A unified approach to ISSB’s IFRS S1 and S2 reporting

Lay the groundwork today for tomorrow’s sustainability reporting requirements. Advisory expertise, carbon accounting, and sustainability reporting software brought together in a coordinated, simplified, and modular IFRS SDS solution.

Preempt global regulatory expectations with a unified

ISSB-aligned reporting program

Developed by the ISSB, the IFRS Sustainability Disclosure Standards (IFRS SDS) are designed to help companies communicate sustainability information that is decision‑useful for investors and other capital market participants. The standards are intended for entities that access global capital markets and need to provide consistent, comparable disclosures about sustainability‑related risks and opportunities that affect enterprise value. The IFRS SDS are sustainability reporting standards, with climate‑related disclosures addressed first through IFRS S2, alongside overarching requirements in IFRS S1. Together, these standards set out how companies should identify, assess, and disclose sustainability and climate‑related risks and opportunities across governance, strategy, risk management, and metrics and targets.

Today, ISSB Standards are increasingly adopted and referenced across global markets, positioning them as an emerging global foundation for sustainability reporting and a key reference point for boards and management teams.

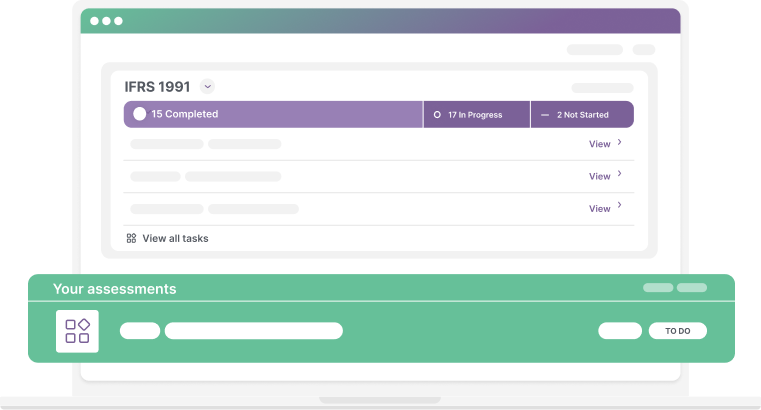

ISS‑Corporate helps support companies with a complete ISSB-aligned reporting program covering IFRS S1 and S2

By combining advisory expertise, carbon accounting, and reporting software, we help organizations move beyond fragmented compliance efforts. Our approach aligns narrative, decisions, data, and workflows through a structured, repeatable pathway—from readiness and analysis through to strategic implementation and reporting.

One integrated program for end-to-end compliance and strategic value

End-to-end

ISSB coverage

Covering IFRS S1/S2 and SASB

Modular by design

Adapted to your reporting journey and regulatory landscape

Built to scale

Expand over time and leverage results across other

reporting frameworks

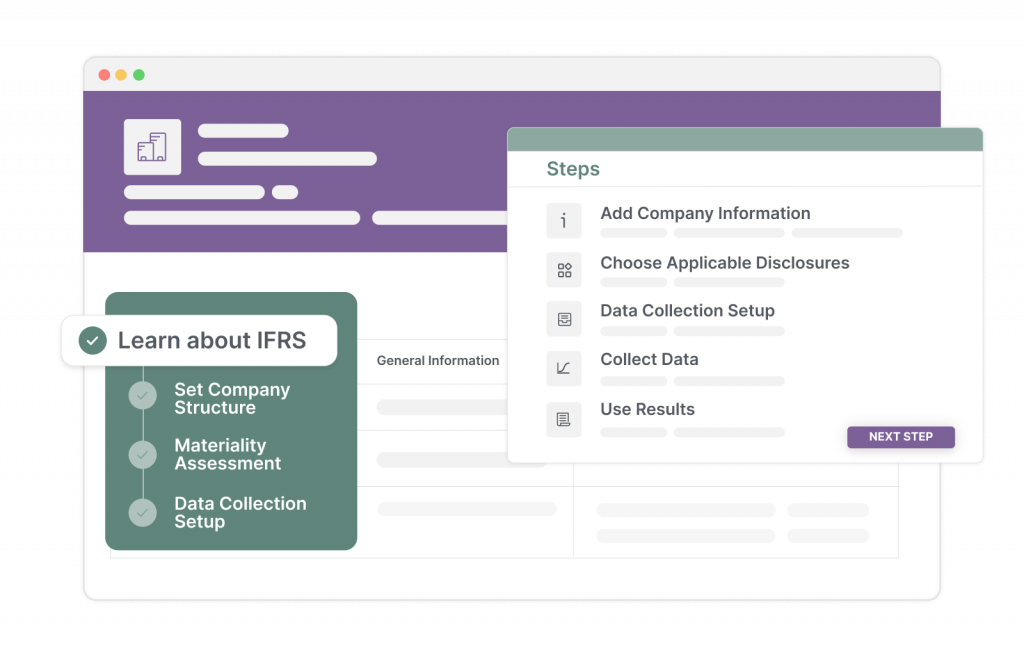

Kick-start or scale your ISSB reporting journey with a structured pathway, beginning with our climate-first program tailored to where you are today

Understand where you are and what it will take to comply

- Compare current climate‑related disclosures, governance practices, and processes against IFRS S2 requirements

- Identify material gaps, priority actions, and near term “quick wins” across strategy, risk management, metrics, and targets

- Define a clear roadmap outlining scope, level of effort, and sequenced next steps to support efficient implementation and planning

Audit-ready emissions data you can trust

- Develop GHG Protocol–aligned Scope 1, 2, and 3 emissions inventories using consistent, transparent methodologies

- Create accurate, assurance‑ready emissions data to support risk analysis, target setting, and IFRS S2 reporting

- Leverage emissions data to strengthen disclosure quality and reinforce stakeholder confidence

Identify where climate hazards could impact your assets—and your bottom line

- Assess exposure to material climate hazards across owned and operated assets, using location‑specific data and climate scenarios

- Understand how hazards translate into financial risk by evaluating potential impacts on assets, business continuity, and value over short‑, medium‑, and long‑term horizons

- Apply risk insights to capital planning, resilience decisions, and disclosures

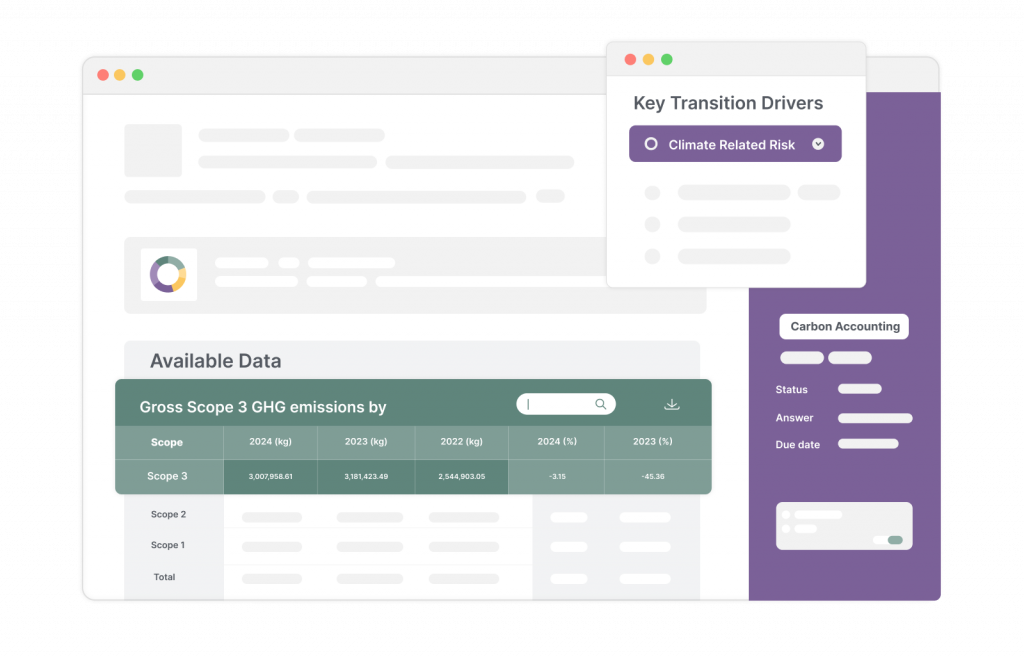

Stay ahead of the low-carbon transition

Assess how key transition drivers—carbon pricing, policy change, energy costs, and technology shifts—could affect your strategy and financial performance. Our analysis highlights both risks and opportunities to inform resilient planning and disclosure.

- Assess how key transition drivers—policy changes, technological advancements, and market shifts—could affect your business strategy and financial performance

- Identify both transition‑related risks and opportunities by analyzing how different transition pathways may impact revenues, costs, and competitiveness over time

- Compare impacts across transition scenarios to understand sensitivity to drivers over time

Set credible, science-aligned climate targets

- Develop clear, defensible climate targets aligned with regulatory expectations and market standards

- Apply SBTi methodologies or tailored pathways to set targets that reflect your emissions profile and business context

- Integrate targets into your broader IFRS S2 narrative to support consistency, credibility, and disclosure quality

An investor-ready transition plan that turns ambition into action

- Design a comprehensive and transparent climate transition plan aligned with IFRS S2 guidance and investor expectations

- Define credible actions, milestones, and governance to support delivery of your transition strategy

- Strengthen the clarity, consistency, and credibility of transition‑related disclosure for stakeholders

Deliver consistent and complete audit-ready climate disclosures

- Structure and prepare ISSB IFRS‑aligned climate disclosures tailored to jurisdiction-specific regulatory requirements

- Ensure disclosures are complete, consistent, and supported by robust data, governance, and documentation

- Strengthen readiness for regulatory review, investor scrutiny, and ongoing reporting cycles

Frequently Asked Questions

The ISSB’s IFRS Sustainability Disclosure Standards (IFRS S1 and S2) are global, voluntary frameworks that can be applied by companies of any size, sector, or location.

While the standards themselves are not mandatory at a global level, they are increasingly being incorporated into national and regional regulatory regimes and are currently being implemented into law as mandatory reporting requirements in 36 jurisdictions.

As a result, many organizations both within and beyond these jurisdictions are choosing to report in line with IFRS S1 and S2 to meet investor expectations and respond to growing market demand for consistent, comparable sustainability and climate‑related disclosures.

IFRS S1 provides the overarching framework and general requirements for all material sustainability-related financial disclosures, while IFRS S2 sets out detailed requirements specifically for climate-related risks and opportunities.

Both. Our ISSB IFRS program combines advisory expertise, carbon accounting, and reporting software into one coordinated solution—so you receive guidance, tools, and execution support without managing multiple providers.

Many clients already report under frameworks such as TCFD, CSRD, or SASB. We help map existing content to an IFRS S1/S2 baseline, identify gaps, reduce duplication, and streamline future reporting cycles.

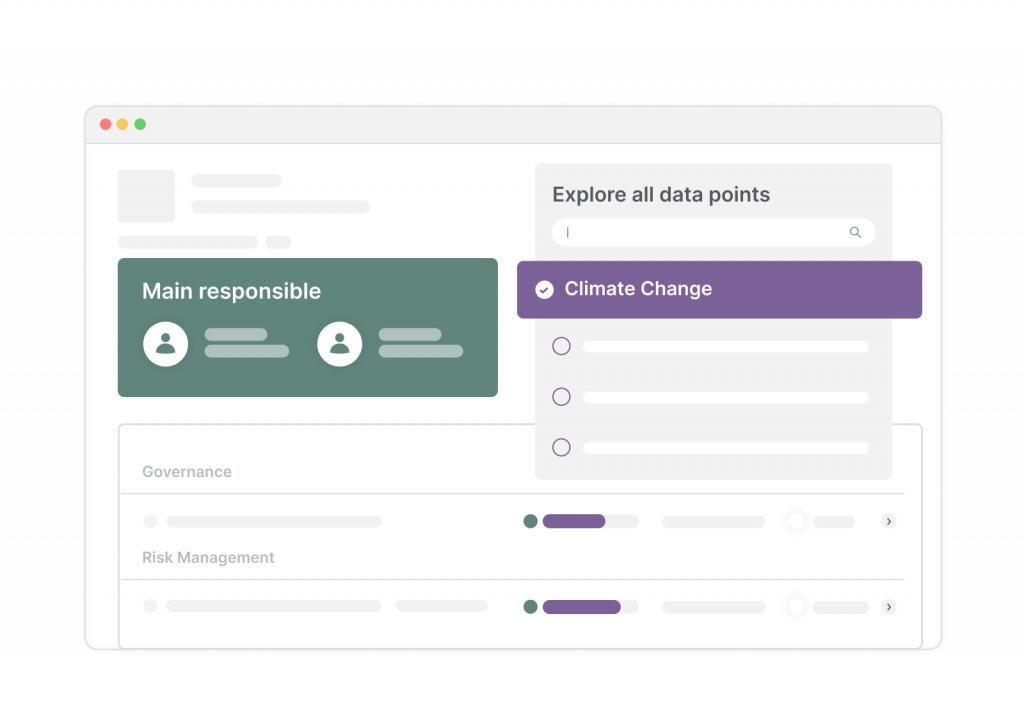

Companies are expected to disclose material information about its sustainability-related risks and opportunities. At a high level, this includes information relating to governance, strategy, risk management, and metrics ad targets related to material sustainability topics.

ISSB IFRS requires companies to disclose only financially material information. Information is considered financially material if omitting, misstating or obscuring it could reasonably be expected to investor decision-making.

No, being a disclosure framework, IFRS S2 does not require companies to develop a formal transition plan. However, it does ask companies to disclose material information related to its climate-related risks and opportunities and its strategies to transition to a climate-resilient economy.

No, net‑zero targets are not mandatory. However, if a company publicly commits to a target, IFRS S2 requires transparent disclosure of how that target will be achieved and monitored.

Recent Resources

ISSB’s Nature Disclosures: What Companies Should Do Now

IFRS Sustainability Disclosure Standards: What Companies Need to Know

UK SRS Published: A New Chapter for Sustainability Reporting

Preparing for the Amended ESRS: Key Considerations While Awaiting Final Adoption

2025 Sustainability Reporting: Global Trends in Framework Adoption

Disclosure Reset: Balancing Simplification and Ambition in Sustainability Reporting

Start your ISSB IFRS reporting journey with

ISS-Corporate

Schedule a live walkthrough of our ISS IFRS solution from one of our reporting experts.