IFRS Sustainability Disclosure Standards: What Companies Need to Know

ISSB sets a global, investor-focused baseline for sustainability reporting through IFRS S1 and S2, integrating material information with financial reporting

The International Sustainability Standards Board (ISSB) has emerged as a central force in shaping the global sustainability reporting landscape in recent years. The ISSB is an international, independent standards-setting body, created by the International Financial Reporting Standards Foundation (IFRS). Established in 2021, it develops a global baseline for sustainability disclosures focused on supporting decision making by the end users of non financial information: investors.

To support investor-focused decision making and ensure global consistency in sustainability disclosures, the ISSB issued two initial standards: IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures. In the past year, it was announced that work was underway on a standard for nature-related risks. In April 2026, the ISSB agreed on the proposed way forward for nature-related disclosures, through the development of an IFRS Practice Statement. The statement will explain how companies should report on nature-related risks and opportunities in accordance with S1.

Prepare for ISSB IFRS sustainability disclosures with ISS‑Corporate expertise »

Further emphasising the ISSB’s goal to provide financially material sustainability information to investors, the organisation operates alongside the International Accounting Standards Board (IASB), ensuring a close relationship between the development of sustainability standards and the existing, widely adopted approach to financial reporting.

What are the IFRS Sustainability Disclosure Standards?

IFRS S1 and IFRS S2 are built on the Task Force on Climate related Financial Disclosures (TCFD) framework and structured around the four pillars: Governance, Strategy, Risk Management, and Metrics and Targets. This makes it easier for many companies familiar with TCFD to start using the new standards.

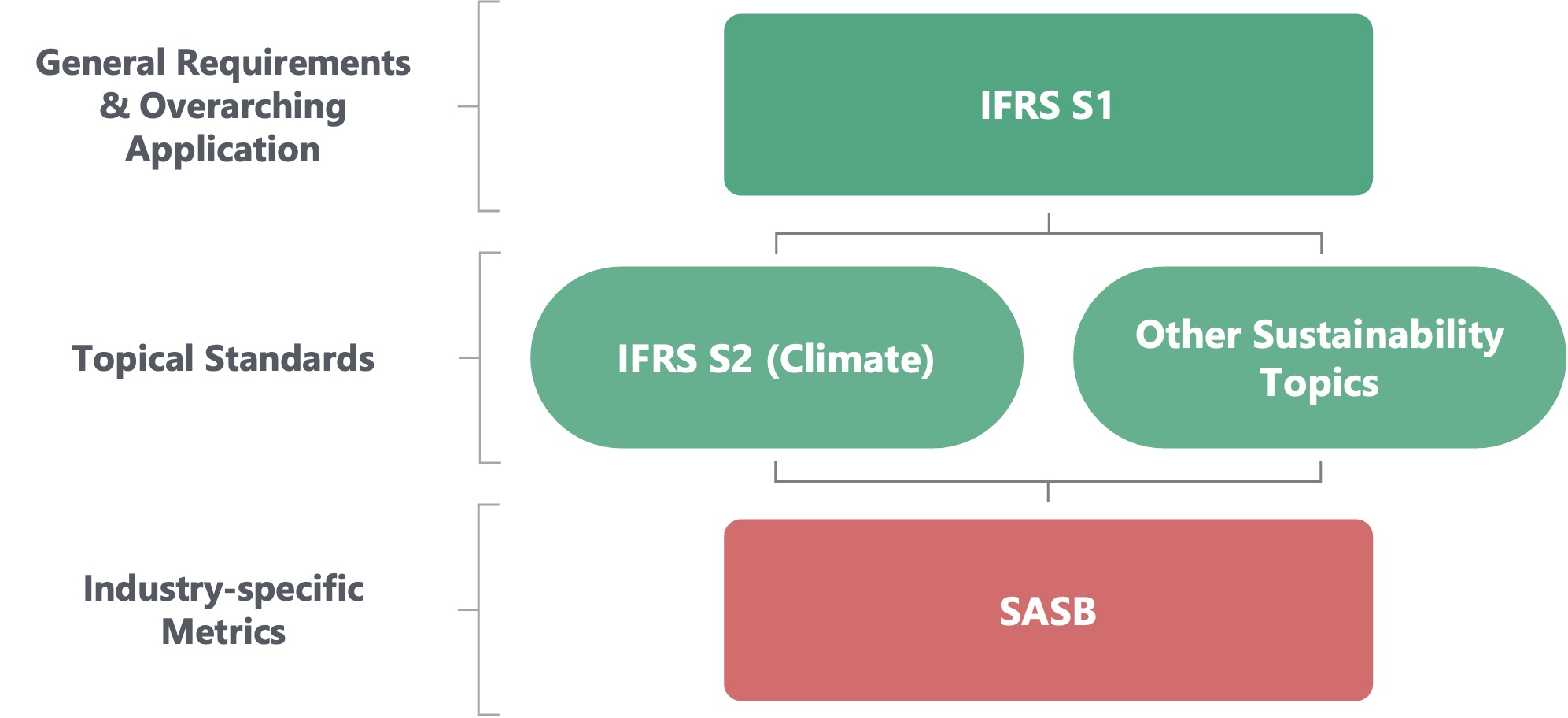

Figure 1: IFRS Structure

In applying this structure, and through public and private consultation, the ISSB has developed the standards with the goal to enable comparability, consistency and verifiability of sustainability information across markets.

Who needs to prepare an ISSB IFRS Report?

The IFRS Sustainability Disclosure Standards (IFRS SDS) have been available for voluntary application since 2024 and are intended to be applicable to companies across sectors and geographies, regardless of size. In practice, however, regulatory implementation is increasingly driving uptake.

Sustainability reporting aligned with ISSB standards is rapidly transitioning from voluntary to mandatory adoption in multiple markets. Currently, over 35 jurisdictions have announced plans to base sustainability disclosure requirements on the ISSB Standards.

Implementation approaches vary by jurisdiction, particularly in terms of scope, phasing, and enforcement. Most regimes are prioritising large, publicly traded companies in initial phases. In some cases, requirements are also being extended to large private companies or entities.

As a result, companies that are listed, seeking capital market access, or operating in jurisdictions aligning with ISSB standards should already be assessing their readiness to report under IFRS S1 and, where relevant, IFRS S2.

What do companies need to disclose?

General sustainability disclosures under IFRS S1

IFRS S1 sets out the general requirements for sustainability related financial disclosures. Rather than prescribing a fixed list of topics, the standard requires companies to identify and disclose all sustainability-related risks and opportunities that are financially material to the business – those that could reasonably be expected to affect enterprise value, specifically through impacts on cash flows, access to finance, or the cost of capital.

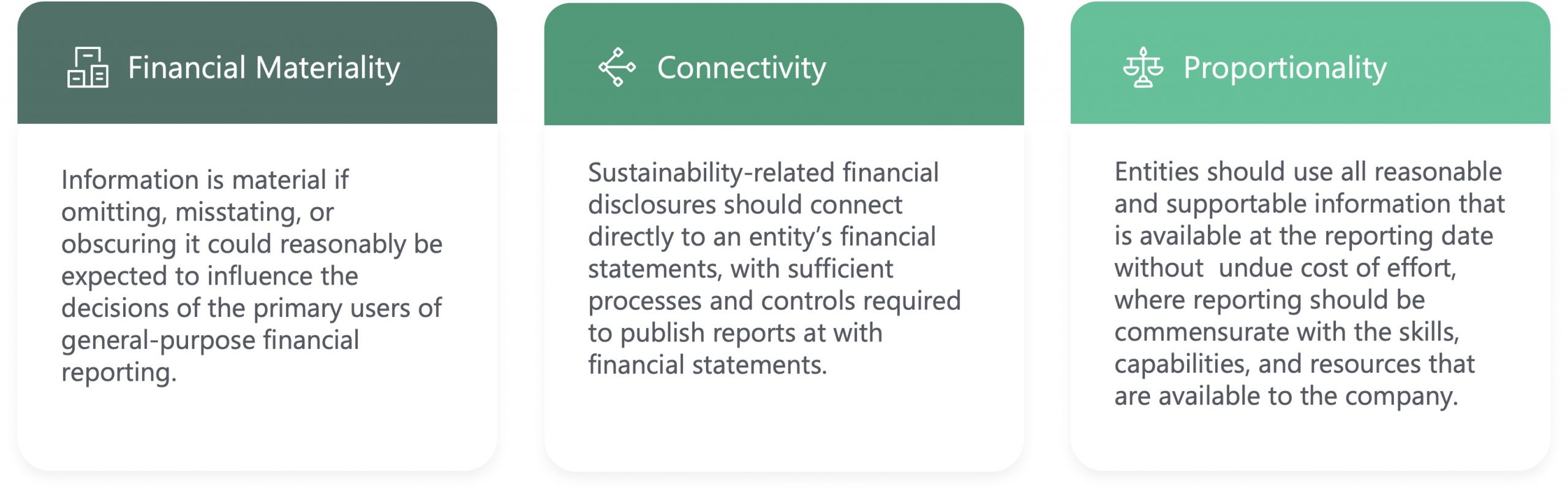

Figure 2: IFRS SDS Key Concepts

In disclosing, companies must explain the governance structure that oversees and manages the risks and opportunities, the impact of those risks and opportunities on the business model and strategy, the process for identifying, assessing and managing material risks, and how performance is measured and monitored over time.

Figure 3: Four Pillars of IFRS SDS

| Pillar | Key Disclosures |

|---|---|

| Governance |

|

| Strategy |

|

| Risk Management |

|

| Metrics & Targets |

|

In addition, companies are expected to tie sustainability information to financial costs or benefits over time and ensure consistency between financial and sustainability disclosures. This concept of connected information is central to ISSB IFRS. For many organisations, this represents a step change from standalone sustainability reports, towards sustainability information that is tightly integrated with financial reporting and corporate strategy.

Reporters can prepare disclosures using reasonable and supportable information, commensurate to their organisation’s size, capabilities and resources, to support the disclosure of decision-useful information without undue cost or effort.

Prepare for ISSB IFRS sustainability disclosures with ISS‑Corporate expertise »

Climate-Related disclosures under IFRS S2

IFRS S2 is the first topical standard that has been produced and covers the climate topic. Built on the TCFD recommendations, it introduces specific disclosure requirements covering climate related risks and opportunities, including governance arrangements, scenario analysis, climate resilience, and greenhouse gas emissions.

Figure 4: Moving from TCFD to IFRS S2 Climate-related Disclosures

Broadly Consistent with TCFD Recommendations, 55% |

Additional Requirement & Guidance, 25% |

More detailed Information Required, 20% |

The ‘climate-first’ relief in IFRS S1 allows companies to report on only their climate-related risks and opportunities in their first year. This means the focus for many firms covered by mandatory IFRS SDS-aligned reporting begins with IFRS S2, before expanding to other sustainability topics.

To report in line with IFRS S2, organisations must disclose:

- Climate-related physical and transition risks

- Climate-related opportunities

- Scenario analysis and resilience of business strategy

- Scope 1, 2, and – where material – Scope 3, Greenhouse gas emissions

- Climate-related targets

Why connectivity between sustainability and financial reporting matters

One of the defining features of the standards is connectivity and linking sustainability disclosures directly to financial reporting and strategic decision-making. This requires sustainability data to be produced, reviewed, and approved with the same rigour as financial information, and understood in terms of financial performance.

In practice, this means that sustainability risks and opportunities need to be quantified, integrated into strategic business decisions, and embedded into existing financial reporting workflows to reduce duplication and improve confidence in their disclosures. This alignment is particularly important as investors and regulators increasingly expect sustainability disclosures to delivered in tandem with the financial report, with comparable and consistent information.

First steps companies should take to prepare for ISSB IFRS

Companies should focus on the following initial steps:

- Ensure internal controls and data processes to build a strong data governance infrastructure

- Enhance board and management oversight of sustainability risks

- Identify financially material risks and integrate them into enterprise risk management

- Improve alignment of sustainability metrics, strategy, and financial reporting

- Track performance using reliable, consistent, and relevant metrics and targets

Early engagement is key for successful disclosure. Companies should start identifying gaps, building internal capabilities, and position themselves for regulatory adoption as soon as possible.

Prepare for ISSB IFRS sustainability disclosures with ISS‑Corporate expertise »