How Sustainability Mandates Shape Proxy Voting

Sustainability-focused funds offer a useful lens on how increasingly mainstream sustainability considerations are shaping stewardship expectations and proxy voting behavior.

Over the past decade, sustainability-focused funds have grown meaningfully in number, visibility, and assets under management as sustainability has become a more established part of investor objectives and of the broader governance and risk management conversation. These strategies are far from uniform. Some concentrate on themes such as climate, water, or clean energy. Others emphasize labor practices, human capital, or faith-based principles. Many take a broader approach, embedding sustainability considerations across investment analysis, engagement, and stewardship more explicitly than is typically the case in more conventional strategies.

According to Morningstar’s latest reporting, sustainable fund assets now total roughly $3.5 trillion globally, despite more muted flows and fewer new fund launches in recent years. That figure, however, captures only part of the picture. Sustainability considerations now influence a much wider universe of asset owners and asset managers, including many that do not market themselves as sustainability-focused. Even so, funds with clearly defined sustainability mandates remain a useful lens through which to examine how differences in philosophy and objectives can translate into differences in stewardship behavior.

Proxy Voting as a Window Into Investor Priorities

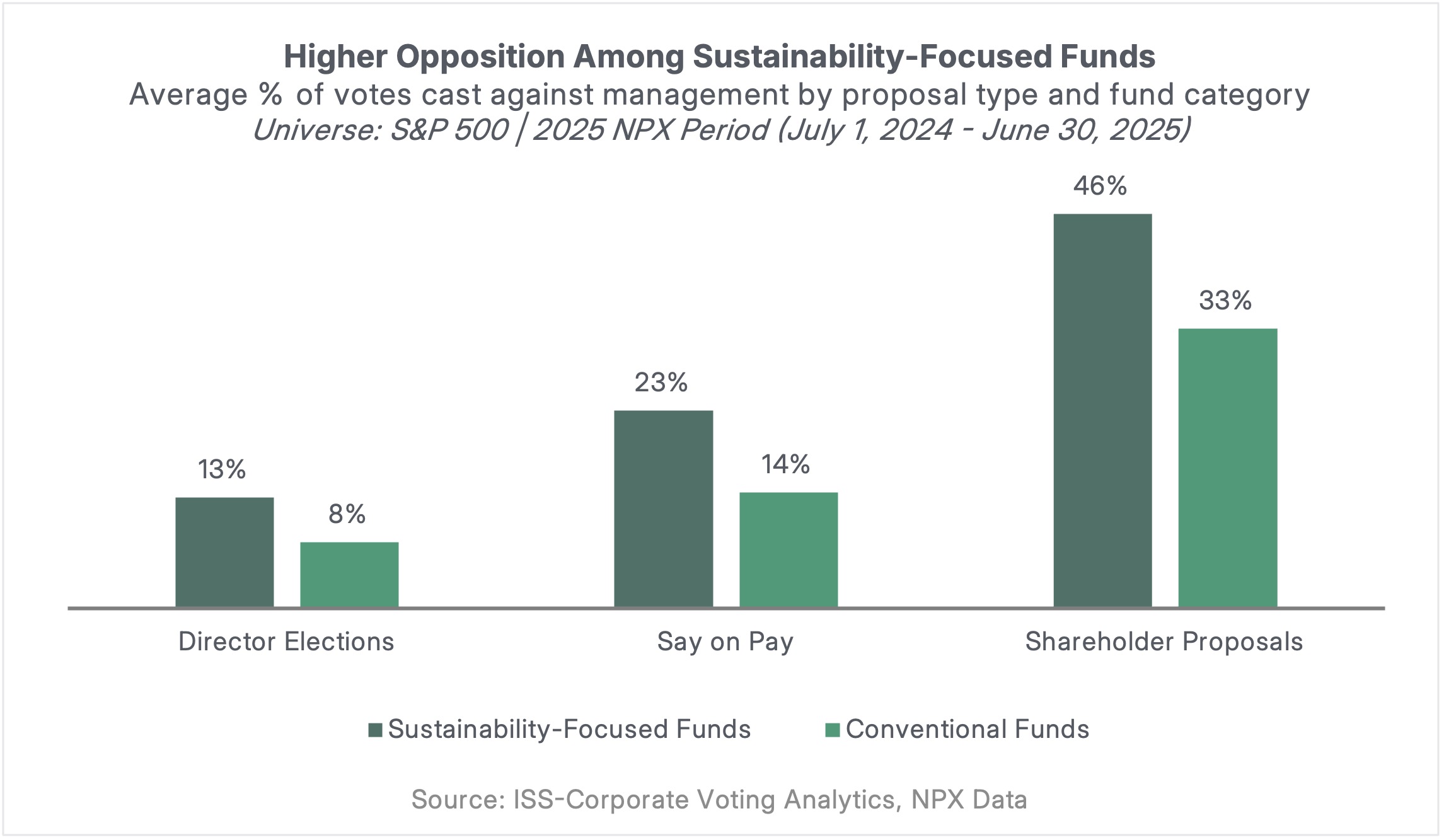

Voting is one of the most direct forms of investor engagement and one of the clearest ways a fund’s mandate becomes visible in practice, whether on director elections, executive compensation, or shareholder proposals. To explore whether sustainability mandates are associated with distinct voting patterns, ISS-Corporate reviewed NPX filings for the most recent proxy period covering shareholder meeting dates from July 1, 2024, through June 30, 2025, comparing the voting behavior of sustainability-focused and conventional funds across S&P 500 companies. The data show a clear pattern: sustainability-focused funds opposed management more frequently across all three major proposal categories examined.

The average opposition rate on director elections was 13% among sustainability-focused funds, compared with 8% for conventional funds. On say-on-pay votes, the gap widened to 23% versus 14%. On shareholder proposals, the difference was larger still: sustainability-focused funds voted against management 46% of the time, compared with 33% for conventional funds. These gaps reflect how mandate influences evaluation criteria. In general, sustainability-focused strategies tend to apply lower tolerance for sustainability-related controversies, more demanding expectations on governance quality, and a broader conception of board accountability. The higher opposition rate on director elections, for example, is not only about climate or social issues in a narrow sense. It also reflects a stricter view of what constitutes an effective and accountable board.

Higher Expectations for Board Accountability and Board Structure

Across sustainability-focused funds, board accountability is often framed more broadly than in more conventional voting approaches. Conventional approaches tend to focus on whether boards respond appropriately after a clear shareholder signal – for example, by implementing a majority-supported proposal, addressing a high withhold vote, remediating problematic pay or audit issues, or avoiding actions that weaken shareholder rights. Sustainability-focused approaches generally retain those expectations but place greater emphasis on whether the board is exercising credible oversight of environmental and social risks in the first place. In practice, that can mean directors face opposition not only for governance breakdowns, but also for weak climate oversight, inadequate sustainability reporting, insufficient disclosure of climate governance and risk management, the absence of credible emissions targets or transition planning, or failure to address serious environmental, safety, or other sustainability-related controversies. The practical effect is a broader understanding of accountability: boards are judged not only on responsiveness to shareholder pressure, but also on whether they are demonstrating sustained oversight of long-term sustainability-related risks.

Another useful illustration is board independence. Conventional voting approaches often focus on whether a board has a simple majority of independent directors and whether key committees are independent. Sustainability-focused approaches frequently set a higher bar. In some cases, the expectation is closer to a two-thirds independent board, often paired with a preference for an independent board chair. Standards may also differ in how strictly independence is interpreted. For example, some investors may view any ongoing professional services relationship with the company as incompatible with independence, whereas more conventional frameworks may apply materiality thresholds in assessing those ties. That difference may seem modest on paper, but in practice it broadens the set of situations in which concerns over board composition can result in votes against directors.

Board refreshment is another area where the distinction often becomes visible. Sustainability-focused investors are generally more likely to raise questions about whether the board is evolving in line with emerging risks and stakeholder expectations. Long tenure does not automatically trigger opposition, but it is more likely to be scrutinized as a possible signal of insufficient renewal, weak challenge, or limited adaptability. In some cases, prolonged tenure may also raise questions about whether a director remains fully independent in practice, even where formal independence standards are technically met. In other words, the question is not only whether directors are classified as independent, but whether the board continues to have the right mix of perspective, expertise, and accountability.

Executive Compensation Faces Stricter Standards

A similar dynamic is visible in executive compensation voting. Conventional approaches generally center on the familiar pay-for-performance framework: whether CEO pay is aligned with company performance, whether problematic pay practices are present, and whether the board has responded appropriately to shareholder concerns. Sustainability-focused approaches typically retain that foundation but evaluate compensation through a broader accountability lens.

In practice, that can mean closer scrutiny of the balance between performance-based and discretionary pay, the rigor and disclosure of performance goals, whether pay design encourages excessive risk-taking or windfall outcomes, and whether equity awards support long-term alignment rather than short-term reward.

In some cases, the analysis also extends to whether environmental or social factors are incorporated into incentive design, whether material sustainability-related controversies raise concerns about executive accountability, and whether large pay disparities or concentrated equity awards signal weaker alignment with stakeholder and shareholder interests. The result is not an entirely different framework, but a more demanding application of it.

More Receptive to Shareholder Proposal

Differences in mandate are especially visible in votes on environmental and social shareholder proposals. Conventional approaches generally assess these proposals on a case-by-case basis, with primary emphasis on whether the request is likely to enhance or protect shareholder value, whether it is reasonable in scope, and whether the issue has already been addressed through company action, regulation, or existing disclosure. Sustainability-focused approaches also consider feasibility, materiality, and company responsiveness, but they are generally more supportive of proposals seeking additional transparency, stronger reporting, or clearer alignment with recognized standards and principles. They also place greater weight on whether the company has adequately addressed shareholder concerns, how its practices compare with peers, and whether controversies or weak disclosure create reputational, operational, or longer-term value risks. The practical effect is a lower level of skepticism toward well-framed disclosure-oriented proposals and a greater willingness to treat environmental and social requests as a meaningful part of stewardship.

What This Signals for Corporate Stewardship

The voting approaches of sustainability-focused funds are useful less because they represent a discrete corner of the market and more because they make visible, in a more explicit form, how sustainability considerations are being incorporated into stewardship. Neither sustainability-focused funds nor conventional funds follow a single model. But the features that stand out more clearly in sustainability-focused approaches – broader accountability, greater emphasis on transparency, and closer attention to environmental and social risk – have increasingly been absorbed into mainstream investment processes as sustainability integration has become more formalized. For companies, that makes these signals important not as a niche set of expectations, but as part of a broader direction of travel in investor oversight.