Sustainability Reporting in Asia: Framework Adoption and Trends in Focus

Across Asia, sustainability disclosures are increasingly shaped by regulatory mandates, with IFRS gaining prominence alongside long established TCFD, SASB, and GRI frameworks.

Asia’s sustainability disclosure landscape is evolving quickly, shaped by a mix of regulatory developments, capital market expectations, and established reporting practices. Across the region, companies are responding to rising demand for decision-useful, investor-oriented sustainability information, while also maintaining frameworks that support broader stakeholder reporting and legacy disclosure programs.

A key recent development is the growing momentum toward the IFRS Sustainability Disclosure Standards (IFRS S1 and IFRS S2), issued by the International Sustainability Standards Board (ISSB). Several Asia jurisdictions have published roadmaps or initial requirements aligned with these standards, signaling a move toward more consistent sustainability-related financial disclosure across markets.

At the same time, the regional baseline did not start from zero. Climate-related disclosures in many markets have been shaped for years by the Task Force on Climate-related Financial Disclosures (TCFD) – and IFRS S2 explicitly integrates and is consistent with TCFD’s four pillars and recommended disclosures.

Against this backdrop, this article reviews how companies in Asia are navigating sustainability disclosure today – including how they reference established frameworks such as TCFD, SASB, and GRI – and what these patterns may indicate as IFRS-aligned requirements begin to scale.

Sustainability Reporting Standards and Frameworks Shaping Asia

Since their issuance in June 2023, the IFRS Sustainability Disclosure Standards (IFRS S1 and IFRS S2) have gained significant traction as a common baseline for investor‑focused sustainability‑related financial disclosure outside the European Union. The IFRS Foundation has reported that jurisdictions representing more than half of global GDP have announced steps toward adoption or other use of these standards, reflecting growing momentum toward globally consistent sustainability reporting.

IFRS Sustainability Disclosure Standards as a Regional Baseline

The IFRS Sustainability Disclosure Standards are emerging as a core baseline for investor‑focused sustainability‑related financial disclosure across many jurisdictions. IFRS S2 builds directly on the TCFD architecture – governance, strategy, risk management, and metrics & targets – enabling jurisdictions and companies with TCFD‑based reporting to transition more efficiently toward IFRS‑aligned climate disclosure.

Based on an ISS‑Corporate review of corporate sustainability disclosures, companies across Asia continue to reference multiple frameworks in parallel, reflecting different regulatory starting points, reporting objectives, and stakeholder audiences. In markets where climate disclosure expectations have been embedded through listing rules and governance codes, references to TCFD tend to be high. For example, Japan’s Corporate Governance Code encourages Prime Market companies to enhance disclosures based on TCFD recommendations (or an equivalent framework).

SASB occupies a different position within the current reporting landscape. Historically developed as a US‑led, industry‑specific framework, SASB content now sits within the IFRS Foundation’s ecosystem: ISSB educational materials clarify that companies applying IFRS S1/S2 “shall refer to and consider the applicability” of SASB Standards and the ISSB’s industry‑based guidance.

GRI remains widely used for broader sustainability reporting in many markets, often alongside investor‑focused disclosure approaches. As a result, it is common to see companies referencing GRI while also increasing alignment with TCFD‑structured climate disclosure – and, increasingly, IFRS‑aligned requirements – rather than treating these approaches as substitutes.

How Sustainability Reporting Differs Across Key Asian Markets

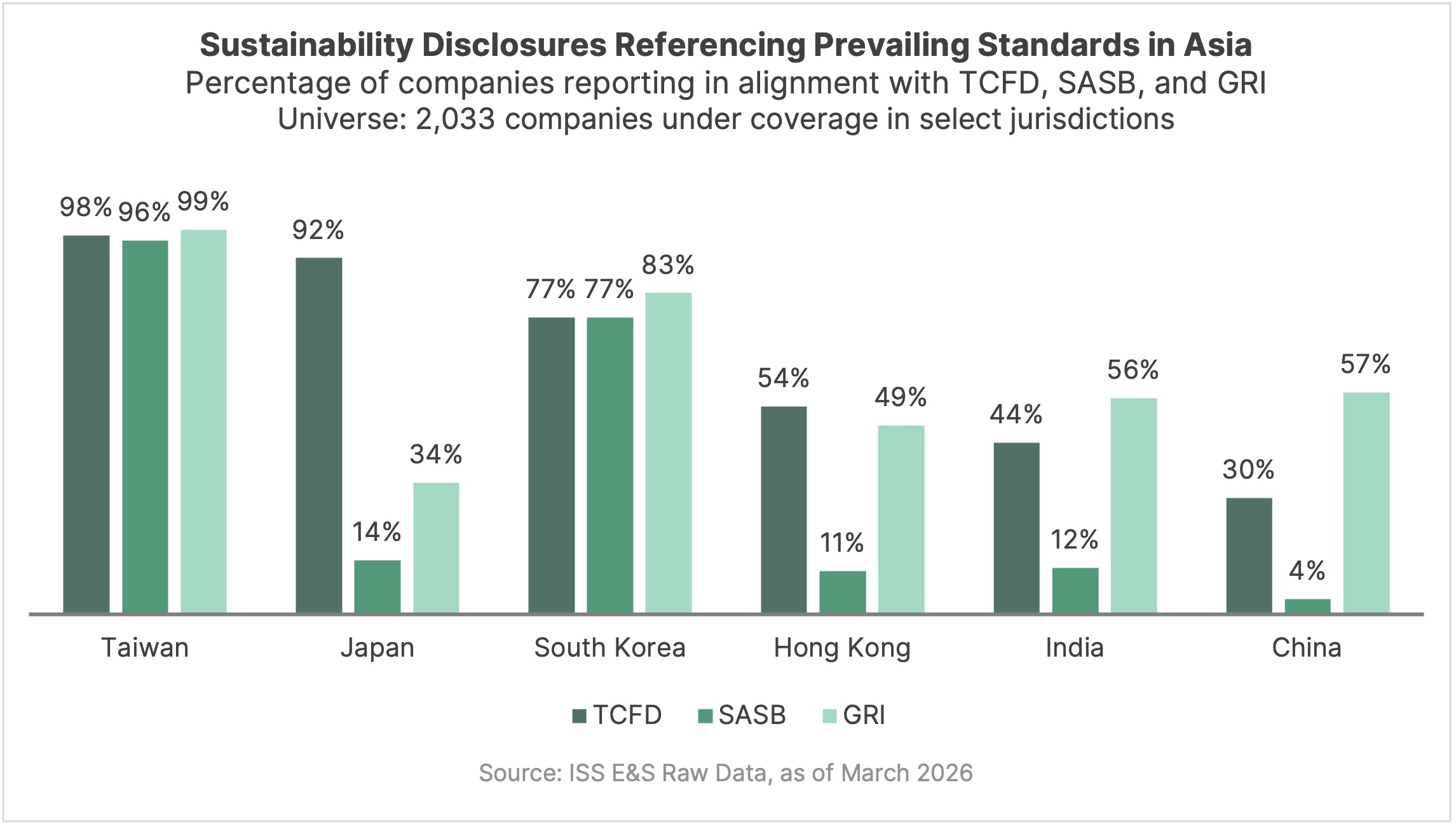

Taiwan stands out as one of the most mature sustainability reporting markets in Asia. Corporate disclosure data show near‑universal referencing across TCFD, SASB, and GRI, reflecting a well‑established, multi‑framework reporting environment. These disclosure patterns are underpinned by a long‑standing regulatory backdrop: prior to the Financial Supervisory Commission of Taiwan’s announcement in October 2025 to adopt the IFRS Sustainability Disclosure Standards, listed companies had been required to report in accordance with the GRI Standards. This historical reliance on GRI, alongside strong climate‑focused and industry‑based disclosure practices, provides important context as Taiwan moves toward closer alignment with IFRS‑aligned sustainability reporting requirements and implementation remains underway.

South Korea also demonstrates relatively advanced sustainability disclosure practices, with companies referencing TCFD, SASB, and GRI at broadly comparable levels (TCFD 77%, SASB 77%, GRI 83%). This pattern points to a blended disclosure approach that combines climate structured reporting, industry based metrics, and broader sustainability frameworks. In the period leading up to the release of IFRS aligned sustainability disclosure standards by the Korea Sustainability Standards Board (KSSB), companies have drawn on established guidance such as the K ESG Guidelines issued by the Ministry of Trade, Industry and Energy in 2021. These disclosure practices provide important context as Korea moves toward IFRS S1 and IFRS S2 aligned requirements built around the TCFD pillar structure.

Japan is characterized by a strong emphasis on climate‑structured disclosure, with a very high level of TCFD referencing (92%) alongside more limited use of SASB (14%) and GRI (34%). This pattern reflects long‑standing expectations under Japan’s Corporate Governance Code for Prime Market companies, as well as the broader regulatory focus on TCFD‑aligned climate disclosure. The release of the Sustainability Standards Board of Japan’s inaugural Sustainability Disclosure Standards in March 2025 marks the next step in Japan’s transition toward IFRS‑aligned sustainability reporting.

Hong Kong exhibits an intermediate sustainability disclosure profile, with moderate referencing of TCFD (54%) and GRI (49%), alongside limited use of SASB (11%). This pattern reflects a regulatory environment that has increasingly emphasized climate‑related disclosure through listing rule requirements, while broader sustainability reporting has developed more unevenly. The introduction of enhanced climate disclosure requirements under the HKEX Listing Rules, developed based on IFRS S2 and effective from the 2025 reporting year under a phased approach, provides important context as Hong Kong moves toward greater alignment with IFRS‑aligned sustainability reporting.

India and China display sustainability disclosure patterns shaped by distinct regulatory architectures, with broader reporting frameworks playing a more prominent role than climate‑structured or industry‑based approaches. In India, sustainability disclosure is anchored in the Business Responsibility and Sustainability Reporting (BRSR) framework mandated by SEBI, with recent regulatory emphasis placed on standardized metrics, industry guidance, limited assurance, and value‑chain disclosures. Rather than replacing BRSR, regulators have focused on strengthening its rigor while encouraging interoperability with global frameworks such as TCFD and ISSB.

In China, regulators have begun constructing a unified national sustainability disclosure system. Following the issuance of the Sustainability Disclosure Standards for Business Enterprises – Basic Standard (Trial) in November 2024 and a climate‑specific standard aligned with IFRS S2 in late 2025, climate‑focused reporting remains in an early, phased stage, providing context for the current disclosure patterns observed.

The Outlook of Sustainability Reporting in Asia

Across Asian markets, sustainability disclosure practices continue to evolve toward greater maturity, structure, and decision‑usefulness. While reporting starting points and regulatory pathways differ, the overall trajectory is clear: companies are increasingly expected to produce disclosures that are more consistent, comparable, and relevant for capital market decision‑making. The growing influence of IFRS‑aligned requirements, alongside continued use of established frameworks such as TCFD, SASB, and GRI, is reinforcing this shift toward more standardized sustainability information. As these practices continue to scale, sustainability disclosures across the region are likely to become more robust and more closely integrated into enterprise‑level risk and performance discussions.