From Framework to Implementation: ISSB Alignment in Practice

Global reporting is evolving around IFRS sustainability standards, with regulation-driven momentum and a growing focus on implementing integrated climate and risk disclosures within enterprise value frameworks.

The global sustainability reporting landscape is undergoing a transition from fragmented frameworks toward a more consistent, financially integrated model. The introduction of the IFRS Sustainability Disclosure Standards establishes a common architecture that links sustainability-related risks and opportunities directly to enterprise value, aligning disclosure more closely with financial reporting and investor decision-making. In doing so, it reduces the separation between sustainability and financial reporting, placing both within a shared reporting framework.

At the center of this framework are IFRS S1 and IFRS S2. IFRS S1 sets out the general requirements for disclosing sustainability-related risks and opportunities that could reasonably be expected to affect enterprise value, while IFRS S2 applies that model specifically to climate. The structure builds on the TCFD framework, organized around governance, strategy, risk management, and metrics and targets, and reflects a broader effort to embed sustainability-related information within the same logic and discipline that governs financial reporting.

As jurisdictions move toward adoption – whether through direct incorporation or local adaptation – a clearer global baseline is emerging. Since the standards were issued, IOSCO support and increasing regulatory engagement have accelerated momentum across regions. While implementation pathways differ, a consistent pattern is taking shape: climate-related disclosure is often the first entry point, with phased approaches and transitional reliefs in more complex areas such as Scope 3 emissions.

At the same time, efforts to improve interoperability are beginning to address long-standing concerns about fragmentation. Initiatives by the IFRS Foundation, EFRAG, and GRI are helping clarify how major frameworks can be used together, supporting the development of a more coherent reporting architecture and enabling companies to build from a common core while adapting to jurisdiction-specific requirements.

For companies, the priority is now implementation. This involves translating the standards into internal processes that support consistent data collection, analysis, and reporting, and integrating climate-related considerations into governance, strategy, and risk management.

Implementation Readiness and Drivers of ISSB Alignment

Earlier this week, ISS-Corporate hosted a webinar and product launch titled “A Complete ISSB-Aligned Sustainability Reporting Solution: Introducing a Unified IFRS S1 & S2 Program.”

REPLAY: A Complete ISSB-Aligned Sustainability Reporting Solution [Americas & EMEA]

REPLAY: A Complete ISSB-Aligned Sustainability Reporting Solution [Asia-Pacific]

The session focused on the practical implementation of the IFRS Sustainability Disclosure Standards, including how IFRS S1 and IFRS S2 work together, how adoption is evolving across jurisdictions, and how companies are translating these requirements into internal processes, reporting workflows, and decision-making structures. It also examined the growing convergence of the reporting landscape, including interoperability with other major frameworks, and outlined the operational steps involved in moving from gap assessment to reporting. As part of the discussion, participants were asked two audience poll questions designed to gauge both where organizations currently stand in operationalizing the standards and what is driving their response.

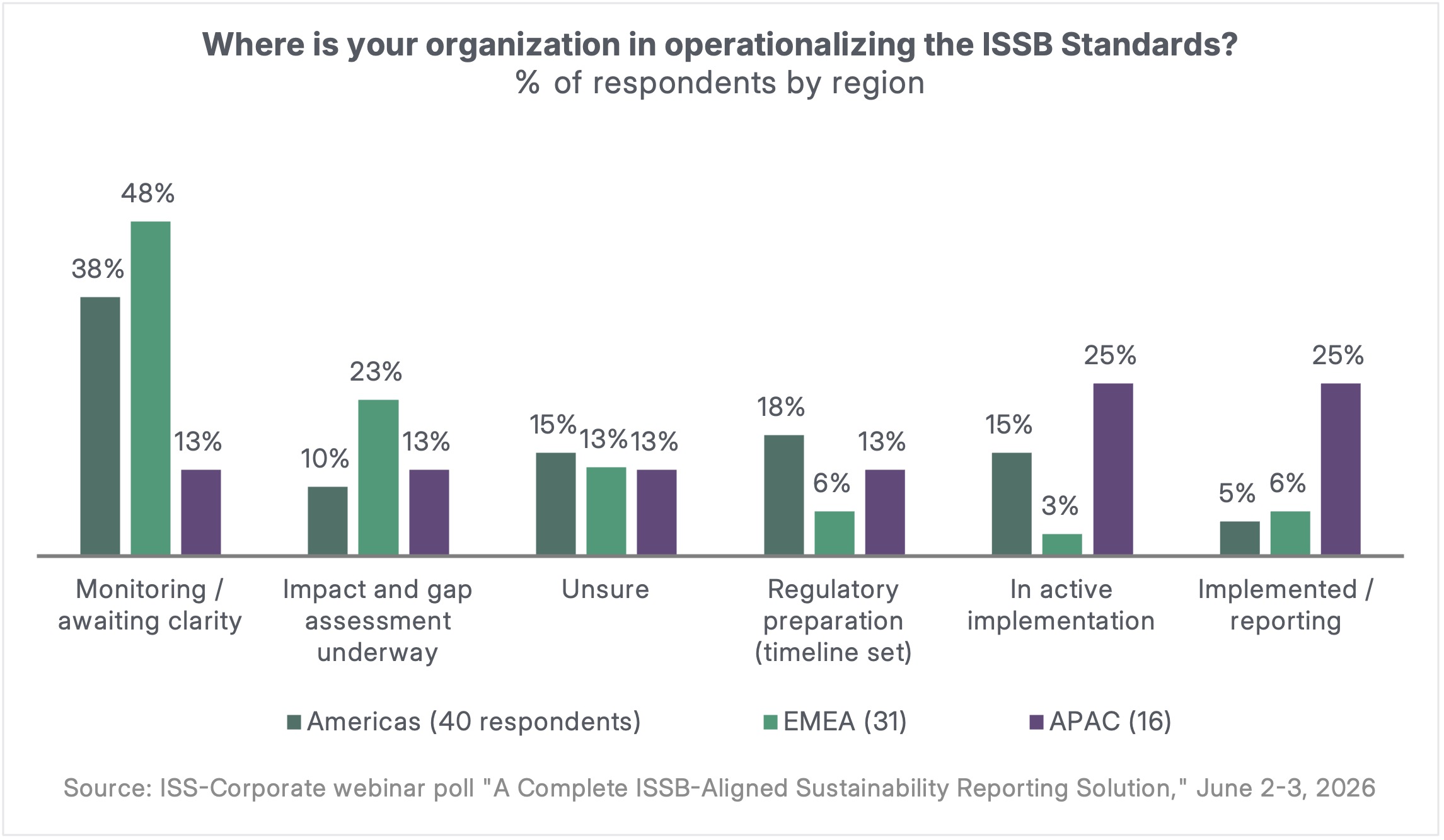

Responses to the first poll question – “Where is your organization in operationalizing the ISSB Standards?” – suggested a split between regions that are still assessing the landscape and those moving more decisively into execution. In the Americas and EMEA, the largest share of respondents said they were still monitoring developments or awaiting clarity (38% and 48%, respectively), with EMEA also showing a meaningful proportion engaged in impact and gap assessments (23%). By contrast, APAC respondents appeared further along the implementation curve, with 25% indicating they were in active implementation and another 25% already implemented or reporting. The pattern is directionally consistent with the broader discussion in the webinar: climate-related disclosure is increasingly becoming the entry point for adoption, but the pace of operationalization still varies by market, regulatory context, and internal readiness.

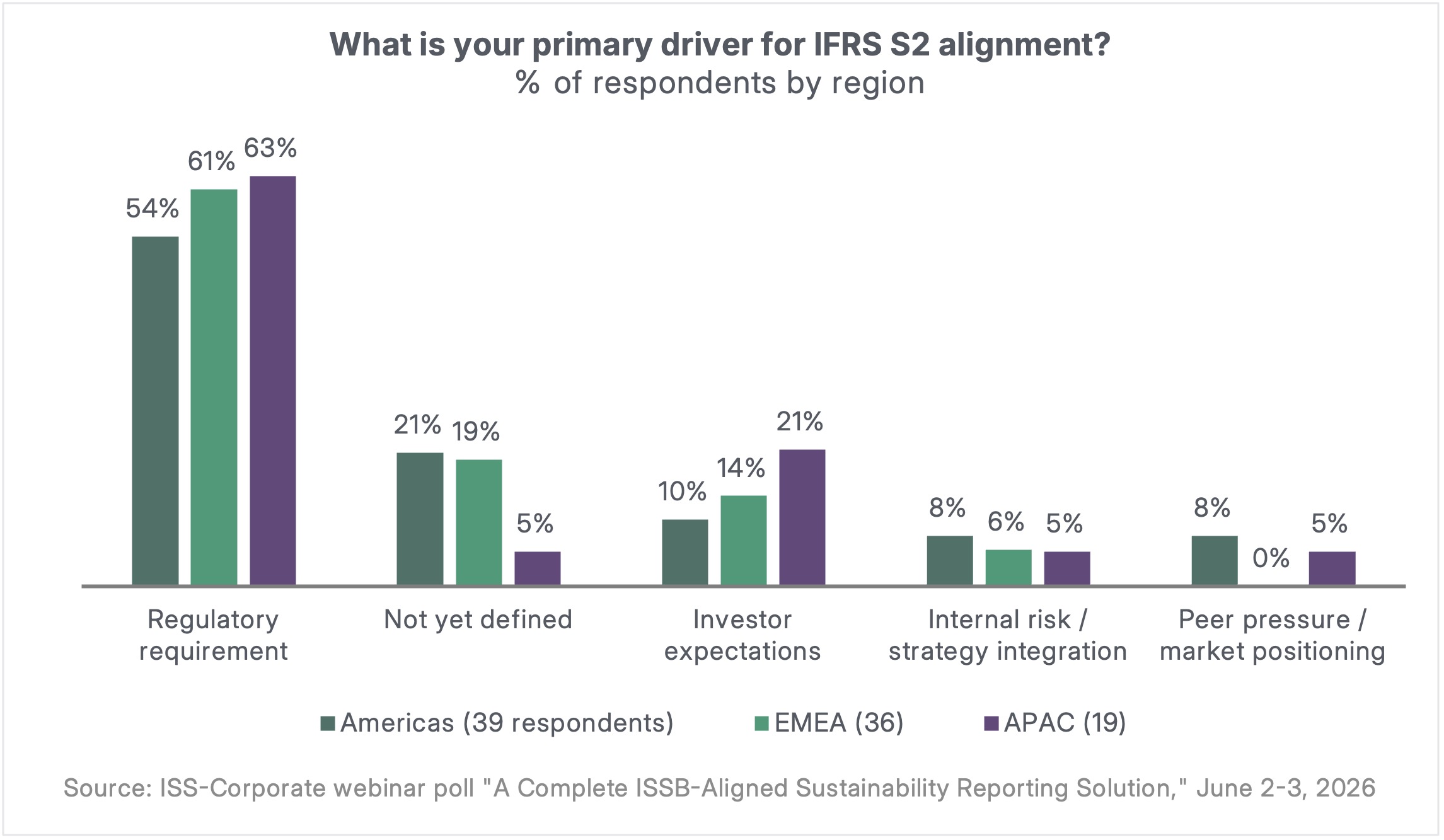

The second poll question – “What is your primary driver for IFRS S2 alignment?” – showed a much clearer point of convergence. Across all three regions, regulatory requirements featured as the dominant driver, cited by 54% of respondents in the Americas, 61% in EMEA, and 63% in APAC. That result aligns closely with one of the webinar’s central themes: regulation remains the primary catalyst for action, even if investor expectations and strategic considerations are also part of the picture. Investor expectations were the second most significant driver in APAC (21%) and EMEA (14%), while a notable share of respondents in the Americas (21%) and EMEA (19%) said their primary driver was not yet defined. Taken together, the results suggest that many companies are approaching IFRS S2 first as a disclosure and compliance challenge, but one that increasingly sits within a broader shift toward more integrated, decision-useful reporting.

Differences in Pace, Similar Direction

ISSB alignment is still being shaped in practice. While a global framework is emerging, companies are moving at different speeds, with regional variation reflecting regulatory timing and internal readiness. At the same time, regulatory requirements remain the primary catalyst across markets. What is beginning to come into focus, however, is a broader transition: climate-related disclosure is not only a compliance exercise, but part of a wider effort to integrate sustainability-related considerations into governance, strategy, and risk management in a more structured and consistent way.