Why Water Stress Disclosure Matters for Corporate Risk Management

Location-specific water stress disclosure helps companies identify exposure, manage impacts, and communicate how water risks are addressed in vulnerable regions.

June 17, recognized by the United Nations as the World Day to Combat Desertification and Drought, highlights the pressures created by water scarcity, land degradation, and the competing demands placed on shared natural resources. For companies, these pressures are not limited to environmental strategy. They can affect operating continuity, local stakeholder relationships, supply chains, and the reliability of inputs that many sectors depend on.

Water management is therefore increasingly a question of location, context, and impact. Aggregate water-use figures can describe the scale of a company’s footprint, but they do not show whether that use occurs in places where water resources are already under strain. A facility operating in a water-abundant region may present a very different risk profile from one operating in a basin facing recurring drought, competing community and agricultural demand, or declining groundwater availability. More decision-useful disclosure begins with a clearer view of where water is withdrawn or consumed, and whether those locations are subject to high water stress.

Management practices matter as much as measurement. In water-stressed areas, general efficiency programs may not be enough. More meaningful approaches may include water reuse and recycling, process changes that reduce consumption, site-level water risk assessments, engagement with local stakeholders, and contingency planning for periods of scarcity. These practices can help reduce pressure on shared water resources while supporting operational resilience.

Water Stress Disclosure Trends Across Regions and Company Sizes

ISS-Corporate reviewed corporate disclosure data on water withdrawal from areas of high-water stress, assessing whether companies provide explicit information on this topic. The analysis captures companies that disclose a quantitative figure, whether absolute or relative, as well as companies that state they do not withdraw water from areas of high-water stress. Companies without such disclosure are treated as silent on the topic.

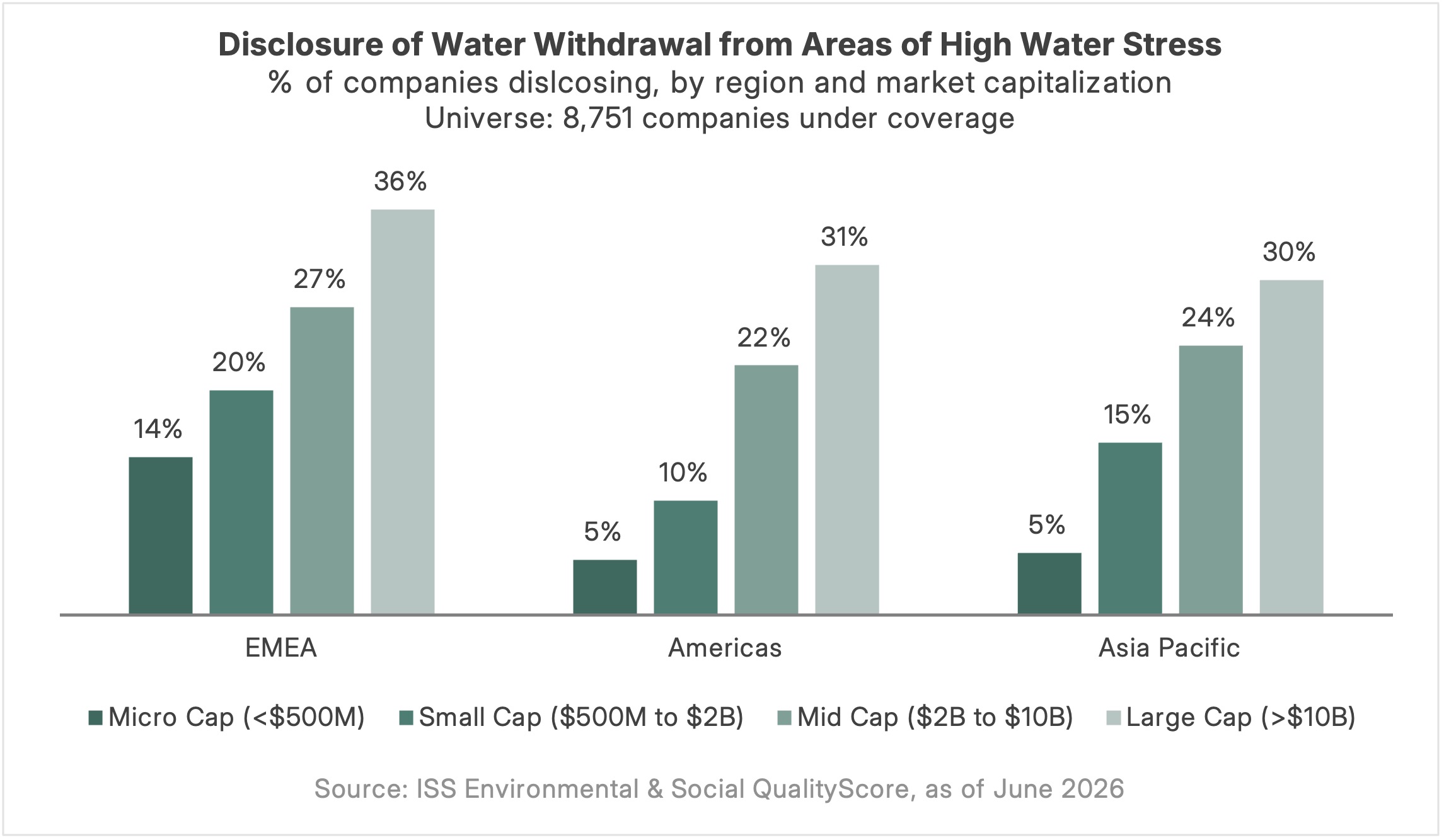

Larger Companies Lead Water Stress Reporting

The results point to a familiar disclosure pattern: larger companies are more likely to provide this information, and disclosure rates are generally higher in markets with more developed sustainability reporting practices. Across each region, disclosure increases with market capitalization. Among large-cap companies, disclosure rates reach 36% in EMEA, 31% in the Americas, and 30% in Asia Pacific, compared with 14%, 5%, and 5%, respectively, among micro-cap companies. This suggests that company size remains an important indicator of disclosure maturity, likely reflecting greater reporting capacity, stronger investor scrutiny, and more established sustainability governance.

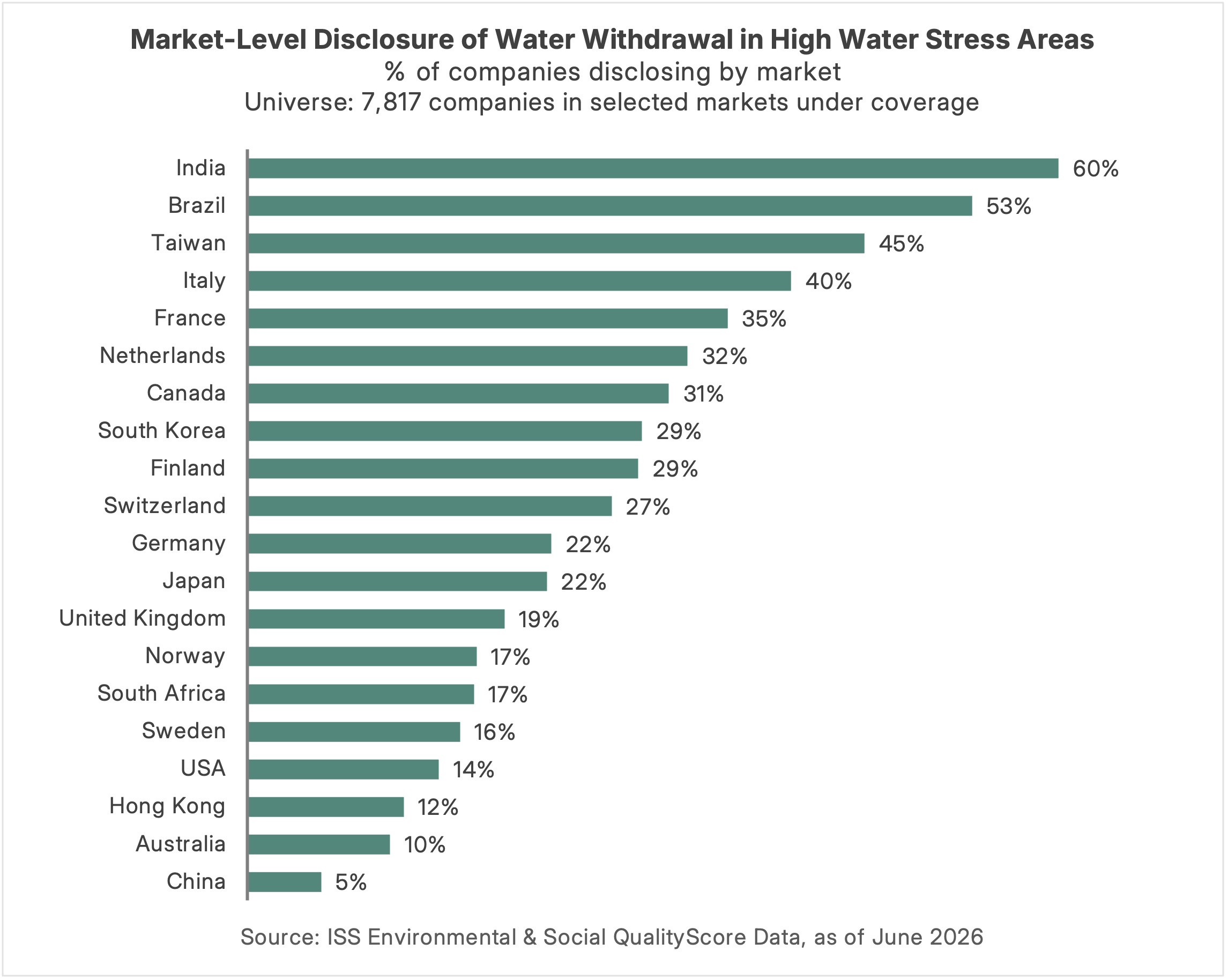

Water Stress Reporting Varies Across Global Markets

Market-level results show additional variation. India, Brazil, and Taiwan report some of the highest disclosure rates among markets with meaningful coverage, at 60%, 53%, and 45%, respectively. These results likely reflect a combination of reporting requirements, market expectations, and sector exposure. In India, the Business Responsibility and Sustainability Reporting framework includes specific water-related disclosure expectations, including total water withdrawal, consumption, discharge, and information on water withdrawn, consumed, and discharged in areas of water stress, which may help explain the relatively high level of disclosure observed in the data. Taiwan’s disclosure environment is also relatively structured, with TWSE-listed companies required to prepare sustainability reports using GRI Standards, while the rules also allow reference to SASB standards for industry-specific metrics. Brazil’s higher disclosure rate may reflect a combination of market practice and regulatory momentum around sustainability reporting. The country’s securities regulator has established an ISSB-aligned framework for sustainability-related financial information, even as recent amendments shifted the regime toward voluntary reporting.

Canada’s 31% disclosure rate is also notable, particularly relative to the U.S. At least part of the trend may reflect the reporting profile of larger Canadian issuers and the country’s evolving sustainability disclosure environment, including voluntary Canadian Sustainability Disclosure Standards aligned with the ISSB framework. Across all geographies, sector mix may also be relevant, especially where extractives, materials, utilities, food, agriculture, semiconductors, and other water-relevant industries are more prominent in the covered universe.

Industry Differences in Water Stress Disclosure

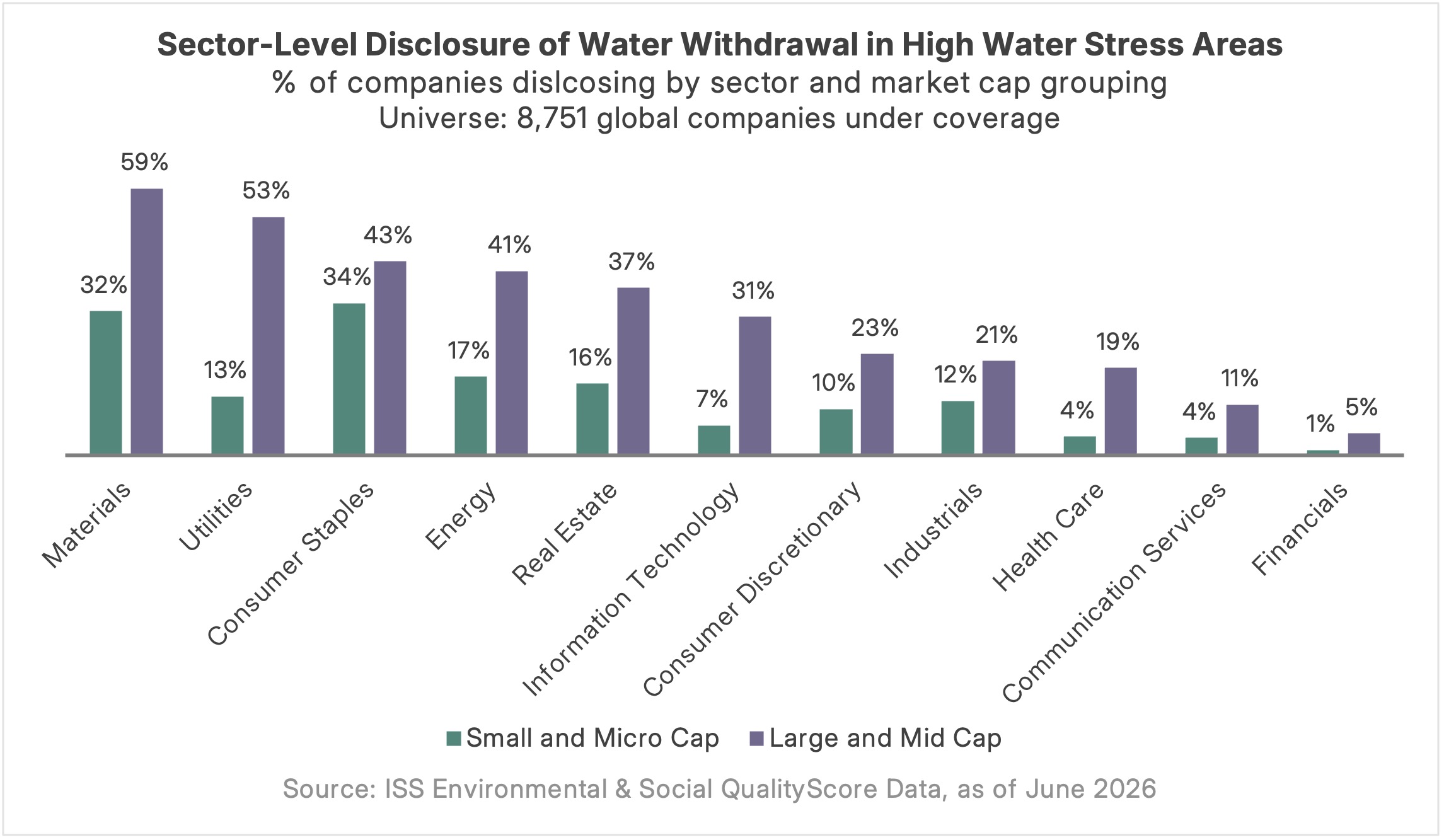

Water-Intensive Industries Show Higher Disclosure Rates

Sector-level results further suggest that disclosure is closely tied to the operational relevance of water. Among large and mid-cap companies, disclosure rates are highest in materials and utilities, where water is often directly connected to production, processing, cooling, and site-level operations. Consumer staples and energy also show relatively elevated disclosure levels, reflecting the importance of water across food, beverage, agriculture, refining, upstream operations, and related value chains.

The results also point to water stress as a topic that extends beyond traditionally water-intensive industries. Information technology shows a comparatively meaningful disclosure rate among larger companies, likely reflecting the growing visibility of water use in semiconductor manufacturing, data centers, and other infrastructure supporting the digital economy. By contrast, sectors with less direct operational water dependency, such as financials and communication services, show much lower disclosure rates.

Reporting Maturity Influences Disclosure Across Sectors

The difference between larger and smaller companies is also important. Across nearly every sector, large and mid-cap companies disclose at higher rates than small and micro-cap companies. This suggests that sector exposure is only part of the story. Disclosure also appears to reflect reporting maturity, internal data systems, investor scrutiny, and the capacity to assess water use by geography. Overall, the sector breakdown supports a practical interpretation: companies are more likely to disclose water withdrawal from high-stress areas when water is both operationally relevant and supported by more mature reporting infrastructure.

Better Water Disclosure Support Better Risk Management

The data suggest that disclosure on water use in high-stress areas remains uneven, but the pattern is not random. It is more common among larger companies, in markets with more developed reporting expectations, and in sectors where water is more directly connected to operations and local impacts. These patterns also underscore the direction of disclosure practices: as drought and water scarcity become more salient business issues, stakeholders are likely to expect more geographically specific information on both exposure and response.

For companies, location-specific water disclosure can support better risk identification, reduce pressure on shared resources, and strengthen water-related reporting. The value of this reporting lies not only in measuring water use, but in explaining its geographic context and how related risks are being managed.