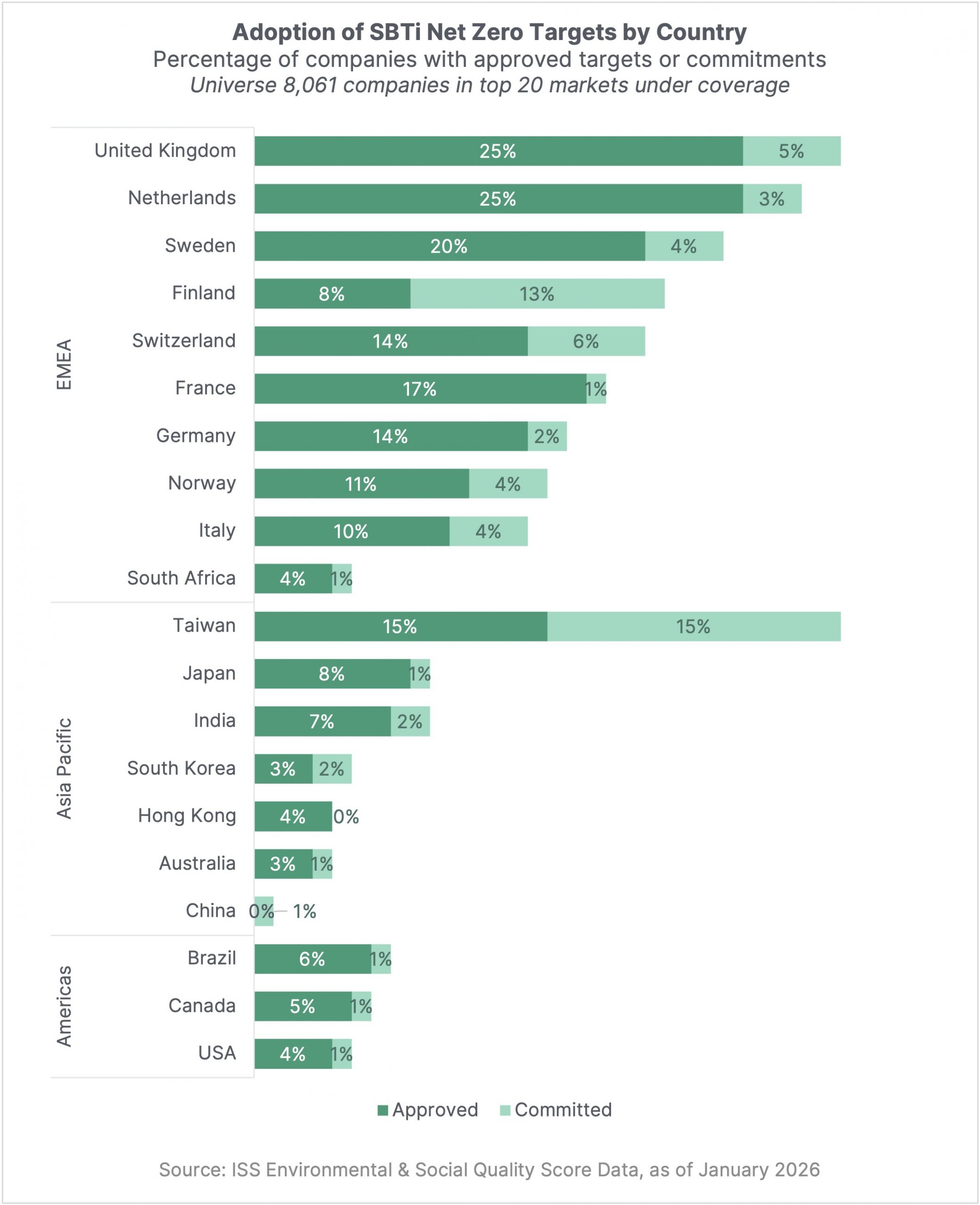

SBTi Adoption Differences by Geography

Adoption of science-based net-zero targets varies meaningfully by market, with the highest overall uptake concentrated in parts of Northern and Western Europe. The United Kingdom and the Netherlands (both at an adoption rate of 25% approved) lead the dataset, followed by Sweden (20%) and France (17%). Other European markets – including Germany and Switzerland (14% each) and Norway (11%) – show more moderate but still notable adoption, while Finland stands out for a relatively high share of commitments that have not yet translated into approvals.

In Asia-Pacific, adoption remains selective rather than uniform. Taiwan stands out, with a combined 30% either approved or committed, reflecting the market’s growing institutionalization of sustainability reporting and climate governance. Japan shows lower net-zero uptake (8% approved), while levels remain limited in South Korea, Hong Kong, and Australia, and minimal in China, where commitments exceed approvals but overall net-zero validation remains very limited.

Adoption across the Americas is more modest. The United States (4% approved) and Canada (5%) trail European leaders, while Brazil (6%) shows slightly higher uptake within a relatively small cohort of adopters. Overall, the distribution suggests that net-zero target validation remains concentrated in markets where disclosure expectations, investor scrutiny, and climate-related governance practices are already relatively well established.

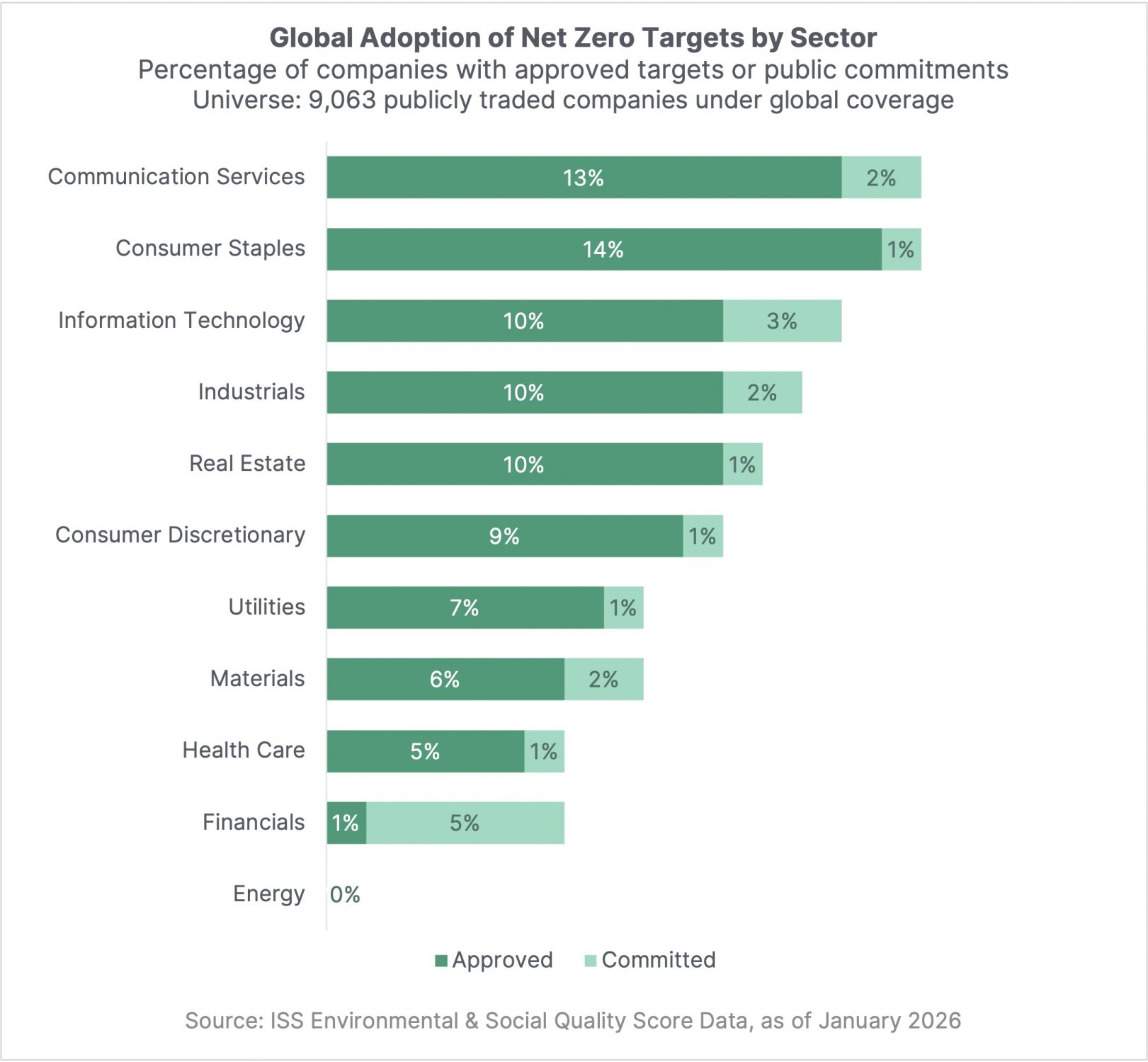

Sector-Based SBTi Adoption Patterns

Sectoral patterns highlight meaningful differences in how science-based net-zero targets are being adopted across the economy. Consumer Staples (14% approved) and Communication Services (13%) show the highest levels of validated uptake, followed by Information Technology, Industrials, and Real Estate (each around 10% approved). These sectors tend to combine material operational or value-chain emissions with relatively well-defined levers for target-setting, reporting, and investor scrutiny.

Consumer Discretionary (9%) sits slightly below this group, while adoption is more limited in Utilities (7%) and Materials (6%), where decarbonization pathways are shaped by higher capital intensity, long-lived assets, and greater dependence on sector-specific technologies and infrastructure. Health Care (5%) also shows relatively low uptake, reflecting different structural factors: the listed universe is more heavily weighted toward smaller and mid-cap firms, many of which are earlier in their climate target-setting efforts despite generally lower direct emissions intensity.

Financials stand out for a different reason: approved net zero-targets remain rare (1% approved), while commitments are comparatively higher (5%), reflecting ongoing methodological development for financed emissions and continued calibration following SBTi’s financial sector guidance. Energy shows no approved or committed net-zero targets in this snapshot, consistent with the absence of an active Oil & Gas pathway under SBTi and the resulting constraints on validation. SBTi’s Oil & Gas Standard has progressed through scoping, consultation, and technical review and is currently paused as part of its structured technical workplan.

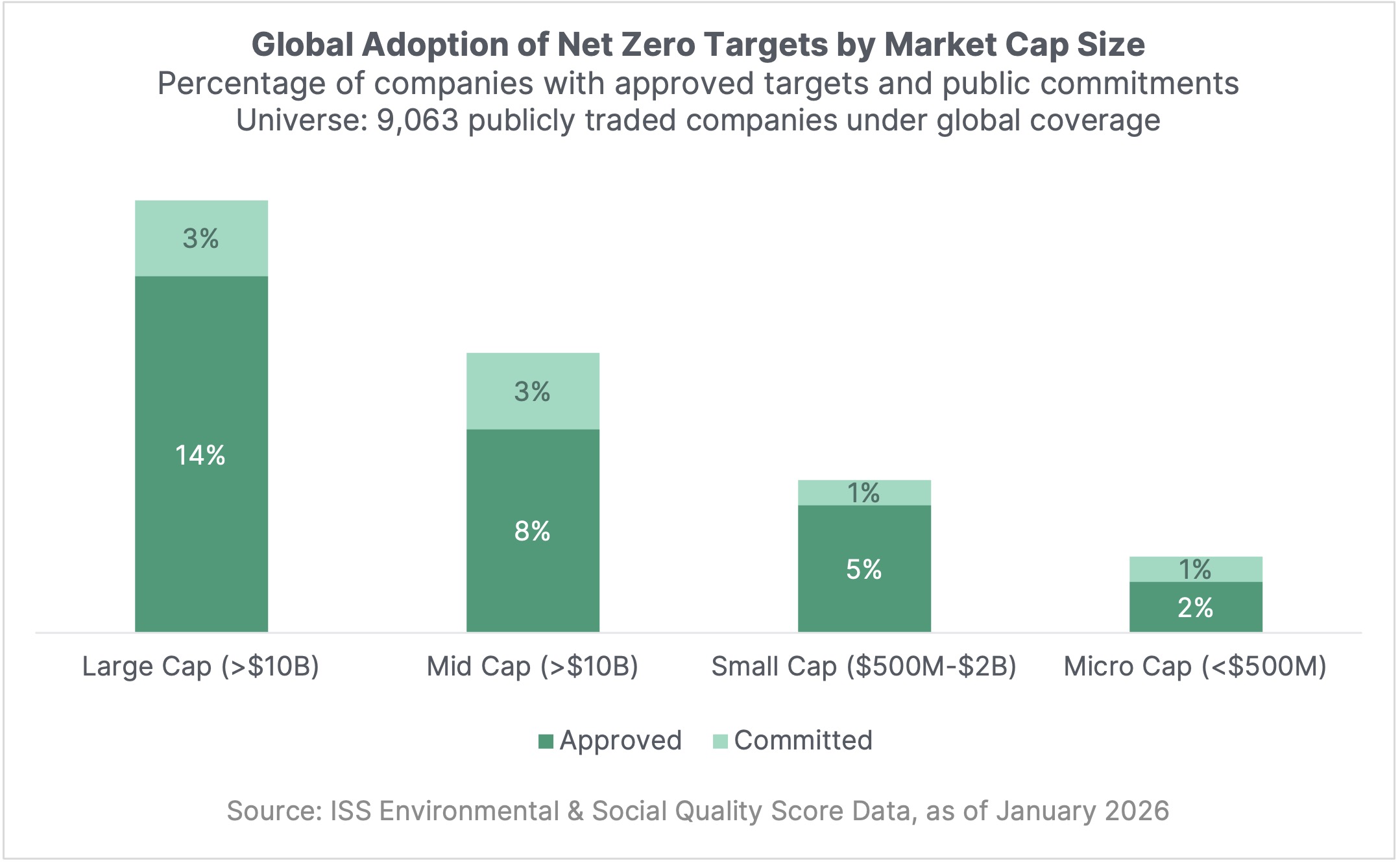

Market Cap-Driven SBTi Variations

Company size is a meaningful differentiator. Adoption increases materially with market capitalization, reaching 14% of approved targets among companies with market values above $10 billion, compared with low single‑digit levels among mid cap and small cap firms. Larger organizations typically face more sustained capital‑market scrutiny, clearer value‑chain expectations, and greater capacity to invest in emissions data systems, governance structures, and third‑party verification.

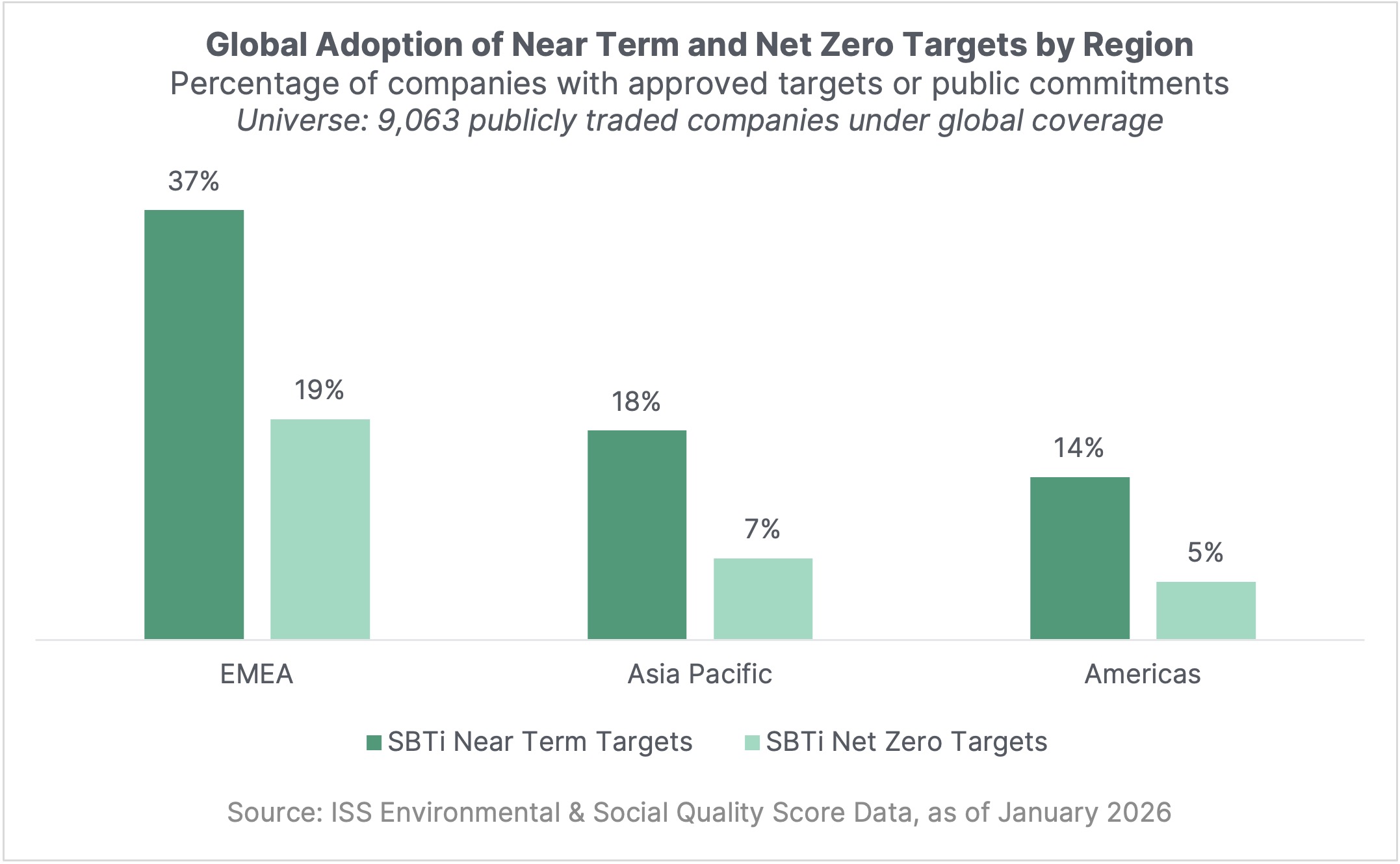

Across regions and sectors, near‑term targets remain considerably more prevalent than net‑zero targets, exceeding them by more than two‑to‑one. This pattern reflects the more immediate actionability of near‑term pathways, as well as their role as a required step within SBTi’s target‑setting framework. The sequencing from near‑term to net‑zero targets is therefore likely to persist as governance, validation, and re‑assessment expectations continue to develop.

Practical Pathways to Credible Climate Targets

For companies considering science-based targets, effective implementation tends to hinge less on ambition than on preparation, sequencing, and governance. Several practical approaches consistently distinguish more durable target-setting efforts from those that later require revision.

-

- Start with materiality and credible baselines. Robust Scope 1, Scope 2, and Scope 3 inventories – developed in line with the GHG Protocol – provide the foundation for credible targets. Emphasis on primary data for the most material categories, alongside a clearly justified base year, reduces downstream adjustments and supports validation and assurance.

- Embed targets within a board-approved transition plan. Rather than standing alone, science-based targets are most effective when integrated into enterprise strategy. Decision-useful plans integrate governance structures, interim milestones, capital allocation, and internal accountability – elements emphasized under IFRS S2 and reflected in SBTi’s evolving expectations.

- Use procurement as a decarbonization lever. For many companies, Scope 3 emissions dominate the footprint. Supplier alignment pathways, activity pools, and targeted engagement in high-impact categories can focus effort where influence is greatest. Embedding climate expectations into procurement processes, contracts, and supplier performance reviews strengthens execution.

- Develop a credible electricity strategy. Anticipated tightening of Scope 2 integrity expectations underscores the importance of a structured approach to electricity sourcing. Companies increasingly develop roadmaps that combine power purchase agreements, market-based instruments, and load-shaping measures, with attention to timing and geographic relevance.

- Prepare for disclosure and assurance. Aligning internal processes with IFRS S2 and, where relevant, CSRD/ESRS disclosure requirements supports consistency across targets, risk management, and transition planning, and can reduce friction as assurance expectations evolve.

Alternatives for Companies Not Yet Ready for Validation

For companies not yet ready for full SBTi validation, several credible alternatives can still support progress. These include setting internal science-aligned targets without external validation, making public supplier-engagement commitments in priority categories, publishing board-approved climate transition plans aligned with IFRS S2 or CSRD, or piloting asset-level decarbonization initiatives with limited assurance. In practice, these approaches can help build the data quality, governance, and operational experience needed for future target validation.

Ultimately, science-based targets function less as an endpoint than as a reference point. They help investors assess the credibility and comparability of climate commitments and provide companies with one structured way to translate climate ambition into planning, governance, and disclosure practices. As standards and stakeholder expectations evolve, the practical value of science‑based targets will depend less on form than on whether climate objectives are supported by coherent strategies, robust data, and execution that can be assessed externally.