Spain Introduces Mandatory Climate Disclosure

Spain’s climate disclosure law offers companies – both domestic and international – a clearer framework for reporting and compliance at a time when EU-level reporting requirements remain in flux. National initiatives like this are helping set the pace for climate reporting across the region.

In response to increasingly severe climate impacts – including record-breaking temperatures, wildfires, and floods – the Spanish government has introduced Royal Decree 214/2025 as part of its broader national Climate Emergency Plan. This new legislation introduces mandatory climate disclosure requirements for companies and public entities operating in Spain, with the aim of advancing the country’s goal of achieving climate neutrality by 2050.

Overview of Royal Decree 214/2025

Starting in 2026, a large number of companies either incorporated in Spain or conducting business there will be required to report their greenhouse gas (GHG) emissions and publish credible reduction plans. The decree also helps address gaps left by delays and potential revisions to the EU’s Corporate Sustainability Reporting Directive (CSRD), particularly in relation to climate-specific disclosures.

Who is in scope:

-

- Companies with over 500 employees or those classified as public interest entities under the EU Non-Financial Reporting Directive (NFRD)

- Companies with more than 250 employees that are either:

-

-

- Public interest entities (excluding SMEs), or

- Meet at least one of the following for two consecutive financial years:

-

-

- Total assets exceed EUR 20 million

- Net annual turnover exceeds EUR 40 million

-

-

What to report:

1. Greenhouse Gas (GHG) Emissions

-

-

- Scope 1 and Scope 2 emissions: Mandatory for all in-scope entities starting in 2026, covering emissions from fiscal year 2025.

- Scope 3 emissions: Required from 2028, but only for public sector bodies. This disclosure requirement includes indirect emissions across the value chain, such as those from suppliers and product use.2. GHG Reduction Plans

-

2. GHG Reduction Plans

Companies must publish a credible and detailed plan to reduce emissions, with the following minimum requirements:

-

-

- A five-year horizon with quantified targets relative to a clearly defined base year.

- Clear definition of organizational boundaries and emission scopes covered.

- Specific actions and measures to achieve reductions.

- Alignment with:

-

-

- The Paris Agreement goal to limit global warming to well below 2°C and pursue 1.5°C.

- The EU Climate Law (Regulation 2021/1119), which sets a legally binding target for the European Union as a whole to achieve climate neutrality by 2050, along with a collective milestone of reducing net GHG emissions by at least 55% by 2030 compared to 1990 levels.

-

-

Importantly, the decree does not prescribe a uniform percentage reduction for individual companies. Instead, it requires that each plan be directionally compatible with the EU’s climate trajectory. Disclosure must demonstrate how the company’s near-term actions contribute to the transition to a sustainable economy, and how its strategy aligns with both national and EU-level climate objectives. This includes showing consistency with Spain’s Climate Emergency Plan and the EU’s legally binding climate targets.

Alignment with EU and Global Climate Goals

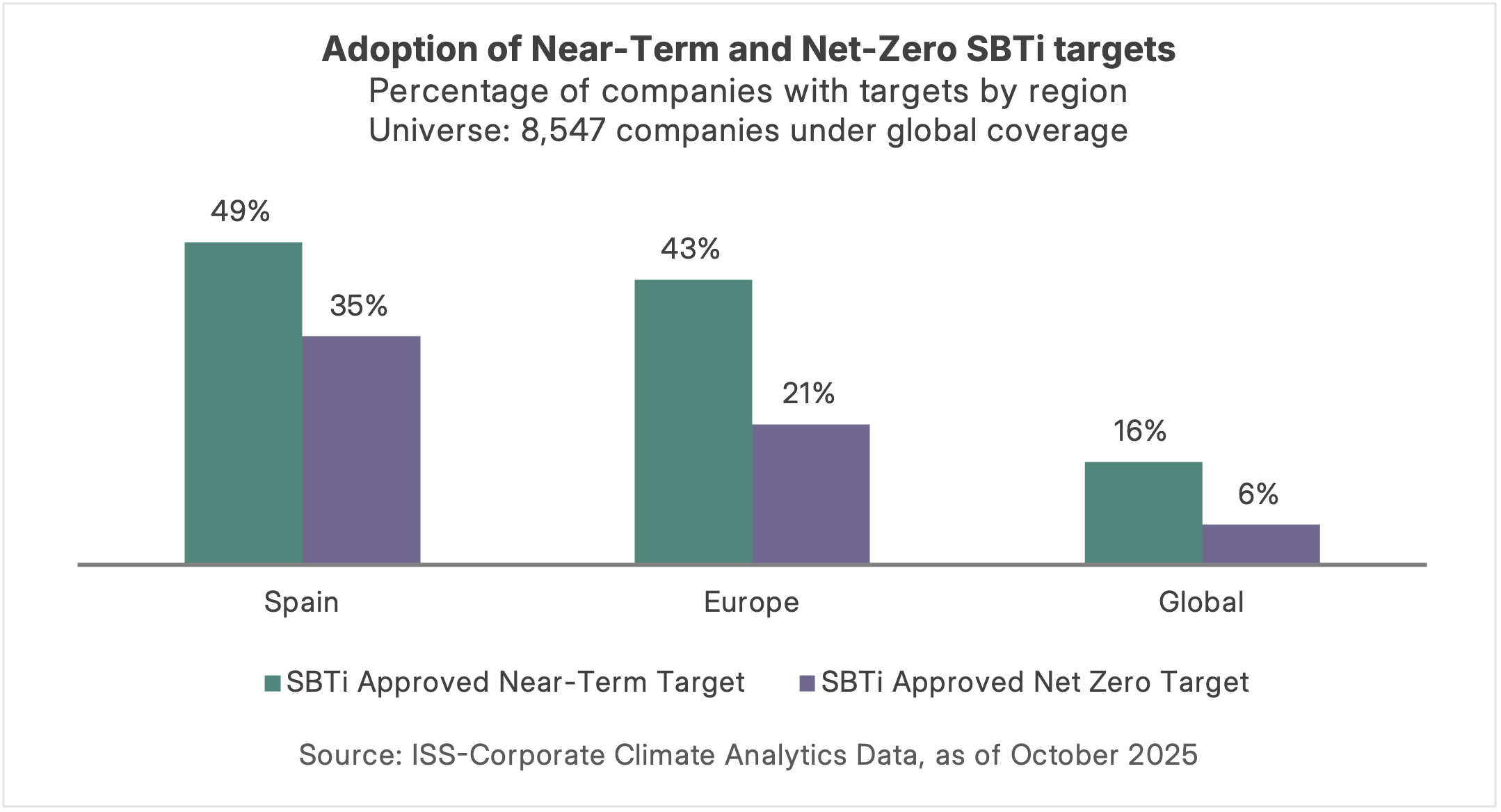

ISS-Corporate analysis shows that near-term and net-zero targets are far from widespread. Globally, only a small fraction of companies have adopted Science-Based Targets, with Europe performing better than other regions. Spain’s numbers are comparatively higher, but with Royal Decree 214/2025 in place, these targets shift from voluntary commitments to mandatory obligations for in-scope companies. For companies without established targets and transition plans, the new mandate requires building credible baselines, strategies, and disclosures fast. Meanwhile, companies in the early stages of their climate journey can turn regulatory pressure into strategic opportunity through proactive planning, strong governance, and clear roadmaps.

Meeting Scope 3 Reporting’s Rising Expectations

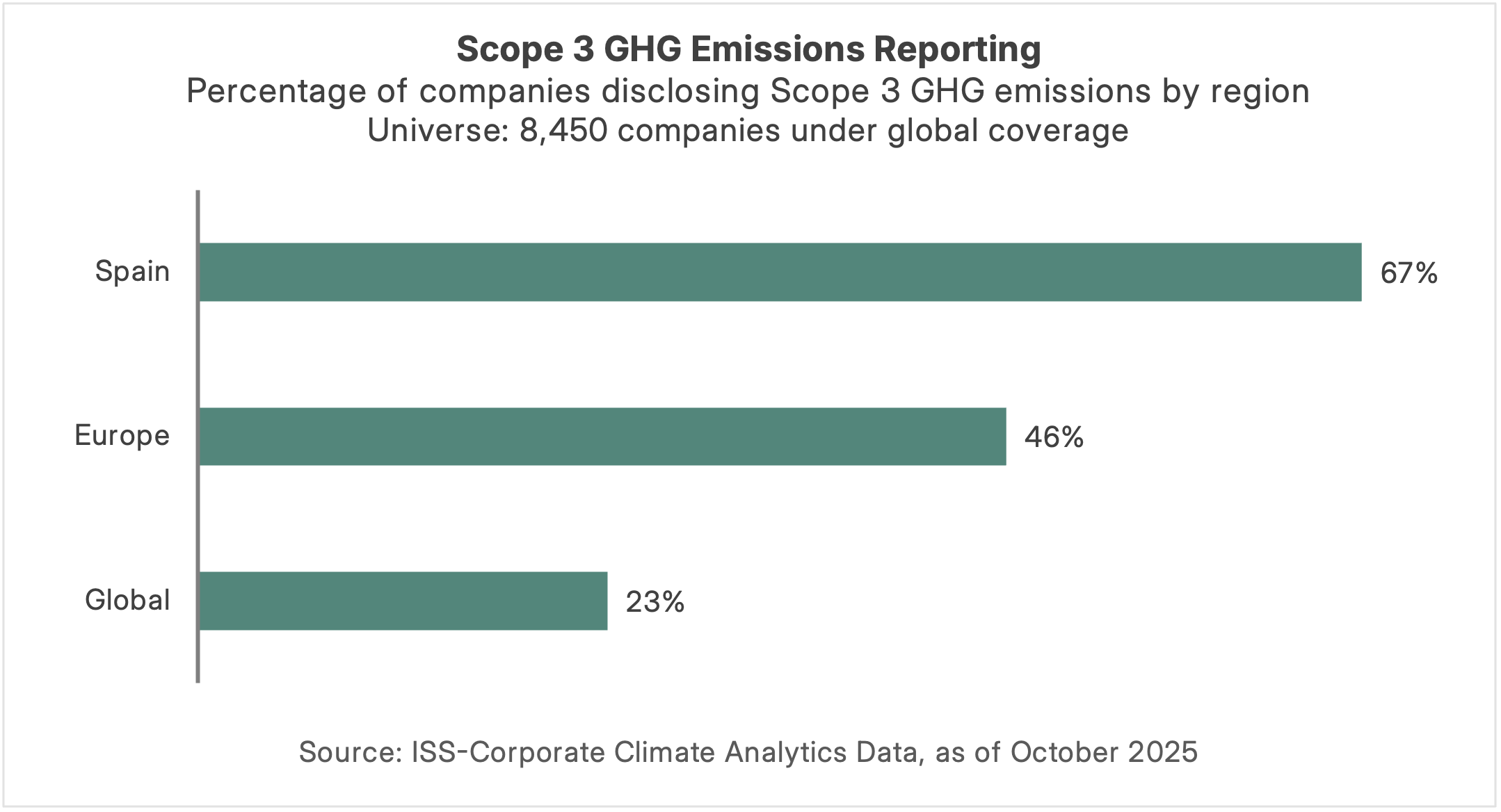

Scope 3 emissions reporting tells a similar story. Globally, fewer than one in four companies disclose these indirect emissions, while Europe shows stronger engagement. Spain is ahead of the curve, but the new decree raises expectations further.

Under the new decree, Scope 3 reporting will initially apply only to public entities, but its effects are expected to extend across supply chains. Larger companies will increasingly request emissions data from suppliers, placing pressure on smaller businesses to measure and disclose their own emissions. The data shown here reflects the largest companies, which helps explain the relatively high disclosure rates – reporting among smaller firms is typically much lower.

For businesses yet to map their value chain emissions, compliance will require significant effort – from data systems to supplier engagement. In such instances, early action not only reduces risk but also positions companies to stay ahead of regulatory demands and strengthen stakeholder trust.

How Companies Can Prepare for Royal Decree 214/2025

Spain’s Royal Decree 214/2025 reflects a growing emphasis on climate-related disclosures. As regulatory and stakeholder expectations evolve, companies will need to assess current practices, identify gaps, and adapt their reporting and planning processes accordingly. While the decree provides a structured framework, its implementation will depend on how effectively companies align internal capabilities with these new requirements. The new law also complements the CSRD framework, which has recently faced delays and scope adjustments. Spain’s move to introduce climate-specific rules ahead of the revised CSRD timeline offers companies a clearer path forward amid broader uncertainty in EU-level reporting.